Have you ever wondered what happens when a major government healthcare program undergoes significant policy shifts? Last year, we saw exactly that play out with Obamacare, officially known as the Affordable Care Act exchanges. Enrollment numbers took a noticeable dive, shedding almost three million participants. This change has sparked intense discussions across the political spectrum about affordability, program integrity, and the future of healthcare access in America.

The numbers are striking. From a peak of over 22 million last year, participation fell to around 19.2 million by early 2026. While some view this as a concerning loss of coverage, others see it as a necessary correction after years of relaxed rules during the pandemic era. As someone who has followed healthcare policy developments for years, I find this situation particularly fascinating because it touches on so many core issues – from family budgets to government oversight.

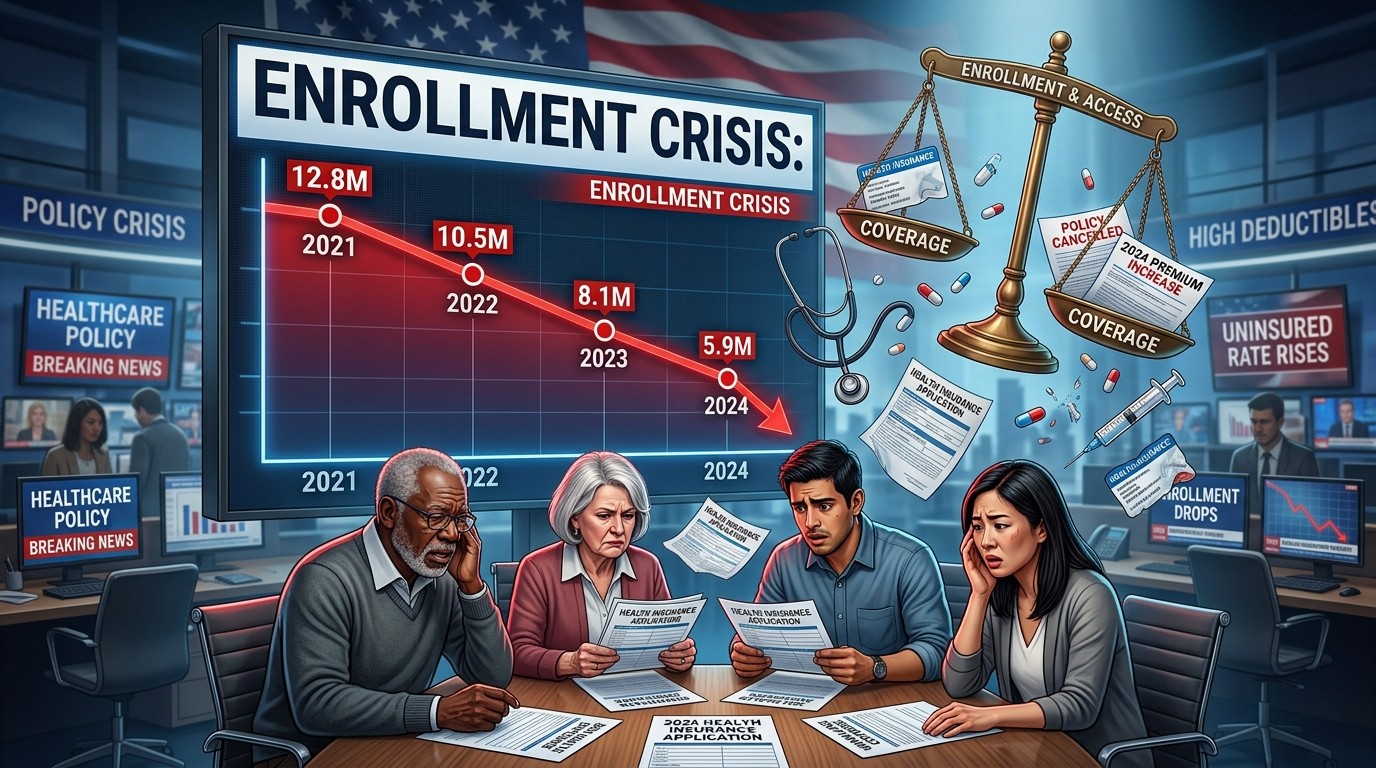

Understanding the Scale of the Enrollment Decline

This wasn’t a small fluctuation. We’re talking about a drop that represents roughly 13-14% of the previous year’s participants. To put that in perspective, it’s like an entire major city’s population suddenly stepping away from their coverage plans. The timing coincides with several important policy adjustments that aimed to restore pre-pandemic verification standards.

During the height of the national health emergency, many requirements were loosened. Automatic reenrollments became the norm, and income checks were less stringent. This led to a surge in participation, but it also opened doors for potential misuse. Now, as those temporary measures have ended, the system is recalibrating.

What the Official Data Shows

Federal figures released in late June painted a clear picture. The program had ballooned during the relaxed eligibility period from 2021 to 2024. But as verification processes tightened, millions of enrollees either chose not to continue or were found ineligible for subsidies. This shift didn’t happen overnight – it was the result of deliberate administrative changes.

Interestingly, even after the decline, enrollment remains higher than in most pre-2025 years. This suggests the core of the program is still serving a substantial population, but the artificial inflation from easier access has been addressed.

The changes mostly reverted to pre-pandemic coverage and policy rules, which had been an incentive for fraud in some cases.

That’s the perspective from analysts who have studied the program’s operations closely. They point to excessive subsidies and minimal verification as creating strong incentives for improper sign-ups.

Rising Premiums and Their Impact

One factor that can’t be ignored is cost. The average monthly premium jumped from $113 in 2025 to $178 this year. For many families already stretched thin, that increase represents a real burden. When your household budget is tight, even an extra $65 a month can force difficult decisions about priorities.

The benchmark silver plan, which determines subsidy levels, saw a roughly 25% increase. This affects how much financial assistance people receive. Some enrollees who previously paid little or nothing suddenly faced higher out-of-pocket costs. It’s easy to see why this might lead certain individuals to drop coverage altogether.

- Monthly premiums increased by over 50% year-over-year for unsubsidized plans in some cases

- Subsidy calculations changed with higher benchmark premiums

- Many families reported reassessing their healthcare spending priorities

I’ve spoken with people in this situation, and the stories are consistent. One middle-class family in the Midwest told me they had to choose between maintaining their plan and covering other essential expenses like groceries and utilities. These are the real human impacts behind the statistics.

The Fraud and Integrity Question

On the other side of the debate, administration officials emphasize program integrity. They claim to have prevented nearly three million ineligible people from receiving subsidies. Estimates suggest fraudulent or improper enrollments dropped significantly from previous highs. This includes cases where individuals didn’t qualify based on income or other criteria.

One striking statistic shared by officials is that around 40% of some enrollees never actually used their benefits. This raises legitimate questions about whether those policies were genuinely needed or if they represented waste in the system. When people sign up but never visit a doctor or fill a prescription, it suggests something isn’t working as intended.

We have a lot of fake people on the policies. The reality is we need to ensure resources go to those who truly need them.

Comments like this from program administrators highlight the tension between expanding access and maintaining fiscal responsibility. It’s a delicate balance that policymakers have struggled with for years.

Political Reactions and Interpretations

As expected, reactions fell largely along party lines. Critics argued the changes disproportionately hurt vulnerable populations and pointed to premium increases as the main culprit. They framed the enrollment drop as evidence of failed policies that made healthcare less accessible.

Supporters, meanwhile, celebrated what they saw as successful efforts to root out waste and ensure taxpayer dollars served legitimate needs. They argued that previous relaxed standards had created opportunities for exploitation that needed correction.

This divide isn’t new in American healthcare debates. What makes this moment different is the concrete data showing a significant shift after specific policy changes. It provides real-world evidence for both sides to analyze.

Historical Context and Pre-Pandemic Trends

It’s worth noting that before the enhanced subsidies and relaxed rules of 2021, Obamacare enrollment had actually been declining for several consecutive years. This suggests underlying challenges with the program’s structure that extend beyond recent events. Affordability has long been a concern for many middle-income families who don’t qualify for substantial assistance.

The pandemic period created an unusual spike through both policy changes and increased health awareness. Now we’re seeing a return toward earlier patterns, though not completely. The system appears to be finding a new equilibrium.

Economic Factors at Play

Broader economic conditions influence these decisions too. With inflation affecting everything from food to housing, healthcare costs compete for limited household resources. Employment trends, wage growth, and overall financial confidence all factor into whether families maintain insurance coverage.

Some analysts suggest that improving job markets in certain sectors provided alternative coverage options through employers. Others point to people simply choosing to go without rather than pay higher premiums. The truth likely involves a combination of these elements.

| Year | Enrollment (millions) | Avg Monthly Premium |

| 2021 | ~15 | Higher (inflation adjusted) |

| 2025 | 22.1 | $113 |

| 2026 | 19.2 | $178 |

This simplified view shows how dramatically things changed during the special period and the subsequent adjustment. Understanding these numbers requires looking beyond headlines to the underlying dynamics.

Impacts on Different Demographics

Not all groups were affected equally. Lower-income families with strong subsidies might have been less impacted, while those just above subsidy thresholds felt the premium increases more acutely. Rural versus urban differences also play a role, as healthcare options and costs vary significantly by location.

Younger, healthier individuals have historically been harder to attract to these plans. If the enrollment drop included many in this category, it could affect the risk pool and future premium stability. This remains one of the ongoing challenges for the exchanges.

What Experts Are Saying

Health policy researchers offer nuanced takes. Some highlight survey data showing about 9% of previous enrollees became uninsured. They worry about potential gaps in care and delayed treatments. Others focus on the reduction in improper payments, arguing that cleaning up the rolls ultimately strengthens the program long-term.

In my view, both perspectives contain important truths. Protecting program integrity matters for sustainability, but we must also consider the human cost when people lose coverage. Finding the right balance is incredibly difficult.

Looking Ahead: Future Implications

This enrollment shift raises important questions for the coming years. Will premiums continue rising, or will market adjustments stabilize costs? How will states respond with their own initiatives? The debate over healthcare reform isn’t going away anytime soon.

One positive note is that despite the drop, millions still benefit from the marketplaces. The core framework continues providing options for those without employer-sponsored insurance. Refining rather than abandoning the system seems to be the current path.

Personal Stories Behind the Numbers

Beyond statistics, real families are navigating these changes. Some successfully found alternative coverage or adjusted budgets to stay enrolled. Others made the tough choice to forgo insurance, hoping they wouldn’t face major medical issues. These decisions carry real risks and reflect the complexity of American healthcare.

I’ve heard from small business owners who saw their premiums spike and had to rethink their benefits packages. Parents of children with special needs expressed anxiety about maintaining consistent coverage. These aren’t abstract policy debates – they affect daily lives across the country.

The Role of Technology and Administration

Improved verification systems likely played a key role in the enrollment changes. Better data matching with tax records and other government databases helped identify ineligible applicants. While this creates friction for some legitimate users, it aims to ensure fairness and proper use of public funds.

Streamlined processes could also help genuine applicants navigate the system more easily. The goal should be striking the right balance between accessibility and accountability. Technology offers tools to achieve this, but implementation matters tremendously.

Broader Context of Healthcare Costs

This situation doesn’t exist in isolation. Overall medical costs continue pressuring the entire system. Prescription drugs, hospital stays, and specialist care all factor into why insurance premiums behave as they do. Addressing root causes of healthcare inflation remains essential for long-term solutions.

Comparative analysis with other countries shows different approaches to balancing access and cost control. While the U.S. system emphasizes choice and innovation, it also results in higher prices in many areas. Understanding these trade-offs helps contextualize the Obamacare experience.

Potential Policy Adjustments

Moving forward, several options exist. Enhancing competition among insurers, promoting price transparency, and encouraging preventive care could help moderate costs. Targeted subsidies for specific vulnerable groups might address equity concerns without broad inefficiencies.

Whatever path policymakers choose, careful analysis of data like this year’s enrollment figures will be crucial. Evidence-based decisions offer the best hope for improving outcomes for American families.

What Individuals Can Do

For those navigating the current landscape, exploring all available options makes sense. Comparing plans during open enrollment, understanding subsidy eligibility, and considering health savings accounts are practical steps. Staying informed about policy changes helps families make better decisions.

- Review your current coverage and costs carefully

- Explore employer options if available

- Check eligibility for any assistance programs

- Consider lifestyle factors that might affect premiums

- Plan for potential healthcare needs proactively

These aren’t foolproof solutions, but they empower individuals facing uncertainty. Healthcare decisions require personal assessment of risks and priorities.

Final Thoughts on This Turning Point

The drop in Obamacare enrollment represents more than just numbers on a spreadsheet. It reflects the complex interplay of policy, economics, personal choices, and administrative realities. While experts disagree on causes and implications, one thing is clear: the American healthcare system continues evolving.

Perhaps the most important lesson is the need for ongoing evaluation and adjustment. No program is perfect, and circumstances change. By examining what worked and what didn’t during this period, we can work toward more sustainable approaches that balance access, quality, and affordability.

In my experience following these issues, meaningful progress comes from acknowledging trade-offs rather than seeking simple answers. The coming years will show how effectively we’ve learned from recent experiences. For now, millions of Americans are adjusting to this new reality, making choices that affect their health and financial security.

The debate will undoubtedly continue, with new data and developments shaping the conversation. What matters most is keeping focus on practical outcomes for real people rather than partisan talking points. Healthcare touches everyone eventually, making these discussions relevant to all of us.

As we move through 2026 and beyond, watching how enrollment trends develop will provide valuable insights. Whether the numbers stabilize, rebound, or decline further depends on many factors – policy decisions, economic conditions, and individual circumstances. One thing remains certain: the search for better healthcare solutions continues.