Have you ever wondered how a single signature on a form could unravel someone’s career? It’s a question I’ve been mulling over lately, especially with recent whispers of financial misconduct shaking up the highest levels of government and finance. The stakes are high—think trillions of dollars in debt and the power to steer the economy. What’s unfolding isn’t just about paperwork gone wrong; it’s a glimpse into how power, money, and influence collide.

The Hidden Power of Mortgage Fraud Allegations

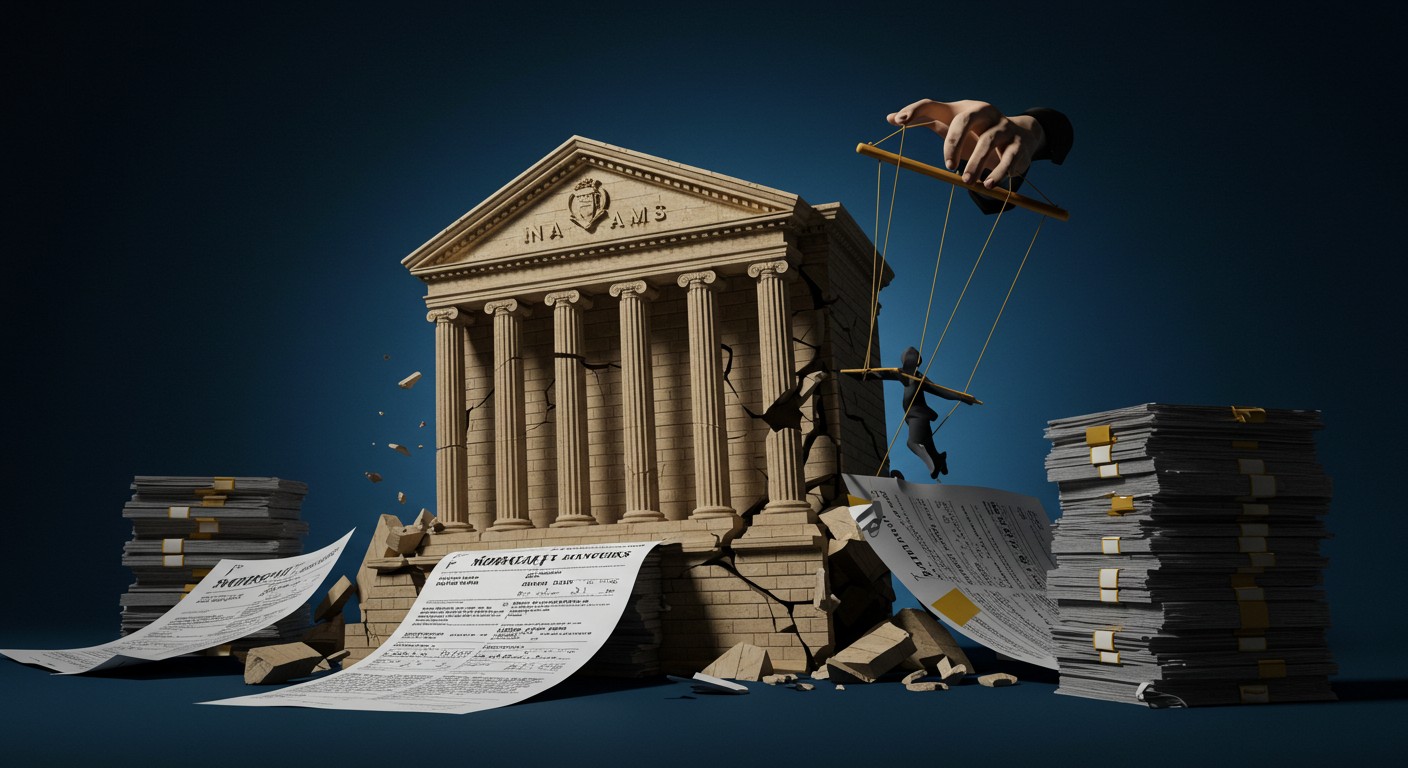

The world of finance is no stranger to scandal, but when allegations of mortgage fraud start targeting key players in the Federal Reserve and political sphere, it’s hard not to sit up and take notice. These aren’t just clerical errors; they’re accusations that could shift the balance of economic control. Let’s dive into what’s happening and why it matters to anyone with a stake in the financial system—which, let’s be honest, is pretty much all of us.

A Scandal That Hits Close to Home

Picture this: you’re filling out a mortgage application, and you check a box claiming a property as your primary residence. Seems harmless, right? It could mean a better interest rate or tax break. But what if you did it for two properties, just weeks apart? That’s the kind of accusation now aimed at a high-ranking Fed official. The claim is that they misrepresented their home status to snag better loan terms—a move that’s not just unethical but potentially illegal.

Misrepresenting your primary residence on a loan application isn’t just a white lie; it’s a calculated risk that can lead to serious legal consequences.

– Financial ethics expert

This isn’t about someone forgetting to dot an “i.” It’s about bank fraud, a charge that carries the weight of federal investigations and public scrutiny. The official in question, a key player in setting interest rates, now faces calls to step down. And the timing? It couldn’t be more suspicious, aligning with a broader push to reshape the Federal Reserve’s leadership.

Why the Federal Reserve Is in the Crosshairs

The Federal Reserve is the backbone of America’s economy, controlling the levers of monetary policy. With the government drowning in over $1.2 trillion in annual debt service costs, there’s intense pressure to lower interest rates. Lower rates mean cheaper borrowing, which could ease the burden of that massive debt. But here’s the catch: not everyone at the Fed is on board with slashing rates, and that’s where the drama begins.

I’ve always found it fascinating how politics and finance intertwine. Recent moves suggest a deliberate effort to stack the Fed with voices that align with a specific agenda—namely, cutting rates to manage runaway debt. When a Fed governor unexpectedly resigned recently, it raised eyebrows. Then, almost like clockwork, another official was hit with these fraud allegations. Coincidence? Perhaps, but I’m not so sure.

The Political Angle: Settling Scores

It’s not just Fed officials in the spotlight. Prominent politicians are also facing similar accusations. One high-profile figure, known for pursuing legal action against others for financial missteps, now stands accused of the same. They allegedly claimed multiple properties as their primary residence and fudged details on loan applications to secure better terms. The irony is thicker than a bank vault door.

No one is above the law, especially when the evidence is a paper trail you can’t erase.

– Legal analyst

These allegations aren’t just about personal gain; they’re a political weapon. The administration seems to be leveraging these claims to clear out opposition and install allies in key positions. It’s a high-stakes game of chess, with the economy as the board. And when you consider the accusations against another politician—a senator no less—for similar tricks, it’s clear this is about more than just one person’s misstep.

What’s at Stake for the Economy?

Let’s break it down. If the administration succeeds in reshaping the Fed, we could see aggressive rate cuts. Sounds great for borrowers, but there’s a flip side. Lower rates often mean printing more money, which can fuel inflation. And with inflation already a concern for many households, this could hit hard.

- Higher inflation: More money in circulation could drive up prices for everything from groceries to gas.

- Weakened dollar: A push for a weaker currency, as some appointees have suggested, could erode purchasing power.

- Market volatility: Uncertainty about Fed leadership could spook investors, leading to choppy markets.

I can’t help but wonder if we’re on the brink of a financial storm. The government’s debt is a ticking time bomb, and lowering rates might just be kicking the can down the road. But for savvy investors, there’s a silver lining—opportunities to protect and even grow wealth in turbulent times.

Protecting Your Wealth in a Shaky System

So, what can you do when the financial system feels like it’s built on quicksand? In my experience, leaning into real assets is a solid move. These are things you can touch—think gold, real estate, or commodities—that tend to hold value when inflation spikes.

| Asset Type | Inflation Protection | Risk Level |

| Gold | High | Low-Medium |

| Real Estate | Medium-High | Medium |

| Commodities | Medium | Medium-High |

Investing in these assets isn’t just about playing defense; it’s about positioning yourself to thrive. For instance, real estate often appreciates during inflationary periods, especially if you lock in fixed-rate financing before rates climb. Gold, on the other hand, is a classic hedge that’s been around for centuries—hardly a new trick, but it works.

The Bigger Picture: Trust in Institutions

Beyond the financial fallout, there’s a deeper issue at play: trust. When Fed officials and politicians get tangled in financial scandals, it erodes confidence in the system. If the people setting interest rates or passing laws can’t follow the rules, why should we trust their decisions?

Trust is the currency of governance. Once it’s gone, it’s hard to earn back.

– Economic commentator

It’s a sobering thought. The average person is held to a higher standard on their mortgage application than some of these officials seem to be. And yet, the consequences of their actions ripple out, affecting markets, savings, and the cost of living. It makes you question whether the system is rigged—or just deeply flawed.

What’s Next for the Fed and Beyond?

The road ahead is murky. If these allegations lead to more resignations, the administration could gain a stranglehold on the Fed, pushing through policies that prioritize short-term relief over long-term stability. But at what cost? Inflation could spiral, and the dollar could take a hit, leaving everyday folks to bear the brunt.

- Monitor Fed appointments: Keep an eye on who’s filling these vacant seats and their stance on rates.

- Prepare for inflation: Diversify into assets that hold up when prices rise.

- Stay informed: Scandals like these often signal bigger shifts—don’t get caught off guard.

I’ll admit, it’s a lot to take in. The interplay of politics, finance, and personal ambition is like a soap opera with real-world consequences. But by understanding what’s happening, you can make smarter choices with your money and stay ahead of the curve.

In the end, these mortgage fraud allegations are more than just gossip—they’re a window into how power is wielded in the financial world. Whether it’s a calculated move to control the Fed or a genuine push for accountability, the fallout will shape the economy for years to come. So, what’s your next step? Maybe it’s time to take a hard look at your investments and ask: am I ready for what’s coming?