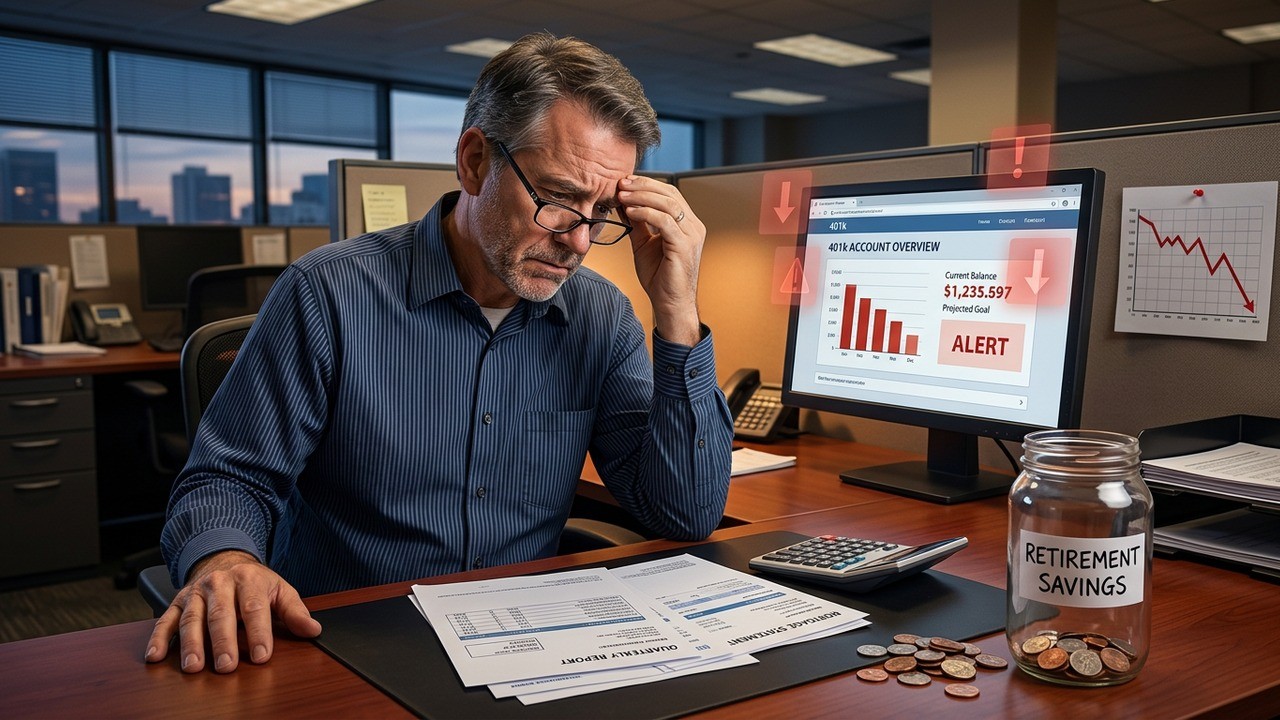

Have you ever paused mid-month, staring at your bank balance, and wondered how you’re supposed to keep up with everything while still thinking about the distant future? Millions of Americans are facing exactly that dilemma right now. New data reveals a troubling shift: roughly one in four workers have reduced their contributions to retirement accounts like 401ks. This isn’t some abstract statistic—it’s a real-time reflection of households feeling the pinch in their everyday budgets.

The modest drop in average contribution rates—from around 9.2% to 8.9%—might seem small on paper, but when you consider how widespread it is, the picture becomes clearer. This change affects people across various income levels, though it hits middle earners particularly hard. As living costs continue to climb, long-term savings are often the first flexible item on the chopping block.

A Growing Sense of Financial Pressure

I’ve followed economic trends for years, and moments like this always stand out as quiet warning lights on the dashboard. When workers start pulling back from automatic retirement deductions, it usually signals that immediate needs are outweighing future security. The data comes from a comprehensive look at workplace savings plans throughout 2025, showing not just lower percentages but also a slight dip in overall participation.

What makes this especially noteworthy is that it persists despite many companies implementing automatic enrollment and gradual increase features designed to boost savings. People are actively choosing—or feeling forced—to scale back. For those earning between fifty and one hundred fifty thousand dollars annually, the pressure appears most intense. These are the folks who often feel caught in the middle: too much to qualify for certain aids, yet not enough cushion against inflation and rising expenses.

Think about it. Mortgage or rent payments, groceries that cost noticeably more, fuel prices fluctuating with global events, and healthcare costs that never seem to stabilize. When your paycheck stretches thinner each month, contributing extra to a retirement account can feel like a luxury rather than a necessity. I’ve spoken with friends in similar situations, and the common thread is always the same: “I’m just trying to make it through the month.”

The Human Side of the Numbers

Behind every percentage point lies real people making difficult choices. A vice president at a financial health organization put it well when noting that daily survival makes it tough to prioritize decades-ahead goals. This resonates deeply. When you’re juggling bills and perhaps even helping family members, the idea of locking money away feels distant.

When you are struggling day to day, it’s hard to focus on your long-term goals.

– Financial health expert

This sentiment captures the mood for many middle-income households. The affordability crisis isn’t just a headline—it’s the reason more people report higher financial stress compared to previous years. Surveys show nearly half of Americans feeling more strained than twelve months earlier. That kind of widespread anxiety doesn’t appear overnight; it builds from sustained pressures on household budgets.

Employers should take note too. Financial worries among staff don’t stay contained to personal life. They can affect focus at work, overall morale, and even decisions about staying with a company. Smart organizations are beginning to recognize that supporting employee financial wellness today helps protect productivity and retention tomorrow.

Broader Trends in Retirement Behavior

This reduction in contributions doesn’t exist in isolation. Other indicators point to similar stress. Loan activity within retirement plans has risen significantly over recent years. People are borrowing against their future to cover present needs, a pattern that carries its own risks and costs.

Hardship withdrawals have also reached notable levels in some major plan administrator reports. Changes in regulations years ago made it somewhat easier to access these funds without first taking a loan, which may have contributed to higher activity. While such options provide necessary flexibility during tough times, frequent use can seriously undermine retirement readiness.

- Contribution rates declining across many plans

- More workers opting for loans from their accounts

- Increased hardship distributions in certain studies

- Slight drop in overall participation rates

These behaviors suggest a population that’s adapting to economic realities rather than building buffers. The gender gap in savings rates remains, with men contributing a bit more on average than women, though both groups show caution. Differences across ethnic groups also appear in the data, highlighting how financial challenges affect communities unevenly.

Why Middle-Income Earners Feel It Most

The squeeze on middle earners deserves special attention. They often face high housing costs, education expenses for children, and healthcare premiums that consume large portions of income. Unlike lower earners who might access certain safety nets or higher earners with more discretionary funds, this group frequently absorbs shocks without much margin.

Automatic features in retirement plans were supposed to help overcome inertia and behavioral biases. Yet when the math simply doesn’t work, even well-designed systems meet their limits. People adjust contributions downward because they need the cash flow now. This practical response reveals deeper issues in cost of living that policy discussions often overlook.

In my view, this trend should prompt a broader conversation about wage growth, inflation impacts, and housing affordability. Retirement security depends not just on individual discipline but on an economic environment where saving feels feasible rather than sacrificial.

Potential Long-Term Consequences

If this pullback continues, the effects could compound over decades. Compound interest works powerfully in both directions—reducing contributions early means significantly smaller nest eggs later. For many, this could translate to working longer, downsizing retirement plans, or relying more heavily on social security systems already facing their own pressures.

Consider a worker in their forties who trims contributions by just one percentage point. Over twenty years, with market returns, that seemingly small change represents tens of thousands of dollars. Multiply that across millions of people, and you see why analysts watch these figures closely. The ripple effects touch everything from consumer spending to government fiscal planning.

Financial stress today influences engagement, productivity, and retention at work.

– Workplace platform analysis

Businesses have a stake here. Healthier personal finances often lead to more engaged employees. Some companies respond with enhanced financial education, matching contributions, or other wellness programs. Yet these efforts can only go so far if broader economic conditions remain challenging.

Demographic Differences in Savings Patterns

The data also shows variations worth examining. Savings rates differ by gender and ethnicity, reflecting diverse economic experiences. Asian and White workers tend to have higher average contribution percentages, while Black and Latino workers show lower rates alongside higher loan usage from retirement accounts. These disparities invite thoughtful discussion about systemic factors, access to information, and cultural approaches to money management.

Rather than assigning blame, recognizing these patterns helps tailor better support systems. Financial literacy programs, culturally relevant advice, and workplace policies that acknowledge different household structures could make meaningful differences. The goal remains helping everyone build security regardless of background.

| Group | Average Savings Rate | Loan Activity Note |

| Men | Higher than women | Varies |

| Women | Lower on average | Varies |

| Asian Americans | Highest | Data limited |

| White Americans | Strong | Lower loan use |

| Black Americans | Lower | Higher loan use |

| Latino Americans | Lowest | Higher loan use |

Understanding these nuances prevents one-size-fits-all solutions. Effective strategies meet people where they are, addressing specific barriers each group faces.

Navigating Uncertainty in Today’s Economy

Global events continue influencing domestic costs. Energy prices, supply chain issues, and geopolitical developments all play roles in household budgets. Workers sense this instability and adjust accordingly. Cutting retirement contributions represents one rational, if unfortunate, response to perceived risk.

Perhaps the most interesting aspect is how resilient many people remain despite these pressures. They continue working, adapting, and seeking ways to provide for their families. That determination deserves recognition even as we highlight the challenges. The question becomes how society can create conditions where saving for tomorrow doesn’t feel impossible today.

Personal finance experts often recommend reviewing budgets carefully, seeking side income, or negotiating bills. While valuable, these tips work best within a stable economic framework. When foundational costs rise faster than wages, even diligent savers find themselves making trade-offs.

What Individuals Can Do Right Now

While systemic changes take time, personal steps still matter. Start by examining your full financial picture. Track spending for a month to identify leaks. Consider whether contribution cuts are truly necessary or if small adjustments elsewhere could free up funds. Even maintaining current levels prevents further erosion of retirement potential.

- Assess your monthly cash flow honestly

- Prioritize high-interest debt reduction where possible

- Explore employer matches—they’re essentially free money

- Build or maintain an emergency fund to avoid retirement loans

- Seek professional financial guidance tailored to your situation

These actions won’t solve everything, but they empower better decisions. Small consistent efforts compound just like investment returns. The key lies in balancing present needs with future security without burning out in the process.

Looking Ahead: Reasons for Cautious Optimism

Despite concerning trends, not all signals point downward. Some workers maintain strong savings habits. Innovation in financial products continues, offering new tools for managing money. Policy discussions around retirement security occasionally gain traction. The adaptability of the American workforce remains impressive.

Yet ignoring the warning signs would be unwise. Reduced 401k activity, rising loans, and increased stress levels suggest underlying fragility. Addressing root causes—like housing affordability, healthcare costs, and wage stagnation—could help restore confidence in long-term planning.

In my experience following these topics, the most successful periods economically occur when everyday people feel secure enough to save and invest comfortably. Rebuilding that sense of stability benefits everyone, from individual families to the broader economy.

This situation calls for honest reflection rather than panic. Workers cutting contributions aren’t being irresponsible—they’re responding to real pressures. The challenge for leaders, businesses, and communities involves creating pathways toward greater financial resilience. Until then, many will continue making the difficult but understandable choice to prioritize today over tomorrow.

As we move forward, keeping an eye on these retirement savings trends offers valuable insight into overall economic health. They reveal not just numbers, but the lived experiences of millions trying to balance dreams of retirement with the realities of current costs. Understanding this dynamic represents the first step toward meaningful improvements.

The coming months and years will test how effectively we address these issues. Will contribution rates stabilize or continue declining? How will markets and policy respond? For now, the data serves as an important reminder: financial security requires both personal effort and supportive economic conditions. Ignoring either leaves too many people vulnerable.

Ultimately, each of us plays a role—whether as employees managing our own plans, employers supporting staff, or citizens advocating for sensible policies. By acknowledging the pressures revealed in these latest figures, we position ourselves better to tackle them constructively. The future of retirement in America depends on how thoughtfully we respond to signals like this one.

Expanding on this further, it’s worth considering how different life stages influence these decisions. Younger workers might feel they have time to catch up later, while those approaching retirement age face more immediate concerns about adequacy of savings. Each group navigates unique pressures, yet all contribute to the overall trend we’re observing.

Family dynamics also play a significant part. Many households support aging parents or help adult children, stretching resources thinner. Multi-generational financial responsibilities add complexity that traditional retirement models didn’t always anticipate. This reality requires updated approaches to planning that account for these extended obligations.

Education around investing and compound growth remains crucial. Too many people underestimate how early reductions affect outcomes decades later. Clear, accessible information can empower better choices even within constraints. However, information alone proves insufficient without addressing affordability fundamentals.

Market volatility adds another layer. When account balances fluctuate dramatically, some workers lose faith in the system or reduce contributions during downturns. Behavioral finance teaches us that emotions heavily influence money decisions. Designing plans and policies with human psychology in mind could improve outcomes.

Considering all these factors together paints a complex but important portrait of American financial life in the current era. The one-in-four statistic isn’t just data—it’s a call to examine how we structure work, compensation, benefits, and economic opportunity. Getting this right matters for individual wellbeing and collective prosperity.

As discussions continue, let’s remember the people behind the percentages. Their choices reflect both personal circumstances and larger forces. By fostering empathy alongside analysis, we stand a better chance of developing solutions that truly help families build lasting security. The path forward requires honesty about challenges and creativity in addressing them.