Have you ever watched the markets react in real time to a single piece of geopolitical news and wondered how interconnected everything truly is? Just when it seemed like tensions in the Middle East might keep energy prices elevated, a surprising development has shifted the narrative. The United States has decided to temporarily waive sanctions on Iranian oil sales, opening the door for more crude to potentially flow back into global markets.

This move comes after initial talks between high-level officials, and it’s already sending ripples through commodity prices and equity markets alike. As someone who follows these developments closely, I’ve seen how such decisions can quickly alter investor sentiment, sometimes in ways that catch even seasoned traders off guard. Today, let’s dive deep into what this all means for everyday investors, the energy sector, and those heavily positioned in technology stocks.

Geopolitical Breakthrough: Temporary Relief on Iran Sanctions

The recent agreement to waive sanctions for a 60-day period marks a notable de-escalation following months of heightened conflict. Reports indicate that discussions in Switzerland involved key figures aiming to clarify terms for potentially ending broader hostilities. With Iranian officials engaging in further talks, including a presidential visit to neighboring Pakistan, there’s cautious optimism that nuclear monitoring could resume under international oversight.

From my perspective, this kind of diplomatic progress is refreshing in a world where uncertainty often dominates headlines. It doesn’t solve every underlying issue overnight, but it does provide breathing room for markets. Oil prices, which had been buoyed by supply concerns, slid further below the $80 mark as traders began pricing in the possibility of additional Iranian barrels reaching international buyers.

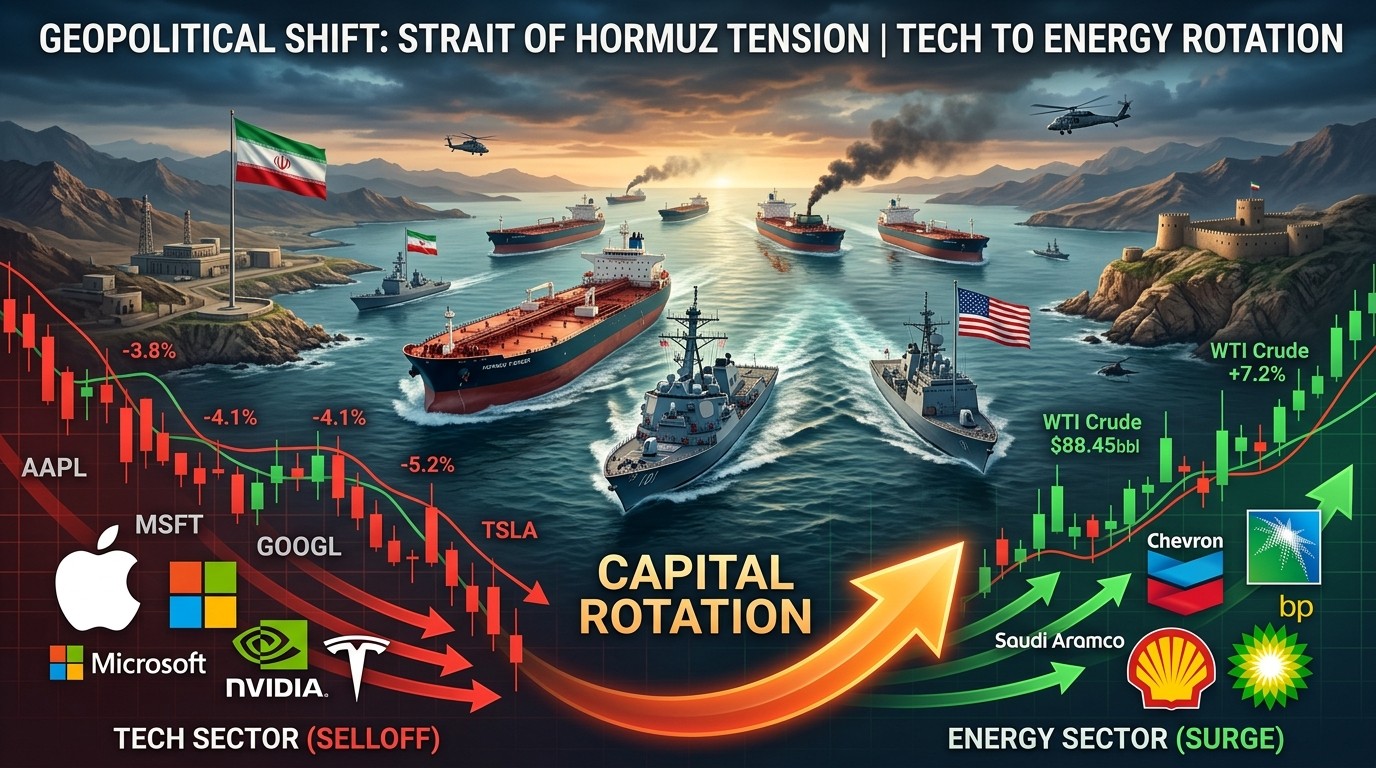

Think about it – the Strait of Hormuz, a critical chokepoint for global energy flows, had seen disruptions. Now, with tankers potentially resuming more regular activity, the supply dynamics are shifting. This temporary waiver isn’t a full resolution, but it certainly eases immediate pressures on importers and could help stabilize costs for everything from gasoline to manufacturing inputs.

Markets move on expectations as much as reality, and right now expectations are tilting toward increased supply.

That sentiment seems to capture the mood. Yet, as with any geopolitical story, the devil lies in the details. Will the 60 days lead to a longer-term framework? Investors are watching closely for signs of sustained progress versus temporary posturing.

Oil Market Implications: Lower Prices Ahead?

Lower oil prices might sound like universally good news for consumers, but the picture is more nuanced for producers and related industries. Energy companies that had benefited from tighter supply could face margin compression if the influx of Iranian oil proves significant. On the flip side, sectors reliant on affordable energy – think transportation, chemicals, and even some consumer goods – stand to gain.

I’ve always found it fascinating how commodity cycles influence so many other areas of the economy. When oil dips, it can act as a tailwind for broader growth by reducing input costs. However, if prices fall too sharply, it might signal weaker demand elsewhere, which carries its own set of risks. In this case, the relief feels more supply-driven than demand-driven, which is generally viewed more positively.

- Potential increase in global oil supply easing tightness in physical markets

- Downward pressure on benchmark crude prices continuing in the short term

- Opportunities for refiners and downstream players to improve margins

- Challenges for upstream producers in higher-cost regions

Beyond the immediate price action, this development could influence investment decisions in the energy patch. Companies with diversified operations or strong balance sheets may weather any volatility better than pure-play explorers. It’s a reminder that in commodities, timing and adaptability often matter more than outright predictions.

Wall Street Rotation: Megacap Tech Takes a Hit

While the oil news provided some positivity on the geopolitical front, domestic markets showed a different story. A noticeable rotation out of megacap technology names weighed on major indices, with the S&P 500 and Nasdaq closing lower. Names that have dominated market gains for years suddenly faced selling pressure amid rising yields and questions around artificial intelligence spending.

Alphabet, Amazon, Meta, and Microsoft each posted declines ranging from a couple of percentage points to more significant drops. Higher bond yields tend to pressure growth-oriented stocks because future earnings are discounted more heavily. Add in some rotation toward sectors that might benefit from lower energy costs or perceived value, and you have the recipe for a session where leadership changed hands.

In my experience covering markets, these rotations are healthy over the long run even if they feel uncomfortable in the moment. They prevent over-concentration and can create buying opportunities for patient investors. Still, watching tens of billions in market value shift in a single day is always a spectacle worth analyzing carefully.

The concentration in a handful of stocks had become extreme; a reset was arguably overdue.

This isn’t to say the tech sector is in trouble fundamentally. Many of these companies boast impressive cash flows and innovation pipelines. But when sentiment shifts, even the strongest names can experience pullbacks. The question now is whether this represents a short-term rotation or the start of something more prolonged.

SpaceX Faces Reality Check After Stellar Debut

One of the most talked-about new public companies recently has been SpaceX, and its post-IPO performance has taken a dramatic turn. After an impressive initial rally, shares have now declined sharply for multiple sessions, including a steep 16% drop that erased substantial market capitalization in one day alone.

The company recently highlighted a robust cash position exceeding $100 billion while also announcing plans for a significant bond offering. Such moves are common as firms look to fund ambitious growth plans, but the timing amid a broader tech selloff has investors scrutinizing the valuation closely. SpaceX’s story remains compelling – reusable rockets, satellite internet, and ambitious exploration goals capture the imagination.

Yet, as with any high-growth name, the market eventually demands proof of execution and sustainable profitability paths. The gravity-defying rally has lost some altitude, to borrow a fitting metaphor. For long-term believers in the space economy, this could present an entry point, but near-term volatility seems likely to persist.

- Review the company’s cash reserves and capital raise plans carefully

- Assess progress on key projects like Starlink expansion

- Consider competitive landscape in both launch services and communications

- Monitor how broader market sentiment toward growth stocks evolves

It’s a classic case of hype meeting operational realities. Space remains an incredibly capital-intensive endeavor, and public markets have a way of reminding everyone that even visionary enterprises face financial gravity.

Remembering Alan Greenspan: A Legacy in Economic Policy

Amid all the current market action, Wall Street took a moment to honor a towering figure in modern economics. Alan Greenspan, who led the Federal Reserve for nearly two decades, passed away at the age of 100. His tenure spanned multiple economic cycles, from the dot-com era to the early 2000s housing boom.

Greenspan was known for his measured approach and memorable phrases, including the famous warning about “irrational exuberance” years before the tech bubble burst. His influence extended far beyond policy decisions – he shaped how generations of investors and policymakers think about risk, inflation, and market psychology.

Today, with excitement around artificial intelligence reaching feverish levels in some corners, echoes of past cycles naturally emerge. Are we seeing similar signs of exuberance? History doesn’t repeat exactly, but it often rhymes. Greenspan’s career reminds us to maintain perspective even during periods of rapid innovation and apparent limitless potential.

Markets and economies move in cycles. Understanding that rhythm remains one of the most valuable skills for any investor.

UK Political Shifts: Another Prime Minister, New Uncertainties

Across the Atlantic, Britain is experiencing yet another change at the top. Keir Starmer’s resignation has paved the way for a potential successor, with Andy Burnham positioned as a frontrunner. This would mark the seventh prime minister in a decade for the UK, highlighting the challenges of stable governance in the post-Brexit era.

Investors are watching for clues on future policy direction, particularly around debt management, growth initiatives, and fiscal responsibility. The pound and government bonds have remained relatively steady so far, but any significant policy shifts could alter that picture quickly. Political continuity, or the lack thereof, matters greatly for long-term investment planning in any country.

It’s striking how leadership changes can become almost routine in certain democracies. While it creates short-term uncertainty, it also offers opportunities for fresh approaches to entrenched problems like sluggish productivity and high public debt. The coming weeks will be telling as nominations and potential contests unfold.

Energy Innovation: Chevron’s Deal with Microsoft Data Centers

On a more constructive corporate note, Chevron announced a long-term agreement to supply natural gas for a massive Microsoft data center project in Texas. The facility, expected to require enormous amounts of power, underscores the growing energy demands of the artificial intelligence boom.

This partnership highlights an important trend: traditional energy companies are increasingly positioning themselves as partners in the tech revolution. Data centers don’t run on hype alone – they need reliable, dispatchable power sources. Natural gas often fills that role effectively, bridging the gap while renewables scale up.

I’ve observed this convergence with interest. The AI surge is reshaping not just software and semiconductors but also the entire energy value chain. Companies that can deliver secure, affordable power at scale stand to benefit significantly. This particular deal spans 20 years, providing visibility that markets tend to reward.

| Sector | Key Driver | Investment Angle |

| Energy | Data center demand | Long-term contracts |

| Technology | Power infrastructure | Reliable supply chains |

| Utilities | Grid modernization | Capacity expansion |

Such collaborations could become more common as computing power requirements skyrocket. For investors, it pays to look beyond headline tech names and consider the picks and shovels providers enabling the infrastructure buildout.

Broader Market Outlook: Balancing Risks and Opportunities

Putting it all together, this moment feels like a classic intersection of geopolitics, sector rotations, and technological disruption. The Iran sanctions waiver provides near-term relief on energy costs but doesn’t eliminate longer-term risks in the region. The tech pullback creates potential value but requires careful stock selection amid evolving AI narratives.

Personal opinion here: diversification has rarely felt more relevant. Concentrated bets on a few megacap names worked brilliantly for years, but cycles eventually turn. Those who spread exposure across energy, industrials, international markets, and quality growth stories may sleep better at night.

Additionally, the Summer Davos gathering in China brings together leaders to discuss innovation at scale, trade shifts, and technology applications. These forums often provide hints about future policy directions and collaboration areas that smart investors track.

- Monitor oil price stabilization levels in coming weeks

- Watch bond yields for continued pressure on growth stocks

- Evaluate individual company fundamentals rather than sector headlines

- Consider geopolitical developments as ongoing rather than resolved

- Stay diversified across asset classes and geographies

One of the most intriguing aspects is how quickly narratives can change. What looked like sustained tightness in oil markets suddenly faces potential oversupply signals. What appeared as unstoppable tech momentum encounters valuation and rotation realities. This fluidity is what makes investing both challenging and rewarding.

Lessons from History and Current Cycles

Alan Greenspan’s passing invites reflection on how policy, psychology, and economics intertwine. His career spanned periods of great innovation and painful corrections. Today’s AI enthusiasm echoes past technological leaps – the internet, personal computers, even railroads in earlier eras. Each brought tremendous progress alongside speculative excesses.

The key, as always, is separating genuine transformative potential from froth. Artificial intelligence undoubtedly holds enormous promise, but implementation, regulation, energy requirements, and monetization timelines will determine winners and losers. Companies that pair technological ambition with sound capital allocation deserve close attention.

Meanwhile, the UK’s political merry-go-round serves as a case study in how governance stability affects economic confidence. Frequent changes can deter long-term investment and complicate policy continuity. Investors in British assets will need to assess any new leadership’s commitment to pragmatic growth strategies.

Expanding on the data center theme, the power demands of modern computing are staggering. A single large facility requiring gigawatts of electricity equates to powering millions of households. This isn’t just an energy story – it’s about infrastructure, permitting, grid resilience, and the entire supporting ecosystem. Natural gas, nuclear restarts, renewables with storage, and efficiency gains will all play roles.

Looking ahead, several factors could influence near-term market direction. Any concrete follow-through on Iran nuclear inspections would be positive for risk assets. Corporate earnings seasons always provide fresh data points, particularly commentary around capital spending plans in tech and energy. Central bank signals on interest rates remain crucial, especially with yields already moving higher.

I’ve found that successful investing often comes down to adaptability and a willingness to challenge prevailing consensus when evidence shifts. The current environment rewards those who can hold multiple scenarios in mind simultaneously: geopolitical progress or setbacks, tech leadership continuation or broadening participation, energy abundance or persistent volatility.

Consider smaller companies that might benefit from rotation. Value-oriented sectors, international equities exposed to global recovery, or firms in the energy transition space could see renewed interest. Of course, thorough due diligence remains essential – not every name benefits equally from macro tailwinds.

Another angle worth exploring is currency implications. A weaker dollar environment, potentially supported by lower oil prices and shifting rate expectations, could benefit emerging markets and commodity producers. The pound’s steadiness amid UK uncertainty suggests markets are withholding judgment pending clearer policy signals.

As we process these developments, maintaining a long-term perspective helps. Short-term noise from sanctions waivers, stock rotations, or political changes can obscure underlying trends like technological advancement and energy system evolution. The companies and economies that adapt best to these forces will likely deliver the strongest results over time.

In wrapping up this analysis, the week’s events underscore the market’s sensitivity to news flow across multiple fronts. From temporary sanction relief potentially flooding oil markets to megacap tech experiencing profit-taking, investors face a complex mosaic. SpaceX’s correction serves as a reminder that even the most hyped stories face scrutiny. Political transitions in the UK add another layer of variables, while landmark figures like Greenspan remind us of the enduring importance of prudent policy.

The Chevron-Microsoft partnership exemplifies how traditional and new economy players are finding common ground in addressing massive infrastructure needs. This cross-sector collaboration could become a template for future deals as AI infrastructure scales globally. For individual investors, the takeaway is clear: stay informed, remain diversified, and focus on quality businesses with durable competitive advantages.

Markets rarely move in straight lines, and the current period is no exception. By understanding the forces at play – geopolitical, sectoral, technological, and political – we position ourselves better to navigate whatever comes next. The coming days and weeks will provide more data points, but the foundational shifts appear underway. Whether you’re an active trader or a long-term holder, these developments merit close attention and thoughtful reflection.

One final thought: in times of rapid change, those who maintain intellectual humility and a learning mindset often fare best. The “Maestro” Greenspan himself evolved his views over decades in response to new realities. Today’s investors would do well to follow that example amid evolving global dynamics.