Have you ever looked at your grocery bill and wondered how it’s possible that prices keep climbing, yet we’re told inflation is under control? It’s frustrating, isn’t it? Lately, there’s been a lot of back-and-forth among policymakers about whether we’ve really beaten rising costs, but for most folks, it feels like the struggle is far from over.

I remember chatting with a friend the other day who was shocked at how much more he’s paying for basics compared to just a few years ago. And he’s not alone. This disconnect between official statements and real-life experiences is at the heart of the current economic conversation.

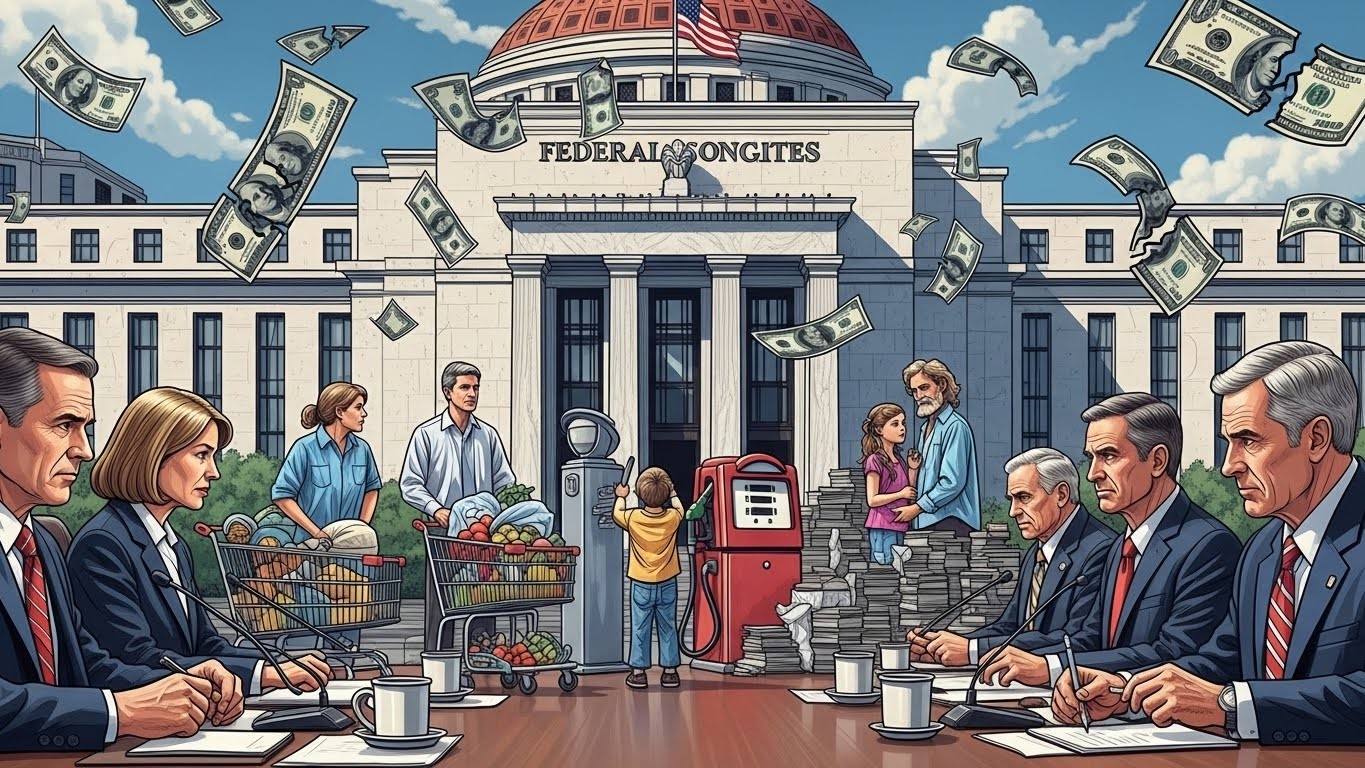

The Ongoing Clash Over Inflation Numbers

Right now, there’s a sharp divide in opinions about the state of price increases in the economy. Some advisors close to incoming leadership claim that certain market indicators show we’re pretty close to the ideal target. They even suggest more aggressive moves to lower borrowing costs to stimulate growth.

On the flip side, many central bank officials are pushing back. They’re highlighting data points that suggest pressures are still building, not easing. In fact, a significant portion of the key metrics they track are showing annual increases well above the desired level.

How can smart people look at the same information and come to such opposite conclusions? It’s a fair question, and it leads us straight to the heart of the issue.

Why the Official Data Feels So Detached from Reality

The truth is, the way we measure price changes in the U.S. has some serious flaws that have been around for years. These aren’t just minor tweaks; they’re fundamental problems that make the numbers look better than they actually are.

Take housing costs, for example. This is one of the biggest parts of the calculation, yet the figures used aren’t based on what people are really paying in the market. Instead, they’re estimates cooked up in a way that often smooths out sharp rises.

Then there’s the decision to leave out things like food and energy prices from the main indicators. Sure, those can be volatile, but they’re also essentials. Excluding them feels like ignoring the very things that hit household budgets the hardest.

The core measures are designed to strip out volatility, but in doing so, they strip out a big chunk of what real people experience every day.

And don’t get me started on healthcare. The official stats suggest insurance premiums rise modestly each year. But talk to anyone who’s renewed their policy lately—they’ll tell you it’s often double digits, year after year.

These adjustments aren’t accidents. Over time, changes to how we calculate these figures have consistently pushed the reported rates lower. It’s like painting a rosier picture to avoid facing tougher truths.

How Everyday Life Tells a Different Story

Think back a few generations. In the mid-20th century, many households managed comfortably on a single income. A family could own a home, a car, take vacations, and still save a bit—all without drowning in debt.

Fast forward to today. Most families need two full-time earners just to keep up. Add in mortgages, car payments, student loans, and credit card balances, and it’s clear something’s gone wrong.

If price increases were really as mild as reported over the decades, this shift wouldn’t make sense. Wages would have kept pace, and life would feel more secure, not less.

- Rising housing expenses forcing longer commutes or smaller homes

- Grocery bills that eat up a bigger share of take-home pay

- Healthcare costs that can wipe out savings in one emergency

- Education expenses burdening young adults for years

These aren’t abstract issues. They’re the reality staring millions in the face. In my view, perhaps the most telling sign is how many people live paycheck to paycheck, even with decent jobs.

It’s not about laziness or poor choices for most. The math just doesn’t add up anymore when costs have outrun income growth for so long.

What Happens When You Adjust for Real Purchasing Power

People often point to the stock market as proof that things are booming. And on the surface, it looks impressive—major indexes have climbed substantially over the past couple of decades.

But here’s where it gets interesting. Those gains are measured in dollars, and the dollar itself has lost a lot of value over time due to persistent price pressures.

When you measure stock performance against something more stable, like gold, the picture changes dramatically. Suddenly, those big gains shrink or even disappear in certain periods.

This isn’t just an academic exercise. It shows how nominal wealth can mask erosion in what that wealth can actually buy.

True wealth isn’t about how many dollars you have—it’s about what those dollars can purchase in the real world.

Markets seem to understand this on some level. Assets that can’t be printed endlessly, like precious metals, often move in ways that reflect deeper concerns about currency strength.

Broadening Pressures Beneath the Surface

Even within the preferred metrics, signs point to renewed momentum. Nearly half of the components in one key gauge are running hot on an annual basis.

This broadening suggests that price increases aren’t confined to a few areas anymore. They’re spreading across more goods and services, which makes them harder to dismiss as temporary.

Supply chain disruptions, labor shortages, and policy decisions all play roles. But the bigger issue is that the foundation has been weakening for years.

When borrowing costs stayed low for so long, it encouraged spending and debt that fueled higher prices. Now, unwinding that without pain is proving tricky.

- Initial shocks push prices up quickly

- Expectations adjust, leading to wage demands

- Businesses pass on higher costs to consumers

- The cycle reinforces itself unless broken decisively

Breaking that cycle requires tough choices, but acknowledging the true extent of the problem is the first step.

Looking Beyond the Headlines for Clues

Alternative measures often paint a starker picture. Some market-based indicators that aren’t as heavily adjusted show much higher rates.

Consumer surveys consistently report feeling the pinch more than official data admits. When people say they’re cutting back on non-essentials, that’s a signal worth heeding.

In my experience following these trends, the gap between reported figures and lived reality tends to widen during certain policy environments. It’s almost as if the numbers are engineered to support specific narratives.

Whether intentional or not, the result is the same: decisions get made based on incomplete or misleading information.

The Bigger Picture of Declining Standards

Zoom out, and the pattern becomes clear. Since the 1970s, the cost of maintaining a middle-class lifestyle has risen faster than most incomes.

Homeownership rates, adjusted for quality and location, tell part of the story. So do savings rates and debt levels.

Families delay milestones like marriage or kids because the economics don’t work. That’s not just personal choice—it’s a response to structural pressures.

| Era | Typical Household | Financial Pressure |

| 1950s-1960s | Single earner common | Low debt, rising savings |

| 1980s-1990s | Dual incomes rising | Moderate debt growth |

| Today | Dual incomes necessary | High debt, low savings |

This table simplifies it, but the trend is unmistakable. Progress in some areas hasn’t offset erosion in affordability for basics.

Technology and globalization brought benefits, no doubt. But they’ve also contributed to wage stagnation in many sectors while asset prices soared.

What This Means Moving Forward

Debates at the policy level will continue, but individuals can’t wait for consensus. Protecting purchasing power requires looking at assets that hold value over time.

Precious metals have historically served this role during periods of currency weakness. They’re not perfect, but they offer a hedge against the very issues we’re discussing.

Other strategies include focusing on real assets, diversifying away from pure dollar exposure, and staying informed about underlying trends.

The key is recognizing that official narratives don’t always match ground truth. When they diverge too far, it’s time to trust your own observations.

In the end, economic health isn’t just about GDP numbers or stock highs. It’s about whether average people can build secure, fulfilling lives without constant financial stress.

Until that reality aligns better with the data we’re fed, skepticism remains warranted. And perhaps that’s the most important takeaway from this whole debate.

What do you think—is the inflation battle really won, or are we missing something bigger? The evidence from daily life suggests the latter, and ignoring it comes at our collective peril.