Have you ever watched an economy send mixed signals and wondered what it really means for the bigger picture? That’s exactly what’s happening in China right now after the latest inflation figures dropped. Consumer prices grew more slowly than many expected, while costs at the factory gate picked up speed. It’s a classic tale of two different parts of the same economy pulling in slightly different directions.

This isn’t just dry numbers on a spreadsheet. These trends touch everything from everyday household budgets to massive international trade flows. As someone who follows these developments closely, I’ve noticed how these shifts often reveal deeper stories about demand, supply chains, and policy choices. Let’s dive into what June’s data actually shows and why it matters.

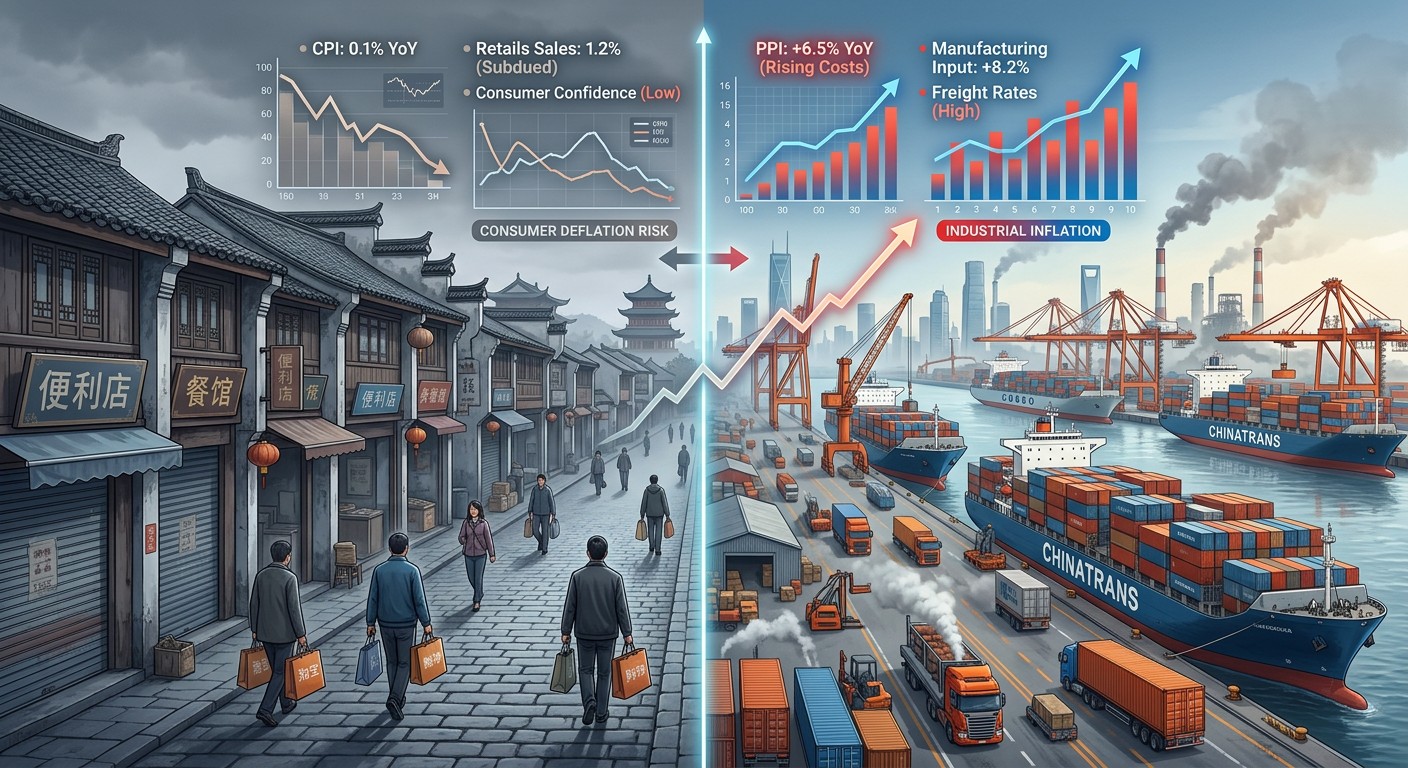

Understanding the Latest Inflation Snapshot

Consumer prices in China rose by just 1% in June compared to the same month a year earlier. That came in below what economists had predicted and marked a slowdown from May’s 1.2% reading. On the surface, it might not sound dramatic, but in the context of recent years, it highlights some ongoing softness in how people are spending.

Meanwhile, the producer price index jumped to 4.1% year-on-year growth. That’s faster than the previous month and right around what analysts expected. Factory-gate prices have been climbing since earlier in the year, driven by higher input costs and strong performance in certain sectors. This contrast between consumer and producer trends creates an interesting dynamic worth exploring in more detail.

Why Consumer Price Growth Slowed

When consumer prices don’t accelerate as hoped, it often points to weaker demand at the household level. People are still feeling the effects of a long housing market adjustment, which has weighed on confidence and spending power. It’s like the classic case where one part of the economy is treading water while another powers forward.

Energy costs remain a factor too. Higher prices for fuel and related items have made daily life more expensive in some ways, yet overall demand hasn’t kept pace. Families are being careful with their money, prioritizing essentials over discretionary purchases. In my view, this cautious approach makes complete sense given the uncertainties many households face.

The gap between robust industrial activity and softer consumption has become a defining feature that policymakers must navigate carefully.

This slowdown in consumer inflation isn’t necessarily all bad news. It can give central authorities more room to support growth without immediately worrying about overheating. But it also underscores the challenge of getting ordinary citizens to spend more freely again.

Producer Prices Gain Momentum

On the producer side, the 4.1% increase tells a story of rising costs being passed along the chain. Commodity prices, influenced by global events, have played a big role here. Factories are dealing with more expensive inputs, yet they’re also seeing solid demand in key areas like technology and equipment.

One bright spot has been the surge in needs related to artificial intelligence and computing power. This has helped lift prices for semiconductors and related tech gear. It’s fascinating how innovation in one field can ripple through traditional manufacturing statistics. Perhaps the most interesting aspect is how quickly these shifts can happen in today’s interconnected world.

- Higher energy and raw material costs from global supply pressures

- Strong export performance supporting factory output

- Increased demand for high-tech components and machinery

- Partial recovery from earlier deflationary periods

These factors combined to push producer prices higher. Yet even here, there are nuances. Recent surveys of purchasing managers showed some easing in input cost pressures compared to the prior month, suggesting the pace might not stay this hot forever.

The Two-Speed Economy Challenge

China’s economy often feels like it’s operating on two tracks. Exports and high-tech manufacturing are showing real strength, while domestic consumption and the property sector lag behind. This imbalance isn’t new, but recent data brings it into sharper focus.

Strong overseas demand has helped keep factories busy. At the same time, many families are still recovering from the wealth effects of a softer housing market. When people feel less wealthy on paper, they tend to hold back on big purchases and even everyday spending. It’s a perfectly human response, yet it creates headaches for those trying to balance overall growth.

I’ve found that these divides can persist longer than many observers expect. The question then becomes how authorities respond. Do they focus stimulus on consumption, or continue leaning on the export and investment engines that have delivered results?

Global Context and Commodity Influences

No economy exists in isolation, and China’s inflation picture reflects worldwide developments. Conflicts in key regions have disrupted energy and commodity supplies, feeding through to higher producer costs. These external shocks often hit manufacturing first before working their way toward consumers.

Semiconductor and tech equipment prices have also benefited from the global push toward advanced computing. Companies worldwide are investing heavily in AI capabilities, and China plays a major role in producing the hardware that makes it possible. This creates a supportive tailwind for certain industrial segments even as broader consumption remains restrained.

What the Numbers Mean for Everyday Life

For the average person in China, slower consumer price growth might mean a bit of relief at the grocery store or when filling up the car. Yet if wages aren’t rising quickly and job security feels uncertain, that relief can be overshadowed by caution. People naturally prioritize saving during uncertain times.

Business owners face a different set of realities. Those in export-oriented industries might be celebrating stronger order books, while retailers dealing with domestic customers could be working harder to attract foot traffic. This divergence affects hiring plans, investment decisions, and even how companies think about pricing strategies.

Policy Outlook and Potential Responses

With growth targets set at a modest but achievable level, authorities have some flexibility. Recent international forecasts have actually become slightly more optimistic about China’s performance this year, citing strong high-tech sectors and infrastructure efforts. Still, getting consumption back on track remains a key priority for many analysts.

A major policy meeting later in July could provide clues about the next steps. Will there be more targeted support for households? Or will the focus stay on reinforcing areas where momentum already exists? In my experience following these developments, patience often proves wise. Big stimulus packages tend to come only when weakness becomes more pronounced and persistent.

The export and manufacturing resilience may reduce the urgency for broad consumer stimulus in the near term.

That doesn’t mean nothing will happen. Smaller, targeted measures could still emerge to support specific vulnerable areas. The art lies in providing enough support without creating new imbalances elsewhere.

Implications for Global Investors and Markets

For those watching from outside China, these inflation figures matter a great deal. Commodity exporters worldwide feel the effects of Chinese demand. Technology companies track factory activity as a signal for component orders. Even currency traders keep a close eye on how these trends might influence monetary policy decisions.

The mixed signals can create volatility in global markets. When producer prices rise faster, it sometimes feeds expectations of stronger growth ahead. Yet softer consumer data raises questions about sustainability. Navigating this requires looking beyond headline numbers to the underlying drivers.

- Track commodity price movements for early warning signs

- Monitor export data for confirmation of manufacturing strength

- Watch consumer confidence surveys for spending clues

- Follow policy announcements closely for stimulus hints

- Consider currency impacts on international competitiveness

Each of these pieces adds to the overall puzzle. Smart observers piece them together rather than reacting to any single release in isolation.

Longer-Term Structural Shifts

Beyond the monthly ups and downs, China continues its transition toward a more high-tech, innovation-driven economy. Success in areas like electric vehicles, renewable energy, and advanced manufacturing provides a buffer against traditional cyclical weaknesses. This evolution takes time but appears to be gaining traction.

Housing will likely remain a focus for years to come. Finding the right balance between stabilizing the sector and preventing excessive speculation is no easy task. How this plays out will influence consumer confidence for the foreseeable future.

Demographic changes also shape the picture. An aging population and evolving workforce dynamics affect both consumption patterns and productivity growth. These are slow-moving forces, but their influence compounds over time.

Comparing With Previous Periods

It’s helpful to remember that China faced deflationary pressures not long ago. The return to positive producer price growth marks an important shift. Yet the consumer side has yet to show the same vigor. This asymmetry is what makes the current situation particularly noteworthy.

| Period | Consumer Prices | Producer Prices | Key Driver |

| May | 1.2% | 3.9% | Moderate demand |

| June | 1.0% | 4.1% | Export strength |

| Earlier Year | Lower | Negative | Deflation concerns |

While the table simplifies complex realities, it highlights how the relationship between these two measures has evolved. Understanding the context prevents overreacting to any single month’s data.

What Could Change the Trajectory?

Several factors might alter the current path. A resolution or easing of global supply disruptions could moderate producer price increases. On the consumer side, successful policy measures to boost confidence and incomes could lift spending. External demand remains crucial but can shift with trading partners’ economic health.

Technological breakthroughs and their adoption rates will also play a role. The faster AI and related technologies integrate into both manufacturing and services, the more opportunities emerge for productivity gains and new revenue streams.

Of course, unexpected events always lurk. Weather patterns affecting agriculture, geopolitical developments, or sudden changes in investor sentiment can move markets quickly. Staying adaptable is key in this environment.

Practical Takeaways for Businesses and Individuals

For companies operating in or with China, diversifying across both export and domestic segments makes sense. Those heavily exposed to consumer markets might look for ways to innovate and offer better value. Manufacturers benefiting from current trends should prepare for potential normalization of input costs.

Individuals might consider how these macroeconomic trends affect personal finances. Saving a bit more during uncertain periods is rarely a bad idea, while keeping an eye on opportunities in growing sectors could pay off over time. Balance remains important.

From my perspective, the most prudent approach involves staying informed without getting overwhelmed by short-term noise. The Chinese economy has demonstrated remarkable resilience through various challenges before, and this period is no different.

As we move through the rest of the year, these inflation dynamics will continue shaping discussions among economists, policymakers, and market participants. The interplay between consumer caution and industrial strength creates both risks and opportunities. Understanding the nuances helps separate signal from noise in what can sometimes feel like a confusing economic landscape.

The coming months will reveal whether consumer prices find renewed momentum or if producer trends dominate the narrative. Either way, adaptability and careful analysis will serve observers well. China’s economic story remains one of the most important in the global arena, full of complexity yet rich with potential insights for those willing to look closer.

What stands out most is how interconnected everything has become. A shift in factory costs in one region affects prices and decisions thousands of miles away. Consumer sentiment in major cities influences supply chains spanning continents. In that sense, these latest figures aren’t just China’s story, they’re part of our shared global economic reality.

I’ll be watching closely for the next set of data and policy signals. In the meantime, keeping perspective on both the challenges and the strengths seems like the most reasonable path forward. The economy rarely moves in straight lines, and this latest chapter reminds us of that truth once again.