Have you ever wondered how a single missed deadline could quietly unravel months of careful financial planning? For millions of Americans juggling student debt, the introduction of the new Repayment Assistance Plan, or RAP, brings both hope and a serious warning. This income-driven option promises real relief, but only if you stay on top of every payment.

I remember chatting with a friend last year who thought he had his loans under control. One overlooked email, a busy week at work, and suddenly his balance wasn’t shrinking the way he expected. Stories like his are becoming more common as borrowers transition to newer plans. With RAP now available, understanding the fine print isn’t just smart—it’s essential.

Understanding the New Repayment Assistance Plan

The RAP program represents a fresh approach from the Department of Education to make student loan repayment more manageable for everyday borrowers. Unlike traditional fixed-payment setups, this plan ties your monthly obligation to a percentage of your income, typically ranging somewhere between one and ten percent. The goal? Prevent balances from ballooning out of control while offering a path toward eventual forgiveness after thirty years.

What makes RAP stand out is its built-in protections designed specifically to fight back against growing interest. But these protections come with strings attached—strings that tighten dramatically if you’re even one day late. In my view, this creates a high-stakes environment where discipline matters more than ever before.

The Valuable Benefits Tied to On-Time Payments

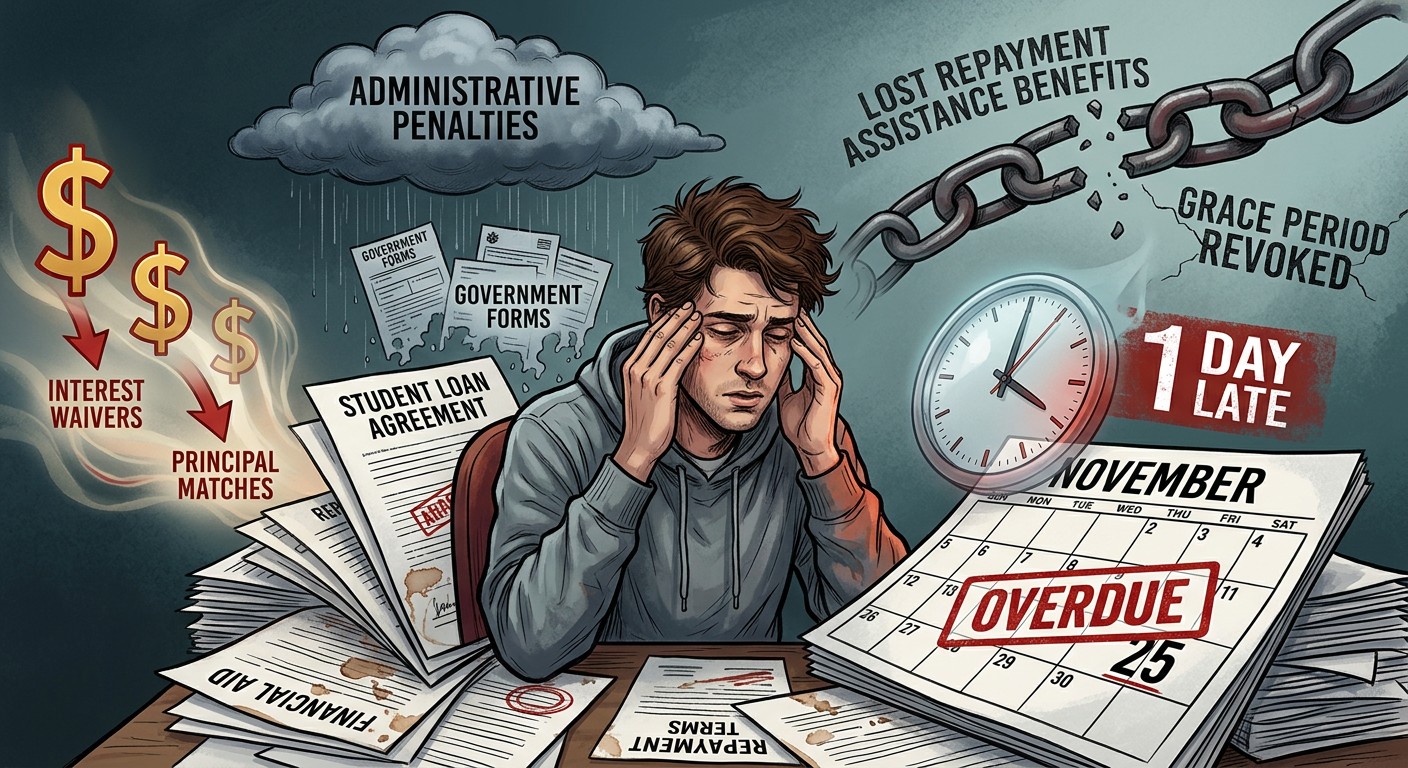

At its core, RAP aims to shield borrowers from the dreaded cycle where interest causes your total debt to exceed what you originally borrowed. Two main mechanisms drive this protection, and both depend entirely on making your payment by the due date.

First comes the interest waiver. Any unpaid interest that accrues during the month gets erased by the government as long as you’ve paid on time. This alone can save hundreds over the life of the loan, especially for those with larger balances or lower monthly payments.

Second is the principal match feature. If your required payment doesn’t reduce the principal by at least fifty dollars in a given month, the department can contribute up to that amount to ensure your balance actually decreases. It’s like having a financial teammate pushing your progress forward each month.

Being late with a payment, by even just one day under the RAP repayment plan, will cost you. You will lose valuable benefits that save you money.

– Higher education expert

These perks aren’t small print bonuses. They form the foundation of why many borrowers are excited about switching to RAP. Yet the plan’s strict enforcement means that missing the deadline resets your advantages for that billing cycle entirely.

What Happens When You Pay Late

Picture this: You’ve had a tough month. Bills piled up, your car needed repairs, or maybe you simply forgot to check the due date. Under RAP, that single slip-up doesn’t just add a late fee—though those might apply too. It strips away the interest waiver and any potential principal match for the month.

Your payment still counts toward progress in a basic sense, but you lose the extra help that makes the plan truly effective. Over time, these missed opportunities compound, leaving borrowers in a tougher spot than if they’d never enrolled at all. Recent discussions among financial advisors highlight how quickly this can erode confidence in repayment programs.

- Full interest waiver forfeited for the month

- Principal matching contribution lost

- No credit toward forgiveness for that payment in some contexts

- Potential impact on overall loan trajectory

Interestingly, one smaller benefit does survive—a per-dependent discount that reduces your bill based on family members listed on your taxes. This might cover children, aging parents, or other qualifying dependents, offering a bit of cushion even during a late month.

Why RAP Handles Late Payments Differently

Many existing income-driven repayment options include some grace period before a payment is officially marked late. RAP takes a firmer stance. The consequences kick in immediately after the due date passes. This uniqueness stems from the program’s design to reward consistent behavior while maintaining strict accountability.

Experts point out that this approach encourages borrowers to treat their student loan obligations with the same seriousness as a mortgage or car payment. In practice, it separates those who succeed from those who struggle with the plan’s long-term potential.

I’ve seen how small habits build big results in personal finance. Setting up systems early prevents the panic that comes from last-minute scrambles. With RAP, that philosophy becomes even more critical.

Real-World Impact on Borrowers

Consider Sarah, a teacher in her late twenties with moderate debt from her master’s program. Under RAP, her payments feel affordable thanks to the income-based calculation. But when she missed a due date while dealing with a family emergency, she watched her interest waiver disappear. That month, instead of seeing progress, her balance barely budged.

Stories like Sarah’s aren’t rare. Nearly fifty thousand borrowers have already applied for RAP since its launch. Many are drawn by the promise of manageable payments and forgiveness after thirty years, but the strict timing rules catch some off guard.

For public servants pursuing Public Service Loan Forgiveness, the stakes rise higher. Late payments under RAP won’t count toward the required 120 qualifying payments, potentially delaying forgiveness by months or years.

Smart Strategies to Stay On Time

The simplest and most effective solution? Automatic payments. Not only does this remove the risk of forgetting, but the Department of Education sweetens the deal with a temporary interest rate reduction for those who enroll by the end of September. This discount lasts through June 2028—a meaningful saving if you qualify.

That said, autopay isn’t foolproof. Some borrowers report occasional glitches where the wrong amount gets withdrawn. Staying vigilant means reviewing your statements each month and keeping your contact information current with your servicer.

- Enroll in autopay with your loan servicer as soon as possible

- Set calendar reminders even with automatic deductions

- Monitor your account for accurate withdrawals

- Update income information promptly when it changes

- Avoid overpaying in ways that trigger “pay ahead” status

Income fluctuations represent another key area. If your earnings drop, contacting your servicer right away allows for an adjusted payment that you can actually afford. Proactive communication prevents missed payments and keeps those valuable benefits intact.

The Psychology Behind Payment Discipline

There’s more to this than numbers on a spreadsheet. Student debt carries emotional weight—stress, anxiety, and sometimes a sense of being trapped. The RAP plan’s structure acknowledges this reality by offering relief, but it also demands responsibility in return.

In my experience following personal finance trends, borrowers who treat their repayment like a non-negotiable priority tend to see better outcomes. They build habits that extend beyond loans into other areas of money management. Perhaps the most interesting aspect is how a seemingly small rule about due dates reveals larger truths about financial resilience.

That protection comes from two benefits, both tied to paying on time.

Building this discipline doesn’t require perfection. It requires systems. Whether through apps that send alerts, dedicated bank accounts for loan payments, or partnering with a trusted family member for accountability, finding what works for your lifestyle makes all the difference.

Comparing RAP to Other Repayment Options

While RAP offers innovative features, it’s not the only game in town. Traditional plans, older income-driven repayment programs, and refinancing with private lenders each come with their own pros and cons. What sets RAP apart is the speed with which benefits evaporate after a late payment.

| Plan Feature | RAP | Other IDR Plans |

| Payment Calculation | 1-10% of income | Varies widely |

| Interest Waiver | On-time only | Often more forgiving |

| Principal Match | Up to $50 | Generally none |

| Late Payment Impact | Immediate loss | Grace periods common |

This comparison helps illustrate why borrowers need to fully understand their chosen path. RAP rewards punctuality generously but penalizes inconsistency sharply. For some, this structure motivates better habits. For others, it might create unnecessary pressure.

Long-Term Forgiveness and Planning Ahead

After thirty years of qualifying payments, RAP offers forgiveness on any remaining balance. That’s a powerful endpoint for those carrying debt from expensive degrees or multiple degrees. However, reaching that milestone requires consistent on-time performance across three decades.

Planning involves more than just making payments. It means periodically reviewing your overall financial picture—budgeting, emergency funds, career growth, and even side income opportunities. Those who succeed often integrate their student loan strategy into a broader wealth-building approach.

Think about it. What if your income rises significantly in the coming years? Your RAP payment will increase accordingly, but so might your ability to pay extra when it makes sense. Balancing the benefits of the plan with opportunities to accelerate payoff requires thoughtful consideration.

Common Pitfalls to Avoid

- Assuming all income-driven plans work the same way

- Setting up autopay and then ignoring account activity

- Paying more than required without understanding “pay ahead” rules

- Delaying income recertification when circumstances change

- Forgetting that dependents can affect your monthly bill

Avoiding these traps starts with education. Take time to read the documentation from your servicer. Ask questions. Join reputable online communities where borrowers share real experiences—though always verify advice with official sources.

Building a Sustainable Repayment Mindset

Student loans often feel like a burden that never ends. Shifting your perspective can help. View RAP not just as a repayment vehicle but as a tool for financial freedom. Each on-time payment preserves benefits and moves you closer to that thirty-year finish line.

I’ve always believed that financial success stems from consistent small actions rather than occasional heroic efforts. Paying your student loan on time every month exemplifies this principle perfectly. It builds credit, reduces stress, and creates momentum that spills into other life areas.

Consider tracking your progress visually. Some borrowers use spreadsheets showing balance over time, projected forgiveness dates, and cumulative savings from waivers and matches. Seeing the numbers improve month after month provides powerful motivation during challenging periods.

What to Do If You Miss a Payment

Even with the best intentions, life happens. If you realize you’ve missed the due date, act quickly. Contact your loan servicer immediately to understand the specific impact on your account. In some cases, they may offer options to get back on track.

While you can’t recover the lost benefits for that month, you can prevent further damage. Recommit to automatic payments. Adjust your budget if necessary. And remember that one setback doesn’t define your entire repayment journey.

Many borrowers who experience a late payment use it as a learning experience. They implement stronger safeguards and emerge more knowledgeable about their loans than before.

The Broader Context of Student Debt in America

Student loan balances have reached staggering levels nationwide. For many graduates, debt influences major life decisions—from buying homes to starting families. Programs like RAP attempt to address these realities by making repayment more humane while still expecting accountability.

Whether you’re newly graduated or have been paying for years, staying informed about policy changes remains crucial. Rules evolve. Benefits appear and sometimes disappear. Your best defense is knowledge combined with consistent action.

In closing, the new Repayment Assistance Plan offers genuine hope for millions struggling with student debt. Its benefits around interest and principal can transform the borrowing experience. But those advantages demand punctuality. By prioritizing timely payments—ideally through automation while staying attentive—you position yourself to reap the full rewards this program offers.

Take a moment today to check your due dates, review your servicer portal, and consider setting up those automatic payments if you haven’t already. Your future self will thank you when your balance steadily decreases and those forgiveness years get closer. Managing student loans successfully isn’t about being perfect. It’s about being prepared and persistent.

The journey might feel long, but with the right approach, it’s entirely manageable. Here’s to making informed choices that support your financial well-being for years to come.