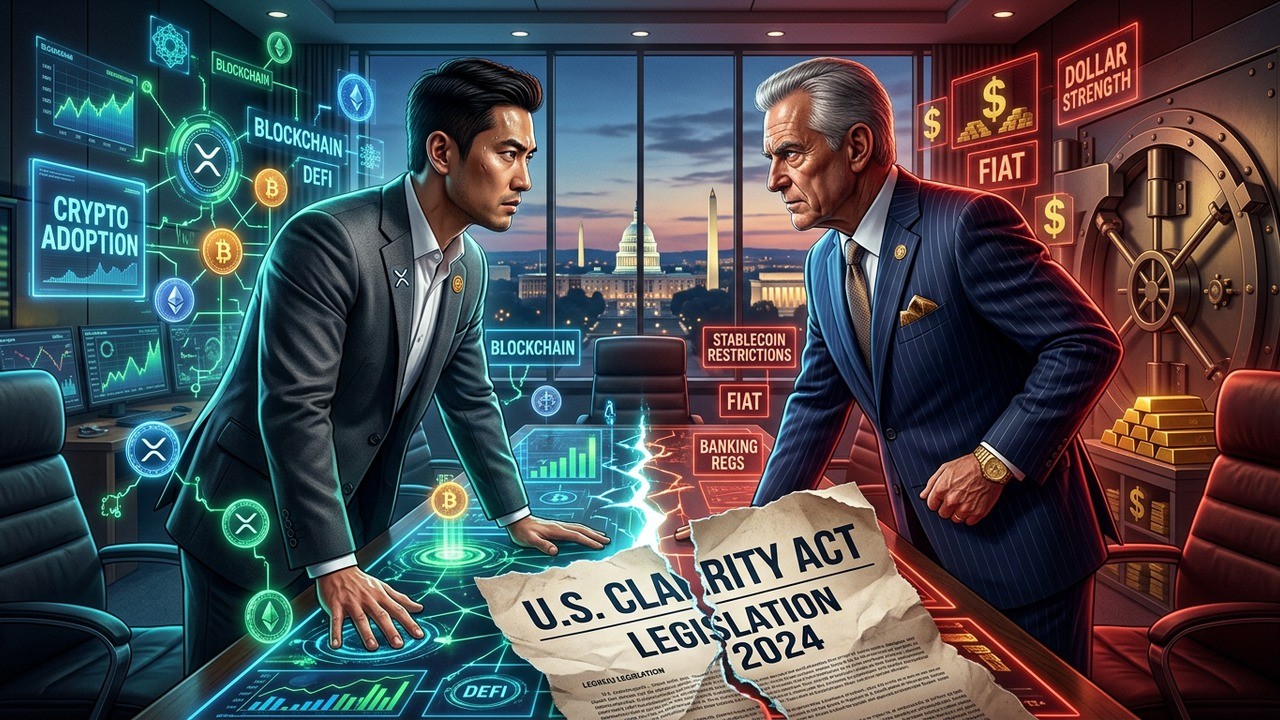

Imagine two titans of finance staring each other down, not in a boardroom brawl but through carefully worded statements, lobbying efforts, and public appearances that could determine the next decade of digital money. That’s exactly what’s happening right now between Ripple’s Brad Garlinghouse and JPMorgan’s Jamie Dimon. While most crypto enthusiasts are glued to volatile price movements, this behind-the-scenes struggle over the CLARITY Act might matter far more for the industry’s long-term survival and growth.

I’ve followed financial markets for years, and moments like this remind me that real change often happens away from the charts. The tension isn’t just personal—it’s a proxy war between emerging crypto innovators and the entrenched banking establishment. What they’re fighting about could either unlock massive institutional adoption or keep things tightly controlled by traditional players.

The High-Stakes Showdown Nobody’s Fully Appreciating

In the midst of market turbulence, with Bitcoin hovering around the low 60k range and altcoins taking hits, a legislative battle is brewing that carries huge implications. The CLARITY Act represents the most significant attempt yet to bring clear federal rules to digital assets in the United States. And at the heart of the debate stands one particularly thorny issue: whether stablecoins should be allowed to offer yields that compete with traditional bank deposits.

Garlinghouse has positioned himself as a champion for regulatory clarity, arguing that well-defined rules will allow crypto to flourish domestically rather than driving innovation overseas. His optimism about the bill’s chances has been notable, even as he acknowledges the complexities involved. On the flip side, Dimon has expressed clear reservations, signaling that the banking sector won’t simply roll over and accept changes that could erode their core funding advantages.

This isn’t your typical tech versus finance story. It’s deeper, touching on fundamental questions about money, power, and who gets to control the future of payments and value storage. Let’s break down what’s really at stake.

Understanding the Key Players and Their Motivations

Brad Garlinghouse didn’t become one of crypto’s most recognizable faces by accident. Leading Ripple through years of legal challenges, including a landmark case with securities regulators, he has consistently advocated for sensible oversight that doesn’t stifle innovation. His company has invested heavily in building bridges between traditional finance and blockchain technology, particularly through institutional-grade solutions.

From my perspective, Garlinghouse represents the forward-looking side of crypto—the one that believes American leadership in this space requires clear rules of the road. He’s pragmatic too, recognizing that not every provision will be perfect but seeing the bigger picture of legitimacy and growth.

The path forward requires balance, but clarity is essential for building sustainable infrastructure.

Jamie Dimon, meanwhile, sits at the helm of America’s largest bank. His views on crypto have evolved over time—from skepticism to cautious engagement as JPMorgan developed its own blockchain initiatives. Yet when it comes to certain aspects of proposed legislation, his stance remains protective of the traditional banking model. Banks rely on deposits as their lifeblood, lending them out to generate profits while offering relatively modest returns to customers.

The concern is understandable from their viewpoint. If stablecoins begin offering competitive yields without the same regulatory burdens, customer funds could migrate quickly. This potential shift represents a direct challenge to the deposit base that powers much of traditional lending.

The Core Dispute: Stablecoin Yields and Economic Reality

At the center of this conflict lies a single but powerful concept—yield-bearing stablecoins. These aren’t just digital dollars; they could function more like interest-bearing accounts that operate on blockchain rails. For crypto users and institutions, the appeal is obvious: seamless, programmable money that earns returns without leaving the ecosystem.

Proponents argue this innovation could democratize access to better yields and increase efficiency in capital allocation. Critics from the banking world see it as unfair competition that operates outside the heavily regulated deposit insurance and capital requirement framework that banks must follow.

The proposed compromise in the legislation attempts to split the difference. It aims to prevent stablecoins from offering what amounts to deposit-like interest while still allowing certain transaction-based rewards or other mechanisms. Whether this middle ground holds will likely decide the bill’s fate.

- Potential for massive capital flows into crypto-native products

- Risk of deposit flight from traditional banks

- Questions around consumer protection and anti-money laundering compliance

- Broader implications for monetary policy and financial stability

I’ve seen similar tensions play out in other industries during periods of technological disruption. The difference here is the speed and global nature of crypto, which makes the stakes feel particularly high.

Why This Fight Extends Far Beyond Two Companies

While the personalities involved draw attention, the real story is much larger. Success or failure of comprehensive digital asset legislation could influence everything from token classifications to how exchanges operate and how institutions allocate capital. For assets like XRP, clear commodity status could open doors to broader banking integration and new financial products.

Regulatory certainty has been the missing piece for many large players waiting on the sidelines. Without it, the industry faces continued uncertainty, enforcement actions, and the risk of talent and business migration to more welcoming jurisdictions. That’s why this particular bill carries so much weight.

Yet the irony isn’t lost on close observers. Even as banks voice opposition to certain provisions, some are actively building blockchain capabilities and exploring tokenization opportunities. This dual approach—participating while trying to shape the rules—highlights the complex relationship between incumbents and disruptors.

Traditional finance isn’t monolithic. Parts of it are embracing change while others fight to maintain established advantages.

Potential Market Impacts and Capital Flow Dynamics

Should yield restrictions remain in place, analysts suggest idle crypto capital might flow toward tokenized versions of traditional assets. Think government securities, money market instruments, or bank-issued digital deposits. This redirection could actually strengthen certain connections between crypto and regulated finance rather than creating pure competition.

In many ways, this outcome would represent a sophisticated win for the banking sector even if the bill passes. Crypto gets its regulatory framework, providing the legitimacy and predictability the industry craves. Meanwhile, the most disruptive competitive threats get blunted, channeling innovation in directions that complement rather than replace existing systems.

From an investor’s standpoint, understanding these nuances matters. Regulatory developments don’t always move prices immediately, but they shape the environment in which assets operate over months and years. Clarity could boost confidence, while prolonged uncertainty might weigh on sentiment.

Timeline Pressures and Political Realities

Legislation doesn’t happen in a vacuum. With midterm elections approaching, the congressional calendar is tightening. Bills need to navigate committee approvals, floor votes, reconciliation between chambers, and ultimately executive approval. Each step introduces opportunities for amendments or delays.

The stablecoin yield question isn’t the only sticking point, but it’s emerged as one of the most contentious. Lobbying efforts from both sides are intensifying, with banking groups mobilizing members to contact representatives while crypto advocates emphasize innovation and American competitiveness.

Recent comments from senators involved suggest ongoing work to refine the language. Bipartisan support exists in principle, but details continue to be negotiated. This is where the Garlinghouse and Dimon perspectives carry influence—not as direct negotiators but as symbols of their respective industries’ priorities.

Broader Implications for Tokenization and On-Chain Finance

Beyond the immediate yield debate, the CLARITY Act touches on foundational questions about digital property rights, smart contracts, and the integration of blockchain into mainstream financial infrastructure. Tokenization of real-world assets represents a multi-trillion dollar opportunity that many see as the next major growth phase.

If done right, clear rules could accelerate adoption across sectors—from real estate to commodities to securities. Companies positioned with strong infrastructure and compliance frameworks stand to benefit most. Ripple’s focus on cross-border payments and institutional solutions positions it uniquely in this landscape, regardless of exact yield outcomes.

- Establish clear jurisdictional boundaries between agencies

- Provide licensing frameworks for digital asset service providers

- Address custody, bankruptcy, and consumer protection standards

- Create pathways for responsible innovation while managing risks

These elements matter because they determine whether the United States leads or follows in shaping the digital economy. Other countries are advancing their own frameworks, creating a competitive global environment where capital and talent flow to the most predictable and supportive jurisdictions.

What a Compromise Might Look Like

The most likely path forward probably involves some version of the current compromise framework. Crypto gets the overarching regulatory structure it needs for growth and legitimacy. Banks secure protections around core deposit functions while potentially benefiting from increased activity in adjacent areas like tokenized assets.

This “both sides claim some victory” scenario is common in complex legislation. It rarely satisfies purists on either end but allows progress to continue. For market participants, even imperfect clarity often beats prolonged ambiguity.

Of course, there’s always the risk of delay or failure. If the bill stalls, it could reinforce narratives about regulatory uncertainty and push more activity offshore. That outcome would disappoint many who have advocated for years to bring crypto fully into the regulated mainstream.

Investment Considerations in an Uncertain Environment

For those navigating these developments, diversification remains key. Regulatory outcomes are inherently difficult to predict with precision, especially when powerful interests are involved. Focusing on projects with strong fundamentals, real utility, and adaptable business models makes sense regardless of short-term legislative twists.

Companies that have already built compliant infrastructure and demonstrated resilience through previous challenges may hold advantages. The emphasis on institutional adoption suggests that solutions facilitating capital movement between traditional and digital systems could see increased interest.

| Scenario | Likely Market Reaction | Key Beneficiaries |

| Bill Passes with Compromise | Positive sentiment, gradual institutional inflows | Infrastructure providers, compliant projects |

| Significant Delay | Continued uncertainty, potential short-term pressure | Offshore-friendly platforms |

| Strong Pro-Crypto Version | Stronger rally potential in affected tokens | Native stablecoin issuers |

These are generalizations, of course. Individual asset performance depends on many factors beyond any single bill. But understanding the regulatory backdrop helps frame bigger picture risks and opportunities.

The Human Element Behind Financial Evolution

There’s something fascinating about watching powerful figures like Garlinghouse and Dimon engage on these issues. Both are experienced leaders who have navigated multiple market cycles and regulatory shifts. Their public positions reflect not just company interests but deeply held views about how finance should evolve.

In my experience covering these topics, personality-driven narratives can oversimplify complex policy questions. Yet they do help illustrate the human stakes involved. Behind the technical language about yields and jurisdictions are real decisions that will affect how people send money, store value, and participate in the economy.

Perhaps the most interesting aspect is how this reflects broader societal shifts toward decentralized technologies while still needing guardrails and integration with existing systems. Finding that balance isn’t easy, but it’s necessary.

As the debate continues, staying informed about both the technical details and the political dynamics will be crucial. The outcome won’t just affect crypto prices in the near term—it could influence the structure of financial services for years to come. Whether you’re deeply invested in digital assets or simply curious about where money technology is heading, this fight deserves attention beyond the daily market noise.

The coming weeks and months will reveal whether compromise prevails or if entrenched positions lead to further delays. Either way, the conversation itself marks progress in bringing these important issues into mainstream policy discussion. The future of on-chain finance is being shaped right now, often in rooms far from the spotlight where most traders focus their energy.

What ultimately emerges from this process will say a lot about America’s willingness to embrace innovation while managing its risks. For an industry that has faced skepticism and regulatory headwinds, achieving meaningful clarity would represent a significant milestone. And for those paying close attention to the Garlinghouse-Dimon dynamic, it offers a window into the real forces determining crypto’s place in the broader financial landscape.

This isn’t just another policy debate. It’s a foundational discussion about the architecture of tomorrow’s money. How it resolves could influence everything from individual investment opportunities to the competitive position of the United States in global technology and finance. In that sense, even if the immediate market reaction seems muted, the long-term implications are profound.

Keep watching the legislative developments even when headlines focus elsewhere. Sometimes the most important moves happen quietly, away from the charts that capture most attention. The battle between these two influential perspectives may well determine whether crypto’s next chapter unfolds primarily in the US or elsewhere—and that choice carries consequences for all of us who believe in the potential of this technology.