Have you ever stared at your student loan dashboard only to feel completely lost? For millions of Americans, that feeling is becoming all too real right now. As we head into July 1, the landscape for federal student loans is shifting dramatically, and early reports suggest the transition is anything but smooth.

I’ve spoken with borrowers who describe the current system as frustrating at best and broken at worst. Technical hiccups, inaccurate estimates, and conflicting messages are creating unnecessary anxiety just when clarity matters most. This isn’t just another bureaucratic tweak – it’s a significant overhaul that will affect repayment options, monthly bills, and long-term debt relief for tens of millions.

Understanding the Upcoming July 1 Student Loan Changes

The changes coming into effect aren’t minor adjustments. New legislation is reshaping the available repayment plans, introducing restrictions on payment pauses, and requiring many borrowers currently on certain programs to switch to alternatives. For those who have been navigating the system for years, this means re-evaluating everything from monthly obligations to forgiveness timelines.

What makes this particularly challenging is the timing. Many people are still recovering from previous disruptions in loan servicing, and now another wave of complexity is arriving. The scale is enormous – over 42 million federal student loan borrowers hold more than 1.6 trillion dollars in debt. When systems struggle under normal conditions, big transitions like this can create real headaches.

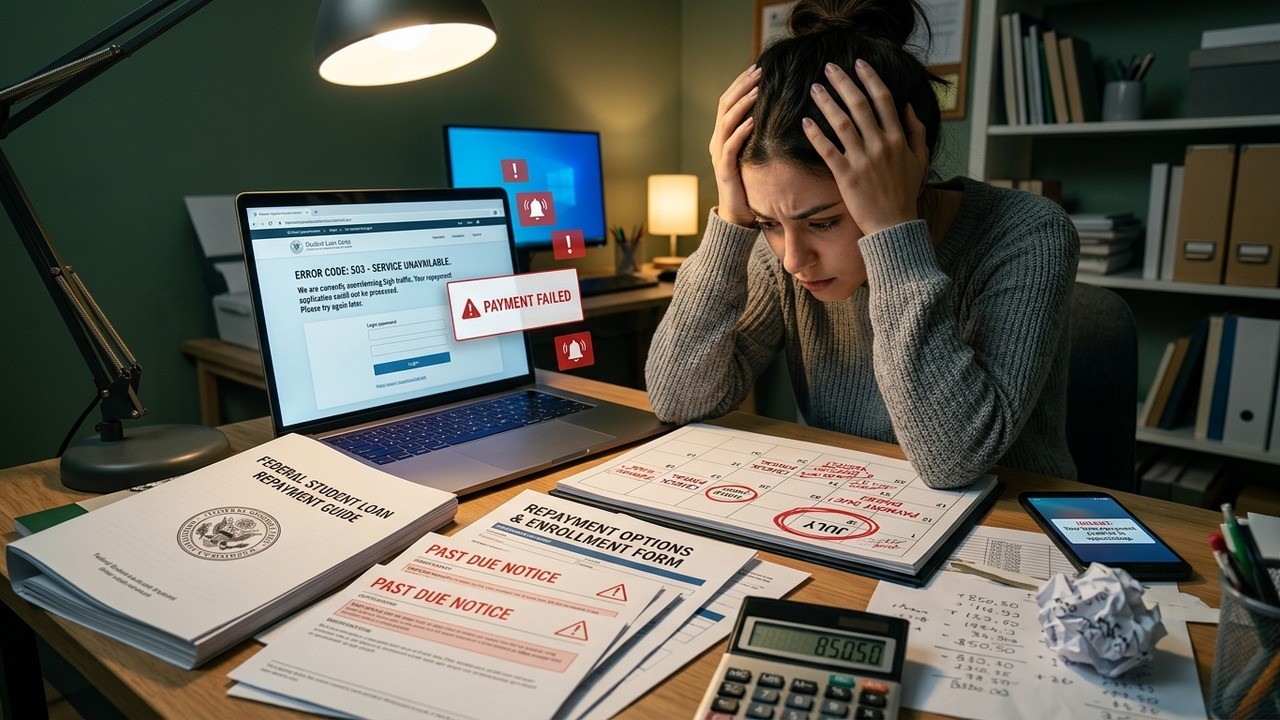

Technical Glitches Disrupting Borrowers Right Now

One of the most immediate issues involves the online tools borrowers rely on to make decisions. Several advocates working directly with loan holders report that certain repayment options simply aren’t appearing for eligible people. This isn’t a small inconvenience – it could force borrowers into more expensive plans without them realizing it until the bill arrives.

Consider the Pay As You Earn plan, often called PAYE. For many with older loans, this option caps payments at a lower percentage of discretionary income. Yet reports keep coming in that the application portal isn’t showing PAYE as available even when borrowers qualify. In my view, this kind of visibility problem undermines the entire purpose of offering flexible repayment choices.

The Department is executing significant, complicated repayment changes on tight deadlines, with new plans and increasingly important fine print. That would be a major challenge for even a well-resourced agency.

– Former Education Department official

Staff reductions at the Education Department over the past year have likely contributed to these growing pains. Managing complex systems with fewer people handling borrower support naturally leads to more errors slipping through. It’s a reminder that behind every policy change are real people trying to make the technology work under pressure.

Inaccurate Payment Estimates Creating False Expectations

Another troubling pattern involves the income-driven repayment calculator. Borrowers describe entering their information only to receive the same $50 monthly estimate regardless of their actual earnings. One person making sixty thousand dollars a year gets the same figure as someone earning over two hundred fifty thousand. That simply doesn’t add up.

These inaccurate projections can lead to poor choices. A borrower might select a plan based on the low estimate, only to discover later that their real payment is hundreds of dollars higher. The result? Budgets get thrown off, stress levels spike, and some people end up behind on payments they never expected.

- Older loans (before July 2014) typically require 15% of discretionary income under standard IBR

- Newer loans use a 10% rate, making accurate calculations essential

- Mismatched estimates ignore important details like family size and location-based income adjustments

The inconsistency raises questions about how thoroughly the systems were tested before rollout. When numbers don’t reflect reality, trust in the entire process erodes quickly. Borrowers deserve tools that provide reliable guidance, especially during such a major transition.

The Consolidation Trap and Potential Long-Term Consequences

Some borrowers are receiving messages urging them to consolidate their loans right now. On the surface, this might seem helpful, but it carries serious risks. Consolidation can reset progress toward forgiveness programs and limit access to certain repayment options under the new rules.

Once you combine multiple loans into one, you might lose valuable time already spent on income-driven repayment counts. For people close to qualifying for forgiveness, this could mean years of additional payments. The decision requires careful thought, yet the automated messages don’t always explain these trade-offs clearly.

Borrowers who consolidate after July 1 will also lose access to several student loan repayment plans under the new rules.

This highlights why personalized advice matters so much. Generic system prompts can’t replace understanding your specific situation – loan types, payment history, career trajectory, and family responsibilities all play important roles.

The SAVE Plan Transition and Upcoming Deadlines

Nearly seven million borrowers currently on the SAVE plan face a mandatory move to different options. The court-ordered end of SAVE means everyone needs to choose something new within roughly ninety days after July 1. Servicers will supposedly roll out these notifications gradually to avoid overwhelming the system, but backlogs already exist.

With over half a million applications pending for other plans, the timing feels particularly precarious. People who wait too long or encounter technical issues could face penalties, higher interest accrual, or collection actions. The pressure is real, and the support infrastructure appears stretched thin.

Practical Steps Borrowers Can Take Today

While the system sorts itself out, there are proactive measures worth considering. First, document everything. Take screenshots of error messages, inaccurate estimates, and confusing communications. This paper trail becomes invaluable if disputes arise later.

- Review your loan details on the official Federal Student Aid site regularly

- Calculate your expected payments manually using the formulas for different plans

- Contact your loan servicer directly rather than relying solely on online portals

- Consider consulting nonprofit counseling services that specialize in student debt

- Explore whether refinancing private options might make sense for your situation

I’ve found that staying organized and asking questions early prevents bigger problems down the road. Don’t assume the automated tools will always guide you correctly during this turbulent period.

What the Broader Changes Mean for Different Borrower Profiles

Not everyone will experience these shifts the same way. Recent graduates with smaller balances might find new plans more manageable, while those with larger debts accumulated over decades could face tougher choices. Public service workers pursuing forgiveness through specific programs need to pay extra attention to how consolidation or plan switches affect their timelines.

Parents who took out PLUS loans for their children’s education encounter unique rules and restrictions. The new framework adds another layer of complexity for families already juggling multiple financial priorities. Understanding where you fit in helps prioritize which aspects deserve immediate focus.

Looking ahead, the coming months will test both the Education Department’s implementation and borrowers’ resilience. Clear communication from officials could ease some tension, but based on current reports, many feel left to navigate murky waters alone. Perhaps the most important takeaway is this: stay informed, keep records, and don’t hesitate to seek help when the official channels fall short.

The student debt situation in America has always been complicated. These latest developments underscore how policy changes, technical limitations, and human circumstances collide in ways that affect daily budgets and future planning. While we can’t control every glitch in the system, we can control how prepared we are to respond when they appear.

Many borrowers have successfully managed transitions before by being persistent, asking detailed questions, and connecting with others in similar situations. Community forums, advocate organizations, and financial counselors often provide insights that official channels miss. Building that knowledge network proves valuable time and again.

The Human Side of Student Debt Challenges

Beyond numbers and portals lies the emotional weight many carry. Anxiety about rising payments can affect mental health, career decisions, and even family planning. I’ve heard stories of talented professionals delaying major life steps because loan uncertainty looms so large. These aren’t just financial issues – they’re deeply personal ones that ripple through every aspect of life.

Recognizing this human element matters. When systems fail to deliver accurate information, it adds insult to an already stressful burden. Policymakers and administrators would do well to remember that behind every application number stands a person trying to build a stable future while managing obligations from their past.

That said, some borrowers have found creative ways to stay ahead. Some negotiate directly with servicers, others adjust side hustles to create payment buffers, and many simply double-check every notification they receive. Small habits like these can make a meaningful difference when larger systems stumble.

Longer-Term Outlook and Forgiveness Considerations

While immediate glitches dominate headlines, the bigger picture involves how these changes influence paths to forgiveness. Different plans have varying timelines and qualification rules. Switching at the wrong moment could extend your repayment period significantly. Taking time to map out various scenarios – even roughly – helps avoid costly mistakes.

| Key Factor | Potential Impact |

| Loan Origination Date | Affects percentage of income used for payments |

| Current Plan Enrollment | Determines transition requirements after July 1 |

| Consolidation Decision | May reset forgiveness progress |

These variables interact in complex ways. What works perfectly for one borrower might create setbacks for another. Personalized evaluation beats one-size-fits-all advice, especially now.

As summer progresses, more details will emerge about exactly how the transitions will unfold. Servicers will likely issue specific instructions to SAVE plan participants at different points. Staying patient while remaining vigilant represents the best approach for most people.

Building Financial Resilience Beyond Loan Payments

Dealing with student loans effectively requires looking at the whole financial picture. Emergency funds, budgeting strategies, side income streams, and long-term investing all influence how manageable debt feels. When one part of the system falters, having strength in other areas provides crucial stability.

Some borrowers I’ve followed have used this period of uncertainty as motivation to review their entire money management approach. They’ve negotiated better terms on other debts, optimized tax situations, or explored income-boosting opportunities. Turning frustration into action often yields surprising benefits.

Ultimately, knowledge remains one of the strongest tools available. Understanding your rights, knowing available options, and recognizing when to push back against incorrect information can prevent many problems. The current glitches serve as a reminder that borrowers must advocate for themselves more than ever.

The road ahead contains challenges, but it also holds opportunities for clearer decision-making once initial technical issues get resolved. By approaching this transition thoughtfully and staying informed through reliable channels, borrowers can navigate toward more stable financial footing despite the bumps along the way.

Remember that you’re not alone in this. Millions face similar questions and concerns. Sharing experiences, learning from others’ mistakes, and celebrating small victories in managing debt helps create a sense of community and progress even when official systems fall short of expectations.