Have you ever stopped to think about the invisible materials that keep modern industry running? One of them, sulfur, usually sits quietly in the background until something disrupts its flow. Right now, that something is happening on a scale that has analysts raising serious alarms about runaway prices and tightening supplies across the globe.

I’ve followed commodity markets long enough to recognize when a situation feels different. This one does. What started as regional logistics headaches has snowballed into a genuine supply shock for a critical industrial chemical most people never think about until it affects everything from fertilizers to metals processing.

The Quiet Crisis Brewing in Sulfur Markets

Sulfur isn’t glamorous. It doesn’t make headlines like oil or gold. Yet this yellow element serves as a foundational building block for countless essential processes. Produced mainly as a byproduct of oil refining and natural gas processing, its availability directly ties to energy production patterns. When those patterns face geopolitical interruptions, the effects cascade quickly.

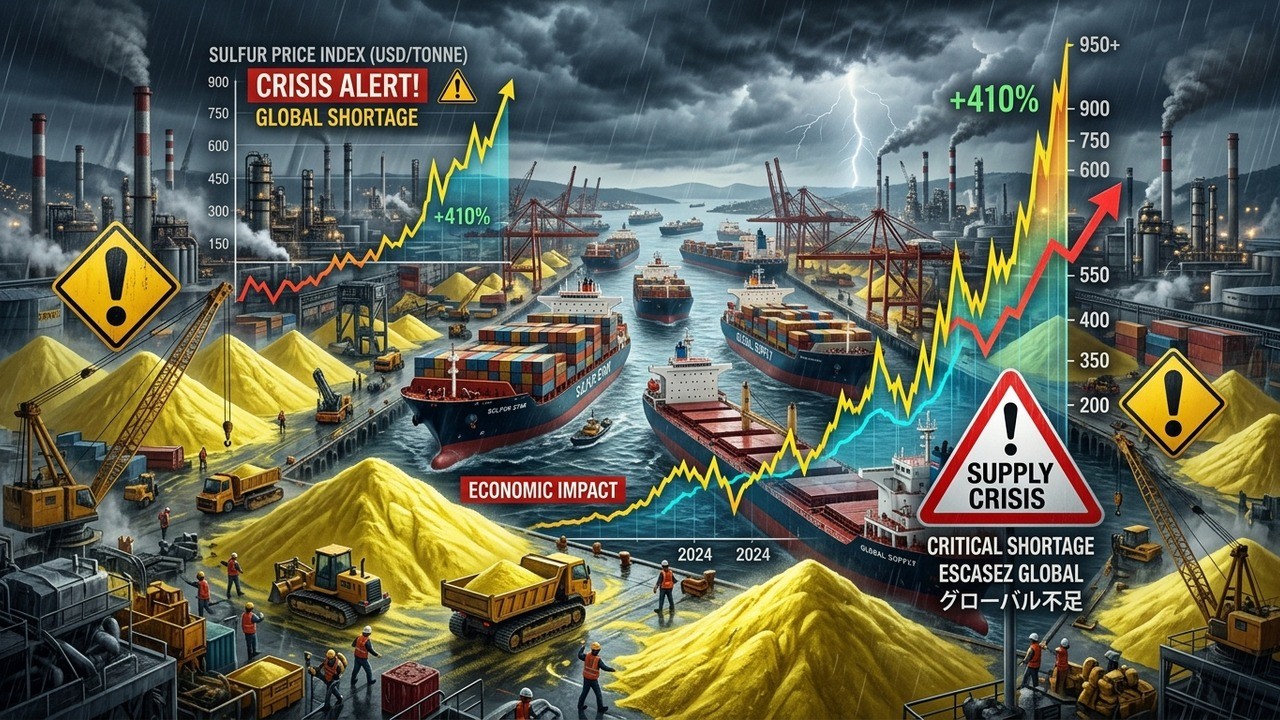

Current spot prices have climbed to roughly twelve hundred dollars per metric ton. For context, longer-term averages often hover well below two hundred dollars. That kind of jump doesn’t happen without major forces at work, and the combination of factors right now appears uniquely challenging.

What makes this particularly worrying is how much of the world’s seaborne sulfur trade depends on routes that have become unreliable. Roughly half of that trade normally passes through a certain strategic waterway in the Middle East. Add in significant volumes stuck in Central Asia due to export difficulties, and you start to see why pressure is building so intensely.

Understanding Sulfur’s Critical Role Across Industries

Before diving deeper into the current squeeze, it helps to appreciate why sulfur matters so much. The majority gets converted into sulfuric acid, often called the workhorse of the chemical industry. This acid plays indispensable roles in producing phosphate fertilizers that feed much of the world’s crops.

Mining operations rely heavily on it too, especially for extracting metals like copper and lithium that power everything from electric vehicles to renewable energy infrastructure. Even pulp and paper manufacturers use derivatives in their processes. When sulfur prices spike, those downstream costs don’t stay isolated for long.

In my view, people underestimate these connections. We talk about battery metals and green transitions, but the supporting chemistry often gets overlooked until prices remind us how interconnected it all really is.

The market is working through unprecedented supply shortages, and prices are inflecting accordingly.

That observation from analysts captures the moment perfectly. Demand destruction from higher costs has appeared in some sectors, particularly phosphates and paper production, but not uniformly or aggressively enough to offset the tightening supply picture.

Mapping the Major Supply Disruptions

The situation involves multiple pressure points hitting simultaneously. The most significant remains the maritime chokepoint affecting about fifty percent of globally traded seaborne sulfur. When flows through that route stall, the impact ripples through international markets almost immediately.

Another fifteen percent or so of supply finds itself effectively landlocked due to logistical blockades in a key Central Asian producer nation. Combined, these represent a substantial chunk of worldwide capacity. Layer on reduced exports from other major players due to ongoing conflicts and you get a recipe for persistent tightness.

China’s restrictions on sulfuric acid exports add yet another layer of complexity. Meanwhile, inventory buffers that normally provide cushion are being drawn down rapidly in certain regions. One contact familiar with the markets suggested only a couple weeks of safety stock might remain in key areas before more serious shortages emerge.

- Strategic waterway disruptions affecting half of seaborne trade

- Landlocked volumes in Central Asia due to export issues

- Geopolitical conflicts reducing output and shipments from key areas

- Export policy changes in major consuming and producing nations

- Rapid inventory liquidation in response to shortages

Each factor on its own would create headaches. Together, they create the potential for what some are calling runaway price risk. And because sulfur comes primarily as a refining byproduct, producers can’t simply ramp up output in response to higher prices the way they might with dedicated mining operations.

Why Demand Destruction Hasn’t Solved the Problem

Higher prices should theoretically curb demand, right? In practice, the response has been uneven. Certain industries feel the pain immediately and cut back. Others, particularly in metals where margins remain strong despite elevated input costs, continue operating and absorbing the increases.

Copper and lithium producers, for instance, operate in an environment where long-term demand outlooks justify paying up for necessary chemicals. This resilience in key segments prevents the market from rebalancing as quickly as many hoped.

I’ve seen this pattern before in other commodities. The pain threshold varies enormously by sector. What feels unsustainable to one buyer barely registers for another with different economics. That diversity keeps the pressure on longer than straightforward supply-demand models might predict.

The Geopolitical Dimensions at Play

You can’t analyze this situation without acknowledging the broader geopolitical tensions. Conflicts involving major energy and commodity producers create ripple effects that extend far beyond immediate battle zones. Attacks on infrastructure and sanctions complicate logistics in ways that markets struggle to price accurately in real time.

The reopening of blocked maritime routes would help, but even that wouldn’t provide an instant fix. Damaged infrastructure, backlogs of vessels, and the time needed to restart full operations mean elevated prices could persist for months even under optimistic scenarios.

This reality forces companies across value chains to rethink their sourcing strategies, inventory policies, and risk management approaches. Those who diversified suppliers or maintained larger buffers might weather the storm better than others caught flat-footed.

Industry-Specific Impacts Worth Watching

Fertilizer manufacturers face particularly direct exposure. Higher sulfur costs translate into elevated expenses for producing phosphate products that farmers rely upon. In some regions, this could eventually influence food production costs, though the transmission takes time.

Mining companies dependent on sulfuric acid for leaching processes are another key group. Strong metal prices provide some offset, but sustained high chemical costs still pressure margins and project economics over the longer term.

Even seemingly unrelated sectors like pulp and paper feel the pinch when input prices move this dramatically. The interconnectedness of industrial chemistry means few areas remain completely insulated.

Hormuz plus Kazakhstan plus broader regional factors equal significant price risk on the upside.

That blunt assessment from market observers underscores the precarious balance. Alternative sources and substitutes exist but come with their own limitations in scale, cost, and quality. Pyrite, for example, sees renewed interest as a potential sulfur source, yet it cannot fully replace traditional supplies in the near term.

Inventory Dynamics and Buffer Limitations

One temporary relief valve involves drawing down existing stocks. Certain countries with large domestic inventories have been liquidating to meet immediate needs. However, these measures have clear limits. Once buffers deplete, the market must confront the underlying supply deficits more directly.

Other regions hold ample supplies but face high transportation costs and slow mobilization timelines that limit their effectiveness as swing providers. This mismatch between available inventory and accessible inventory adds friction to any rebalancing effort.

Price inelasticity on the supply side compounds these challenges. Since most sulfur emerges as a byproduct rather than a primary product, economic incentives don’t translate directly into increased production volumes the way they would for dedicated commodities.

Longer-Term Implications for Markets and Policy

As this situation unfolds, several broader questions emerge. Could sustained high sulfur prices accelerate innovation in alternative chemistries or recycling technologies? Might governments consider intervention to protect domestic agricultural or industrial priorities?

Some analysts have raised the possibility of export restrictions in certain producing regions to safeguard local fertilizer production. Such moves, while understandable from a national security perspective, could further fragment global markets and create additional price pressures elsewhere.

For investors, companies with strong positions in sulfur-related segments or those able to pass through higher costs warrant closer attention. Conversely, businesses with heavy exposure and limited pricing power may face margin compression that affects their financial performance.

Potential Paths Forward and Scenarios

What might resolve this tightness? Improved geopolitical conditions allowing freer movement through key routes would certainly help. Increased output from unaffected regions, technological adaptations, or even a sharper economic slowdown reducing overall industrial demand could contribute to rebalancing.

Yet even positive developments would likely take months to fully work through the system. Markets don’t reset overnight after disruptions of this magnitude. Participants need to prepare for an environment of elevated volatility and structurally higher prices for the foreseeable future.

In my experience covering these markets, the most dangerous periods often come when multiple shocks overlap. The current combination of energy market tensions, logistical bottlenecks, and persistent demand in key sectors creates exactly that kind of challenging environment.

What Businesses and Investors Should Consider

For companies using sulfur or its derivatives, proactive risk management has become essential. This might involve securing longer-term contracts, exploring alternative suppliers despite higher costs, or investing in efficiency measures that reduce consumption intensity.

Investors tracking related sectors should monitor quarterly reports for mentions of input cost pressures and pricing power. Management teams that demonstrate strategic foresight in navigating these conditions could outperform peers struggling with the same headwinds.

Beyond immediate financial impacts, this situation highlights vulnerabilities in global supply chains that have developed over decades of optimization for efficiency rather than resilience. The lessons learned here may influence corporate strategies for years to come.

Stepping back, the sulfur market situation serves as a microcosm of larger forces reshaping commodity landscapes. Geopolitical risks, energy transitions, and industrial demands interact in complex ways that defy simple predictions. While the current price levels feel extreme, they reflect real constraints that won’t disappear quickly.

Whether this leads to lasting changes in how industries source and use critical materials remains to be seen. For now, participants across the value chain must navigate heightened uncertainty and elevated costs. The coming months will reveal how resilient different sectors prove when tested by these supply realities.

One thing seems clear: ignoring the foundational chemicals that enable modern production carries risks. Sulfur may not capture public imagination like flashier commodities, but its current troubles remind us how dependent our economies remain on reliable flows of even the most unglamorous inputs.

As analysts continue monitoring developments, the focus will likely stay on whether additional supply can reach markets before inventories run critically low. Until then, the potential for further price movement keeps everyone watching closely. The story of sulfur in 2026 might ultimately say more about global interconnectedness than about any single element alone.

Expanding on the agricultural angle, phosphate fertilizers directly influence crop yields across major growing regions. Any sustained increase in production costs could eventually filter through to food prices, though farmers and distributors often absorb initial shocks through various mechanisms. Still, the chain reaction potential exists and deserves attention from policymakers concerned with food security.

In mining, sulfuric acid enables efficient extraction of valuable metals essential for technology and energy infrastructure. Higher costs here don’t just affect company profits. They influence the pace and economics of projects critical to broader societal goals like electrification and decarbonization. The irony isn’t lost on observers watching green transition materials face headwinds from traditional industrial chemicals.

Logistics professionals face their own puzzles. Moving sulfur requires specialized handling due to its properties. When traditional routes close, finding viable alternatives involves not just transportation but regulatory compliance, safety protocols, and infrastructure compatibility. These hidden complexities multiply the effective impact of any surface-level disruption.

Looking historically, commodity markets have experienced similar tight periods before. What differentiates the current episode is the simultaneous nature of multiple large-scale interruptions combined with strong underlying demand in strategic sectors. Recovery paths that worked in past cycles might prove less effective this time around.

Market participants who approach the situation with flexibility and creativity may discover opportunities amid the challenges. Whether through substitution, process innovation, or strategic inventory management, adaptive responses often separate survivors from those who merely react.

Ultimately, this sulfur supply story reinforces a broader truth about global markets. No commodity exists in isolation. When one element faces extraordinary pressures, the effects touch far more than its direct users. Understanding these connections helps build better mental models for navigating an increasingly complex economic landscape.

The coming weeks and months will bring more data points as inventories dwindle and markets test new price levels. How different players respond will shape not just immediate outcomes but potentially longer-term industry structures. For anyone involved with industrial materials or broader economic analysis, keeping a close eye on these developments makes good sense.