I’ve been watching markets for years, and few things capture attention quite like the interplay between distant geopolitical sparks and immediate price movements on trading screens. Right now, that tension feels particularly sharp. Peace talks hover in the background while key waterways stay contested, leaving traders guessing about the next big swing.

The past few weeks have delivered a masterclass in how quickly sentiment can shift. Crude oil futures dropped sharply through May, yet certain physical benchmarks refused to fall as fast. Equities pushed to new records even as some commodity prices held firm. It’s the kind of environment where assumptions get tested daily, and patience becomes a rare trading skill.

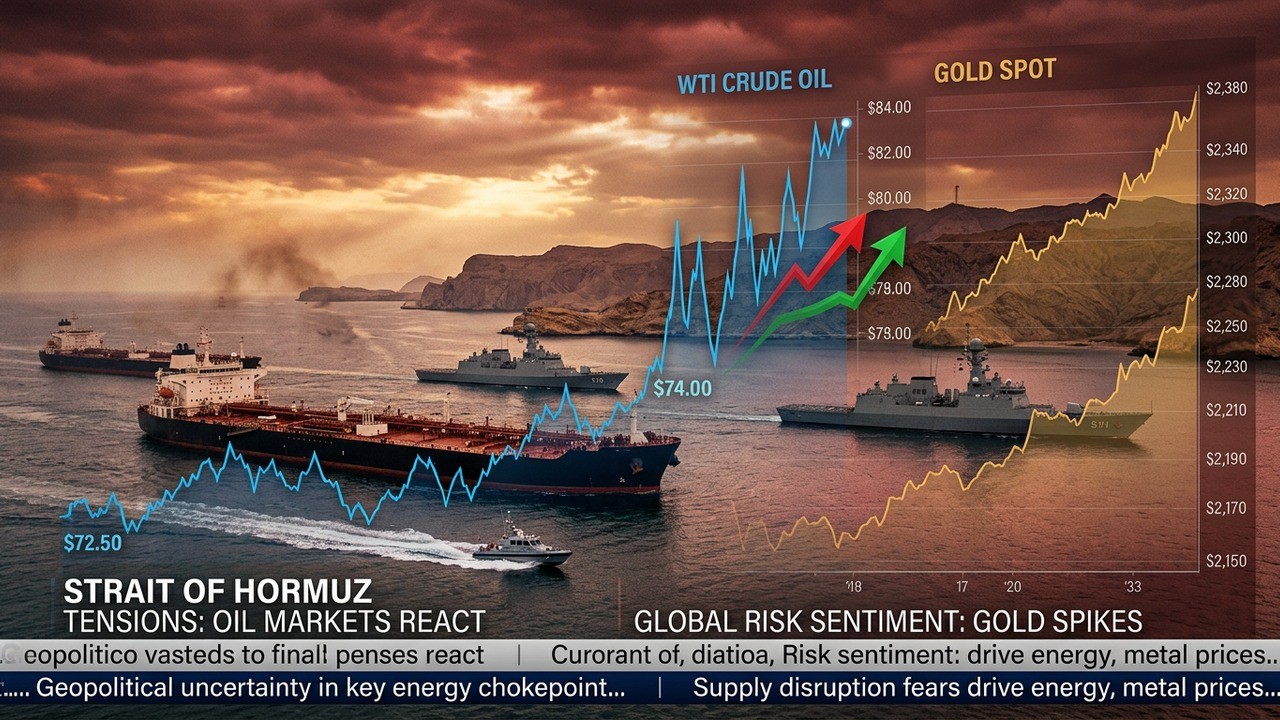

Understanding the Current Energy Market Squeeze

When you look at Brent crude front-month contracts inching higher after a tough month, it’s hard not to feel the weight of unresolved issues. The selloff in May came fast, driven largely by hopes of some diplomatic breakthrough. Yet here we are, with no firm agreement in sight and critical passages remaining restricted. That gap between rumor and reality keeps volatility alive.

Physical grades like Malaysian Tapis have shown more stubbornness, clinging to levels from recent months. Diesel prices in Singapore test lower supports but remain elevated compared to earlier baselines before regional flare-ups intensified. These discrepancies matter because they reflect real supply chain frictions that paper markets sometimes gloss over.

In my experience, when spot prices refuse to collapse alongside futures, it often signals underlying tightness that could reassert itself quickly if headlines turn negative again. Traders watching these spreads closely have an edge in anticipating the next leg.

Why the Strait Remains a Focal Point

The strategic importance of certain maritime chokepoints cannot be overstated. When passage through vital routes faces ongoing challenges, the ripple effects touch everything from refinery margins to consumer fuel costs worldwide. Current conditions suggest this situation may persist longer than many initially hoped.

Negotiating parties appear to face deeply entrenched positions, particularly around sensitive technical programs and regional influence. What began with expectations of rapid resolution has evolved into a more patient, and at times frustrating, process. Each side weighs significant risks before making concessions.

The parties find their positions on key security issues remain incompatible in the near term.

Recent political developments within one key nation add another layer of complexity. Reports of internal leadership tensions and power balances between different institutions suggest domestic dynamics could influence external bargaining stances. When civilian and security elements diverge in priorities, progress often slows.

Comments from international figures highlighting distinctions between military branches have raised eyebrows too. These nuances hint at factional differences that complicate unified decision-making. Reaching a durable understanding may require more time for internal alignments to occur.

Gold’s Role as a Barometer of Uncertainty

Precious metals have their own story in this environment. After a period of consolidation, gold managed a positive weekly close recently, respecting important support zones around the mid-four thousands. This resilience speaks volumes about underlying caution among investors.

Earlier in the crisis period, central banks adjusted holdings amid liquidity needs, contributing to price fluctuations. Now, as the situation drags on without clear resolution, the metal finds renewed interest as a store of value. It’s trading in ranges reminiscent of late last year, suggesting a return to familiar safe-haven patterns.

What strikes me is how consistently gold reacts to prolonged geopolitical stalemates. Even when equities climb, the yellow metal often finds buyers willing to pay up for perceived protection against tail risks.

- Respect for major support levels shows technical strength

- Central bank activity earlier created temporary selling pressure

- Current ranges align with pre-escalation periods of uncertainty

Equity Markets Defying the Headlines

Despite commodity swings and international friction, major stock indices in the US closed the week on a positive note. The S&P 500 extended its streak of weekly gains, sitting near record territory. Asian markets showed more mixed performance, reflecting regional differences in exposure.

This resilience raises interesting questions. Are investors pricing in eventual resolution? Or has the market simply grown accustomed to living with elevated background risks? Nine consecutive positive weeks suggest confidence remains intact for now, though futures point to continued caution mixed with optimism.

I’ve seen similar patterns before where bad news gets ignored until it can’t be. The key will be whether economic data and corporate earnings continue supporting valuations even as external pressures mount.

Bond Yields Reflect Shifting Expectations

Sovereign debt markets also moved this week. After declines, yields ticked higher across several curves. US two-year notes rose modestly while longer tenors showed more pronounced shifts. Australian and other regional benchmarks followed suit in places.

These moves could indicate reduced expectations for rapid policy easing if conflicts persist and energy costs remain sticky. Central banks face their own balancing acts between inflation risks from energy and growth concerns if disruptions worsen.

New Zealand’s case stands out with relatively stable short-term rates following recent policy signals and fiscal updates. Delayed tightening plans add their own flavor to the global mix.

| Market Segment | Recent Movement | Implication |

| US 2-Year Yield | Up 2bps to 4.04% | Modest repricing of near-term rates |

| US 10-Year Yield | Up 3bps to 4.47% | Longer-term uncertainty premium |

| Gold Weekly Change | +0.68% | Safe-haven demand returning |

Such tables help visualize how different assets respond in tandem or opposition during stress periods. The divergence between equities and yields deserves close watching in coming sessions.

Broader Geopolitical Context and Risks

Beyond the Middle East, other longstanding conflicts continue influencing global sentiment. Developments in Eastern Europe, including technological cooperation and reported incidents near borders, add layers of concern. Public statements from senior officials carry increasingly sharp tones, reminding everyone that peaceful resolutions remain elusive on multiple fronts.

Citizens should realize authorities have entered difficult territory. Be vigilant.

These words, while strong, reflect deep frustrations on all sides. When major powers feel their security interests are challenged, rhetoric can escalate quickly. Markets have largely shrugged off these warnings so far, but history shows complacency can be costly.

Drone technology proliferation and energy infrastructure targeting represent new chapters in modern conflict. The economic consequences extend far beyond immediate battle zones, affecting global supply chains and investment decisions.

What Investors Should Consider Moving Forward

In situations like this, diversification takes on renewed importance. Exposure to energy, defense, and precious metals can serve as partial hedges, though timing and sizing matter enormously. Over-concentration in any single narrative carries risks as new information emerges daily.

- Monitor physical versus futures price relationships for early warning signals

- Track internal political developments in key nations for negotiation clues

- Assess yield curve shifts as indicators of changing growth and inflation expectations

- Maintain balanced portfolios that can weather both positive and negative surprises

- Stay informed but avoid reactive trading based on unconfirmed rumors

Perhaps the most interesting aspect is how markets have adapted. Record equity highs alongside elevated energy prices suggest underlying economic strength in some regions. Yet the longer key passages remain contested, the greater the chance of broader impacts on inflation and consumer confidence.

I’ve always believed that successful investing in turbulent times requires equal parts analysis and emotional discipline. The current environment tests both. While some observers see potential for breakthroughs soon, others prepare for extended friction. Reality likely lies somewhere in between.

Potential Scenarios and Their Market Impacts

Let’s think through different paths forward without claiming certainty. A meaningful diplomatic step could ease pressure on energy prices relatively quickly, supporting risk assets and pressuring safe havens lower. Conversely, prolonged stalemate or renewed incidents might drive fresh spikes in volatility across commodities and bonds.

Hybrid outcomes seem most probable – partial agreements that leave core issues unresolved. In such cases, we might see choppy trading with periodic relief rallies followed by renewed selling on implementation doubts.

Equity leadership could rotate toward sectors less sensitive to energy costs while cyclicals face pressure. Technology and consumer staples have shown varying degrees of insulation in past episodes, though nothing is guaranteed.

Historical Parallels and Lessons

Looking back, previous disruptions in energy supply routes have produced varied outcomes depending on duration and severity. Short-lived events often led to quick reversals once resolved. Longer episodes reshaped industries, accelerated energy transitions, and left lasting marks on inflation expectations.

What feels different this time is the simultaneous occurrence of multiple global flashpoints. The interplay between regions adds complexity that pure historical comparisons struggle to capture fully. Central bank toolkits have also evolved, potentially altering transmission mechanisms.

Still, core principles remain. Markets hate uncertainty more than bad news itself. Clear communication and credible commitments tend to calm nerves faster than vague promises.

Broader Economic Implications

Higher sustained energy costs flow through to transportation, manufacturing, and household budgets. Depending on regional exposure and policy responses, this could either exacerbate inflationary pressures or tip fragile economies toward slower growth. The balance will differ country by country.

Emerging markets with high import dependence face particular challenges, while producers might see mixed benefits depending on their ability to actually export. Currency movements often amplify or dampen these effects.

For developed economies, the focus remains on whether wage growth and service sector strength can offset headwinds from commodities. Recent corporate reports suggest varying degrees of success in passing costs along.

Key Variables to Watch:

- Duration of waterway restrictions

- Success of diplomatic initiatives

- Central bank policy reactions

- Corporate earnings resilienceThese factors will likely dominate market narratives in coming months. Investors ignoring them do so at their peril.

Maintaining Perspective Amid the Noise

It’s easy to get caught up in daily headlines and minute-by-minute price action. Stepping back reveals that markets have absorbed significant shocks while continuing to function and, in some cases, reach new milestones. Human ingenuity and economic adaptability shouldn’t be underestimated.

That said, dismissing risks would be equally foolish. The combination of contested strategic assets and multifaceted international disagreements creates an environment where black swan events have higher probability than in calm periods.

My personal approach involves maintaining core long-term positions while keeping some dry powder for opportunistic adjustments. Regular portfolio reviews help ensure alignment with evolving realities without over-trading.

As negotiations continue and other conflicts simmer, the coming weeks promise more twists. Whether we see breakthroughs or further entrenchment remains to be seen. What matters most is staying informed, disciplined, and prepared for different outcomes.

The markets have shown remarkable capacity to climb walls of worry before. Whether that pattern holds depends on how quickly leaders can bridge current divides. Until clearer signals emerge, vigilance remains the watchword for investors worldwide.

Expanding on these themes, one cannot ignore how interconnected modern economies have become. A disruption in one region quickly transmits through financial channels, commodity flows, and confidence indicators. This reality makes isolated analysis nearly impossible and underscores the value of a global perspective.

Consider the role of alternative energy sources and technological advances in mitigating long-term risks. While not immediate solutions, investments in these areas have accelerated during past crises and may do so again. Policy support varies, but market forces often drive innovation when traditional supplies face question marks.

From a trading psychology standpoint, environments like this reward those who can tolerate uncertainty without abandoning sound principles. Emotional decisions based on fear or greed frequently lead to suboptimal results. Data-driven approaches combined with flexibility tend to fare better.

Looking ahead, seasonal factors, upcoming economic releases, and political calendars will intersect with the geopolitical backdrop. Each element deserves attention in its own right while never losing sight of the bigger picture.

Ultimately, the resilience we’ve observed so far offers hope but not guarantees. The path forward will be shaped by decisions made in multiple capitals, responses from market participants, and perhaps some luck in avoiding escalation. For now, the prudent course involves awareness, preparation, and measured optimism balanced with healthy caution.

This situation serves as a reminder that markets never operate in isolation from the real world. Geopolitics, economics, and human elements combine in complex ways that challenge even the most sophisticated models. Staying humble before that complexity might be the most valuable lesson of all.