Picture this: that unexpected car repair bill lands in your lap, or maybe you’ve been dreaming about finally updating your kitchen. Your savings aren’t quite there yet, and the thought of borrowing money starts creeping in. Many people immediately think of a personal loan as the go-to solution. After all, it’s straightforward and can cover just about anything. But here’s the thing I’ve noticed after years of watching how folks manage their money – sometimes, there are better paths that could save you serious cash or give you more flexibility.

Recent surveys suggest nearly half of Americans lean on personal loans for big-ticket items or emergencies. It’s easy to see why. These loans offer fixed payments and can come with decent rates if your credit is solid. Yet, they aren’t always the perfect fit. Interest can add up, approval isn’t guaranteed, and the terms might not match what you really need. That’s where exploring alternatives becomes not just smart, but essential.

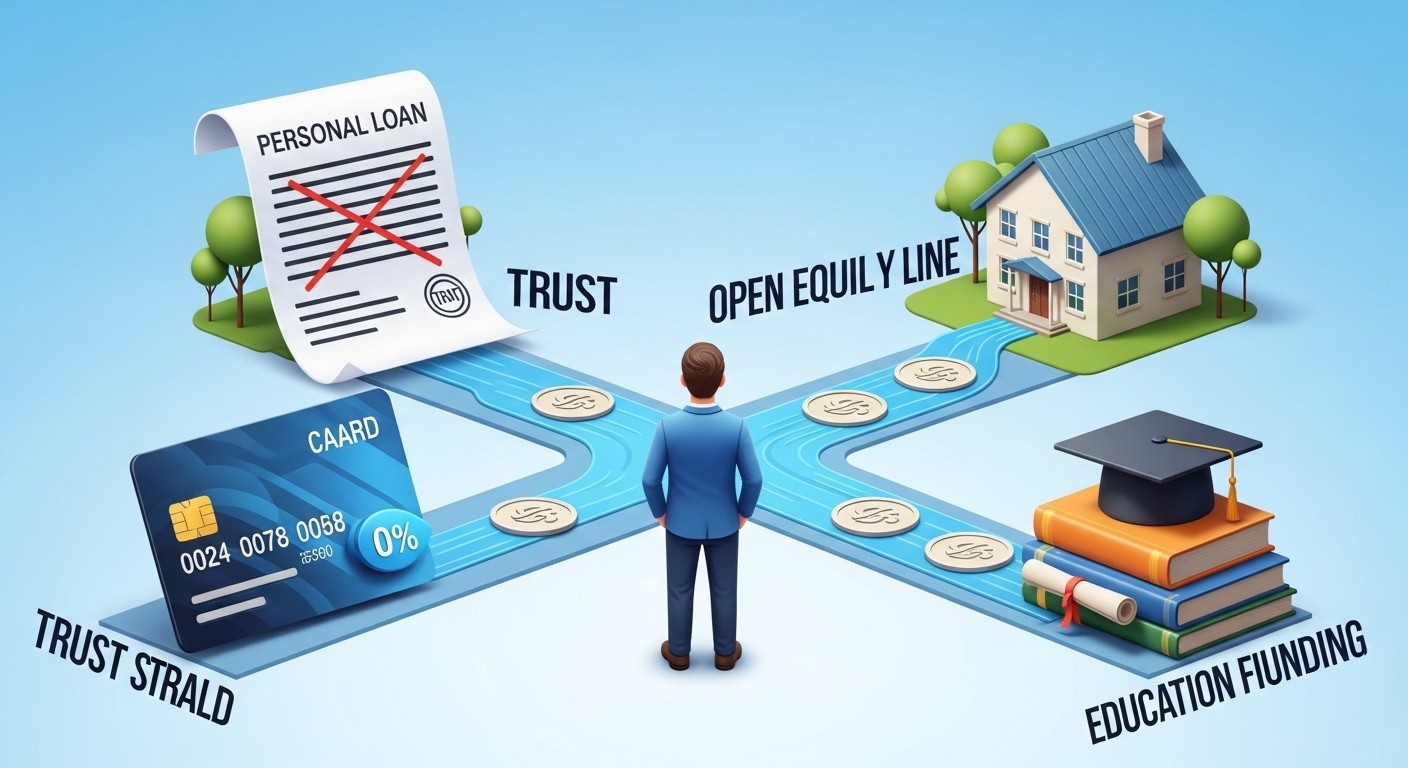

Why Look Beyond Personal Loans for Major Purchases?

Let’s be honest. Taking on debt for a major expense feels heavy enough without wondering if you’re getting the best deal possible. Personal loans shine in many situations because they’re unsecured and versatile. You don’t put your house on the line, and the application process is usually quick. But they come with their own drawbacks – rates that can climb if your credit isn’t top-notch, origination fees that nibble at the amount you actually receive, and repayment schedules that don’t always bend to life’s curveballs.

In my experience chatting with people about their finances, the real game-changer often lies in matching the financing tool to the specific need. A one-size-fits-all approach like defaulting to a personal loan might work, but it rarely optimizes your costs or risks. Whether it’s spreading out payments interest-free, tapping into existing assets, or funding something as targeted as education, other options can align better with your goals. And in a world where every dollar counts, that alignment can make all the difference between stress and relief.

Of course, no financial decision is one-size-fits-all. Your credit score, the size of the expense, and your overall money picture all play huge roles. Still, having these three alternatives in your back pocket can empower you to make choices that feel more tailored and less burdensome. Let’s dive into them one by one, with real talk about when they might beat a personal loan hands down.

Zero Percent APR Credit Cards: Buy Now, Pay Later Without the Interest Sting

Imagine charging a significant purchase to a card and not paying a penny in interest for months – even up to a couple of years in some cases. That’s the magic many 0% APR introductory offers bring to the table. These cards are designed specifically to give you breathing room on new purchases or balance transfers, letting the cost of that big expense spread out over time without extra charges eating into your budget.

Why does this matter when comparing to personal loans? Personal loans usually start accruing interest right away, even if the rate looks reasonable on paper. With a solid 0% APR card, you essentially get an interest-free loan period. Pay it off before the promo ends, and you’ve avoided hundreds or even thousands in interest. It’s particularly handy for emergencies or planned big buys where you know you can clear the balance within that window.

Zero-interest periods can turn a stressful expense into a manageable monthly commitment, as long as you stay disciplined.

I’ve seen friends tackle everything from medical bills to home upgrades this way. One even furnished an entire apartment during a long intro period and came out ahead because they budgeted aggressively. But here’s the catch – and it’s an important one. These offers aren’t forever. Once the introductory phase wraps up, the regular APR kicks in, and it can be steep, sometimes climbing into the high twenties. Miss the payoff deadline by even a day, and you could face retroactive interest on the whole balance. Discipline is non-negotiable here.

Another upside? Many of these cards come with no annual fee, making them accessible without ongoing costs. Some even throw in perks like cell phone protection or purchase safeguards that add extra value. If your credit is good to excellent, qualifying is often straightforward, though you’ll want to check your score first since approvals hinge on it.

- Great for shorter-term financing needs where you can repay quickly

- Avoids fixed loan structures if your cash flow varies month to month

- Potential for rewards or protections alongside the 0% offer

That said, these cards aren’t ideal for everyone. If the purchase is massive and will take years to pay off, a personal loan’s fixed rate might provide more predictability. Or if your credit isn’t strong enough for approval, you might face higher regular rates from the start. Still, for many mid-sized major purchases – think a few thousand dollars that you can tackle in 12 to 21 months – this route can feel like a financial breather.

Consider your spending habits too. If you’re someone who might be tempted to keep charging after the big purchase, the revolving nature of credit could lead to trouble. But used strategically, a 0% APR card transforms debt from a burden into a strategic tool. It’s about buying time without the immediate cost of interest, something personal loans rarely match in the early stages.

HELOCs: Unlocking Your Home’s Equity for Flexible Funding

If you own a home and have built up some equity, a home equity line of credit, or HELOC, might open doors that a personal loan simply can’t. Think of it as a revolving credit line secured by your property. You borrow what you need, when you need it, often at lower interest rates than unsecured personal loans because the lender has collateral.

This option particularly shines for home-related expenses. Renovations, repairs, or even adding value through upgrades – these are classic HELOC uses. Why? The rates tend to be variable but start lower, and you only pay interest on the amount you actually draw. It’s not a lump sum dumped into your account all at once like many personal loans; instead, you have a draw period where you can access funds flexibly, followed by repayment.

One aspect I find fascinating is how this shifts the risk-reward balance. Yes, your home is on the line if things go south, which makes it scarier than an unsecured loan. But for homeowners confident in their ability to repay, the potential savings on interest can be substantial. I’ve heard stories of families completing major kitchen overhauls or addressing urgent roof issues without draining savings or facing sky-high rates.

Lower rates and flexible access make HELOCs a powerful tool, but only when paired with realistic repayment plans.

Compared to personal loans, HELOCs often allow larger borrowing amounts tied to your equity rather than strict income or credit limits alone. Some lenders even offer small minimum draws, making them viable for more moderate projects too. Repayment terms can stretch longer, giving you room to breathe. However, variable rates mean your payments could fluctuate with the market, unlike the fixed predictability of most personal loans.

- Assess your home equity and current mortgage situation first

- Compare draw periods and repayment timelines across options

- Factor in closing costs and any fees that might apply

- Build a buffer in your budget for potential rate changes

Not every homeowner qualifies easily, and the process involves more paperwork – appraisals, title searches, the works. It’s slower than snapping up a personal loan online in a day or two. Plus, that home-at-risk element isn’t something to take lightly. If your income is unsteady or the expense isn’t home-related, a personal loan might feel safer emotionally, even if costlier.

Still, for the right person in the right situation, a HELOC can be a game-changer. It turns the value you’ve already built in your property into usable funds without forcing you into a rigid lump-sum structure. Just remember: this isn’t “free” money. Treat it with the same respect you’d give any loan, and it could help you build even more equity through smart improvements.

Private Student Loans: Targeted Funding for Education and Career Growth

When the major expense revolves around furthering your education or that of a loved one, private student loans often step up as a more specialized alternative. Personal loans can sometimes fund schooling if the lender allows it, but they’re not built for it. Student loans, especially private ones after maxing out federal options, come with features tailored to academic timelines and costs.

Higher borrowing limits are a big draw here. While personal loans might cap out around certain amounts, private student loans can cover the full cost of attendance – tuition, books, housing, you name it. This is crucial for expensive programs where a personal loan simply wouldn’t stretch far enough. Terms can extend longer too, aligning better with post-graduation earning potential.

Deferment and forbearance options provide another layer of protection that many personal loans lack. You might not have to start repaying while still in school or during tough times afterward. Of course, you should exhaust grants, scholarships, and federal loans first – those often carry better protections and lower rates. But when there’s still a gap, private options fill it without the generic constraints of a personal loan.

Education investments pay dividends over a lifetime, making specialized financing worth considering carefully.

I’ve always believed that borrowing for education should feel like an investment rather than just debt. Private student loans support that mindset by focusing on career-building expenses. Rates vary widely based on credit, and co-signers can help if needed. Yet, they lack some federal perks, so understanding the differences is key before signing on.

One subtle advantage? Lenders in this space often understand variable costs of different programs, from undergrad to advanced degrees. A personal loan might force you to borrow more broadly or face restrictions. With student loans, the purpose aligns perfectly, potentially leading to smoother approvals when education is the clear goal.

- Prioritize federal aid before turning to private options

- Compare lifetime borrowing caps and repayment flexibility

- Consider future earning potential in your field of study

- Watch for co-signer requirements or release policies

That doesn’t mean they’re risk-free. Variable rates can rise, and without federal forgiveness pathways, you’re on the hook. For non-education major purchases, this alternative doesn’t make sense at all. But when schooling is the driver, it often provides a more nuanced, purpose-built solution than a general personal loan.

When a Personal Loan Still Wins Out

Despite these strong alternatives, there are moments when a personal loan remains the smartest move. Debt consolidation stands out as a prime example. Combining high-interest credit card balances or multiple bills into one lower-rate loan can simplify your life and save money over time. The fixed payments bring predictability that revolving credit or variable HELOC rates might not.

Smaller, unexpected expenses also favor personal loans. A sudden vet bill or appliance failure might not justify opening a HELOC or applying for a student loan. Personal loans often fund quickly – sometimes the same or next day – with minimal fuss. No collateral means less risk to your assets, and many lenders accommodate a wide range of credit profiles, though better scores unlock better rates.

Flexibility is another plus. Use the funds for almost anything, from vacations to moving costs, without the restrictions some alternatives carry. No prepayment penalties on many mean you can pay off early if windfalls come your way. In uncertain times, that freedom can feel reassuring.

| Expense Type | Best Option Likely | Why |

| Home renovations | HELOC | Lower rates, larger amounts, home-tied purpose |

| Short-term purchase payoff | 0% APR Card | Interest-free period if repaid on time |

| Education costs | Private Student Loan | Higher limits, deferment options |

| Debt consolidation | Personal Loan | Fixed rate, single payment simplicity |

| Quick emergency under $5k | Personal Loan | Fast funding, no collateral |

Ultimately, the “best” choice depends on your unique circumstances. I’ve found that people who pause to compare not only rates but also terms, risks, and alignment with their needs end up making decisions they feel good about long-term. Rushing into any borrowing without that reflection can lead to regret.

Building a Stronger Financial Foundation Along the Way

Beyond picking the right tool for one expense, these conversations often highlight the importance of broader money habits. An emergency fund, even a small one, can reduce the need for borrowing altogether next time. Budgeting apps or simple tracking methods help spot patterns before crises hit. And improving your credit score opens doors to better rates across all options – personal loans included.

Perhaps the most valuable takeaway is this: knowledge reduces fear. Understanding these alternatives empowers you to negotiate from a place of confidence rather than desperation. Shop around, ask questions, and don’t settle for the first offer that comes along. Lenders want your business, and comparing can uncover hidden gems or better terms.

In the end, major purchases don’t have to derail your progress. Whether you lean toward a zero-interest card for its temporary relief, a HELOC for its power and potential savings, or a private student loan for education-specific needs, the goal remains the same – handle the expense without compromising your future financial health. Sometimes a personal loan fits perfectly. Other times, one of these paths leads to smoother sailing.

Take time to run the numbers for your situation. What feels manageable month to month? How does the total cost compare over time? Are there risks you’re comfortable with? Answering these honestly can steer you toward the option that not only solves the immediate problem but supports your bigger picture. And if you’re still unsure, talking with a trusted financial advisor never hurts – another set of eyes can spot angles you might miss.

Life throws big expenses at us when we least expect it. Having multiple tools ready means you’re not forced into suboptimal choices. Explore, compare, and choose with eyes wide open. Your wallet – and your peace of mind – will thank you.

Financial decisions like these evolve with your life stage, income, and goals. What works brilliantly today might need revisiting in a few years. Stay curious about new offers and changes in lending landscapes. The more informed you stay, the better equipped you’ll be when the next major purchase or surprise expense appears on the horizon.

Remember, borrowing is a tool, not a trap. Used thoughtfully, any of these options – personal loans or their alternatives – can help you move forward rather than hold you back. The key is matching the method to the moment with clear eyes and realistic planning.