Have you ever wondered why something as technical as stablecoin rules could spark one of the most intense lobbying battles in Washington? I certainly did when I first dug into the story. What started as a crypto regulation bill has turned into a raw contest over the future of money itself.

Banks aren’t just mildly concerned. They’re pulling out all the stops, flooding Senate offices with thousands of letters in a matter of days. At the center of this storm sits one specific issue: whether stablecoins should be allowed to pay yield to their holders. It might sound like inside baseball, but the implications stretch far beyond digital assets.

The Hidden Battle That’s Really About Competition

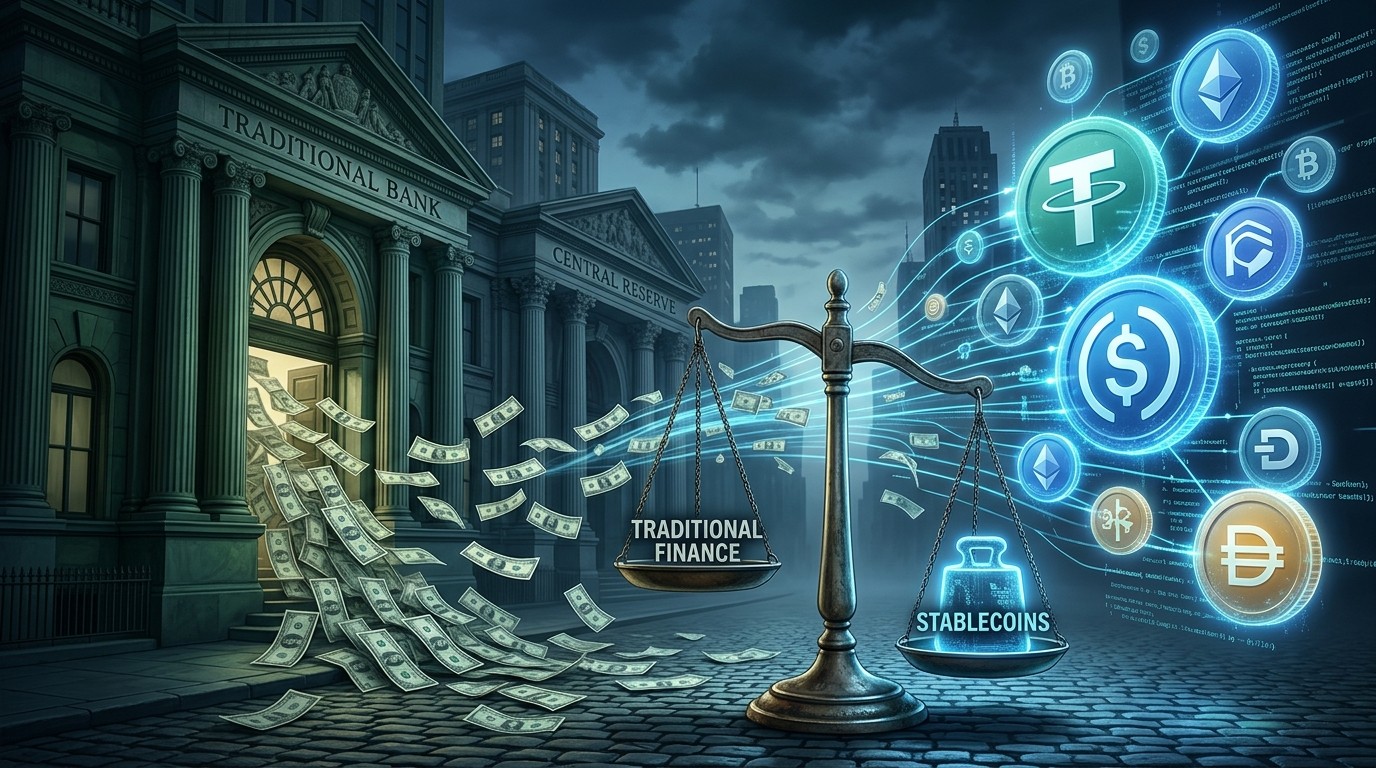

Picture this. You have your savings sitting in a traditional bank account earning next to nothing. Meanwhile, a digital dollar on the blockchain offers stability plus a real return. Suddenly, the comfortable world of banking faces a serious challenger. That’s the essence of what’s happening with the CLARITY Act.

In my view, this fight reveals how far crypto has come. No longer a niche speculation play, it’s now stepping directly onto banking’s turf. And the established players aren’t happy about it. The American Bankers Association didn’t mobilize like this over some abstract principle. They see a genuine threat to their core business model.

Let’s break it down step by step so you can see exactly why this matters and what’s really at stake for everyday people who use both traditional finance and crypto.

Understanding Stablecoins and the Yield Question

Stablecoins are digital tokens designed to maintain a steady value, usually pegged one-to-one with the US dollar. They’re backed by reserves like cash or short-term government securities. Those reserves naturally earn interest because that’s how money markets work.

The big debate is simple on the surface but complex underneath: should the issuers of these stablecoins pass some of that earned interest back to the people holding the tokens? In other words, can your digital dollars earn yield while remaining perfectly stable and easily transferable on blockchain networks?

This combination — stability, convenience, and return — creates something incredibly powerful. It’s like having a bank account that works at internet speed with potentially better rates. And that’s precisely why banks are concerned.

The real question isn’t whether technology can improve money. It’s whether the old system will let the new one compete fairly.

From what I’ve observed following these developments, yield-bearing stablecoins represent more than just another crypto feature. They could become a genuine alternative to traditional savings accounts. People could hold value outside the banking system while still earning competitive returns.

How This Threatens the Traditional Banking Model

Banks don’t just hold your money. They use deposits as cheap funding to make loans at much higher rates. The difference, called the net interest margin, is how they make most of their profit. It’s a model that’s worked for generations.

But what happens when customers have an attractive alternative? If significant money flows from bank accounts into yield-bearing stablecoins, banks face what’s known as deposit flight. They’d have to pay higher rates to keep customers, squeezing their margins and potentially limiting their ability to lend.

This isn’t theoretical. In a world of high interest rates, the math becomes even more compelling for users. Why accept minimal returns in a bank when a stable digital alternative might offer more? Banks understand this dynamic better than anyone, which explains their intense focus on this one provision.

- Deposits provide stable, low-cost funding for banks

- Yield on stablecoins comes from the same type of safe assets banks use

- Blockchain offers faster, cheaper transfers than traditional rails

- Users gain more control and potentially better returns

I’ve spoken with people in both industries, and the tension is palpable. Traditional finance sees this as an uneven playing field, while crypto advocates view it as innovation finally challenging outdated systems.

The Tillis-Alsobrooks Compromise Explained

After months of deadlock, senators crafted a middle-ground approach. The compromise aims to prevent purely passive yield that mimics bank deposits too closely while still allowing some activity-based rewards tied to actual usage of the stablecoin.

It’s an attempt to thread a very fine needle. Block the features that would make stablecoins direct deposit substitutes, but don’t kill the potential for innovation entirely. Crypto supporters accepted this as a necessary concession to advance the broader bill. Banks, however, believe it doesn’t go far enough.

The specific language defining what counts as prohibited passive yield versus permitted rewards has become the primary battleground. Small wording changes could have massive real-world effects on how competitive stablecoins can actually be.

Inside the Banking Industry’s Lobbying Push

The scale of the response caught many by surprise. More than 8,000 letters in less than a week targeting Senate offices. This wasn’t a casual objection. It was a coordinated, high-priority campaign focused laser-like on the yield provision.

Banks argue for regulatory parity. If something functions like a deposit, they say, it should face similar rules and oversight. There’s logic to this position from a stability perspective. Yet the intensity suggests competition is the deeper driver.

Perhaps what’s most telling is that banks aren’t trying to kill the entire bill. They largely accept many other aspects of crypto regulation. Their fight is surgical — aimed at protecting their deposit base above all else.

This isn’t about being anti-crypto. It’s about preserving a system that has funded economic growth for decades.

— Perspective often heard from banking representatives

In reality, both sides have valid points. Innovation needs space to breathe, but financial stability matters too. The challenge lies in finding the right balance without stifling progress or creating new risks.

What This Reveals About Crypto’s Evolution

Step back for a moment. The fact that traditional banks are engaging at this level shows crypto has matured. It moved from the fringes into a position where it can meaningfully challenge established financial giants. That’s no small achievement.

Yield-bearing stablecoins represent the collision point where new technology meets old infrastructure. The fight over the CLARITY Act isn’t just legislative theater. It’s the opening chapter in a longer story about how money, payments, and value storage will work in the coming decades.

I’ve followed financial markets for years, and moments like this feel historic. We’re watching incumbents recognize a genuine disruptor and respond accordingly. How lawmakers navigate this will set precedents far beyond stablecoins.

Implications for Users and the Broader Market

For everyday crypto users, the outcome matters tremendously. If rules allow meaningful yield, stablecoins could become much more attractive places to hold dollar-value assets. Think seamless transfers, global accessibility, and actual returns.

Conversely, tight restrictions might keep stablecoins primarily as trading tools and payment rails rather than full deposit alternatives. The difference affects practical choices millions of people make about where to park their money.

- Greater yield potential could accelerate mainstream adoption

- Banks might innovate in response, benefiting consumers overall

- Clear rules could reduce uncertainty and attract more institutional players

- The competitive pressure might improve services across both sectors

Markets are watching closely too. Legislation like the CLARITY Act influences not just prices but the entire infrastructure supporting crypto. Positive resolution could unlock significant growth, while prolonged uncertainty creates headwinds.

The Bigger Picture: Redefining Money in the Digital Age

This conflict goes beyond one bill or one provision. It’s about who controls the future of money. Banks have dominated this space for centuries through regulation, infrastructure, and trust. Crypto offers an alternative vision built on transparency, programmability, and borderless access.

Neither side has a monopoly on virtue here. Traditional banking has powered economic development and provided stability. Crypto brings innovation, inclusion, and efficiency gains. The ideal outcome probably involves elements of both rather than total victory for one.

Consider how payments have already changed. Instant transfers, lower fees in many cases, and 24/7 availability are becoming expectations rather than luxuries. Stablecoins accelerate these trends while introducing new possibilities around yield and composability in decentralized finance.

Following the money, as they say, explains a lot. Banks depend on deposits for their business model. Protecting that base is rational self-interest. At the same time, preventing beneficial innovation to shield incumbents would ultimately hurt consumers and economic progress.

Potential Outcomes and What Comes Next

Several paths lie ahead. The compromise language might hold, offering a pragmatic middle way. Banks could succeed in tightening restrictions further. Or, with enough support, the rules might tilt more toward allowing competitive yield features.

Each scenario carries different consequences for the bill’s passage and the crypto industry’s development. Lawmakers face difficult choices balancing innovation, stability, consumer protection, and industry interests.

One thing seems clear: this won’t be the last battle. As technology continues advancing, similar tensions will arise in other areas — custody, lending, payments, and beyond. How we resolve this current fight will influence future ones.

Why This Matters to Regular People

You don’t need to be a Wall Street executive or crypto trader to care about this. Where you keep your money, how much return you earn, and how easily you can move it affects daily life. Better options ultimately benefit everyone, even if they challenge comfortable existing arrangements.

I’ve always believed competition drives improvement. When banks face real alternatives, they tend to innovate — offering better rates, services, or convenience. Users win in that scenario. The key is ensuring the competition happens on a level playing field with appropriate safeguards.

Stablecoins already serve important roles in trading, remittances, and as a bridge between traditional and digital finance. Enhancing their utility through thoughtful yield rules could expand those benefits significantly.

Key Considerations for the Future

- Consumer protection remains essential regardless of the technology

- Reserve transparency and auditing build necessary trust

- Clear regulatory frameworks reduce risks while enabling growth

- International coordination will matter as stablecoins cross borders

Looking ahead, the integration of crypto features into traditional finance seems inevitable. The question is whether it happens through collaboration or continued conflict. The CLARITY Act represents an important test case for that dynamic.

In my experience covering these intersections, the most successful outcomes come when both sides find ways to coexist rather than trying to eliminate the other. Banks can adapt and partner with new technologies. Crypto projects can incorporate lessons from centuries of financial regulation.

The lobbying battle over stablecoin yield captures this tension perfectly. It’s technical on the surface but fundamentally about power, money, and control in the evolving financial landscape. As the Senate considers the CLARITY Act, the decisions made will echo for years to come.

Whether you’re deeply involved in crypto or simply curious about where banking is headed, staying informed on these developments matters. The rules being written today will shape the financial tools available tomorrow.

This situation reminds us that progress rarely happens without resistance. The real test lies in whether that resistance leads to better, safer innovation or simply entrenches outdated advantages. Only time — and the final shape of legislation — will tell.

One thing is certain: the conversation about stablecoins and banking has moved from the edges into the mainstream. And that’s a sign of how much has already changed in the world of money.