Have you ever wondered what it feels like when prices just keep creeping up, month after month, without much relief in sight? In Japan, that’s been the reality for nearly four years now. It’s the kind of stubborn inflation that keeps economists and policymakers on their toes, debating the next big move.

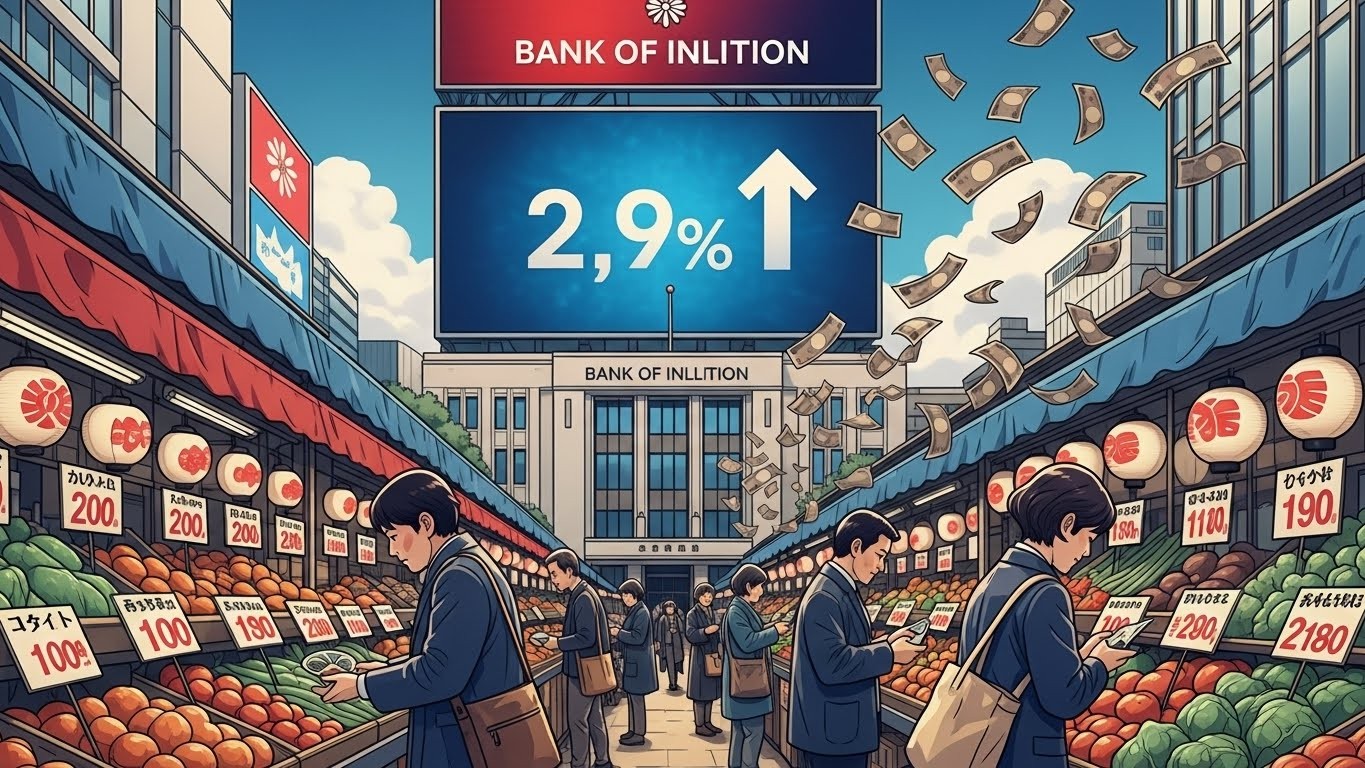

The latest numbers show consumer prices rising 2.9% in November compared to a year ago. That’s down a touch from previous months, but still comfortably above the central bank’s longtime goal. And it’s not a one-off – this marks the 44th consecutive month of inflation running hot.

Persistent Inflation Strengthens the Case for Higher Rates

Let’s dive into what these figures really mean. The headline inflation rate eased slightly, yet the core measure – which excludes volatile fresh food prices – held steady at 3%. That’s exactly what many analysts expected, but it doesn’t diminish the broader trend.

Even the “core-core” reading, stripping out both food and energy, only dipped marginally to 3%. In my view, this kind of resilience suggests inflation isn’t ready to fade quietly into the background. It’s embedded deeper than some might hope.

Why the Central Bank Targets 2%

For years, Japan’s central bank chased that elusive 2% target, battling deflationary forces that weighed on growth and wages. Achieving it sustainably was seen as a victory. Now that it’s overshot for so long, the conversation has shifted dramatically.

A rate hike seems increasingly likely as policymakers wrap up their latest meeting. If it happens, rates could reach levels not seen since the mid-1990s. That’s a big shift for an economy long accustomed to near-zero or negative interest rates.

But here’s the tricky part: hiking rates too aggressively could squeeze an economy that’s already showing signs of weakness. Recent revisions to third-quarter GDP painted a gloomier picture – a sharper contraction than initially thought.

The Delicate Balancing Act

Imagine walking a tightrope. On one side, you have inflation that’s proving stickier than expected. On the other, growth that’s faltering. Fall too far either way, and the consequences could be painful.

The central bank has to normalize policy without derailing recovery. It’s a fine line, and they’ve acknowledged as much. Avoiding premature tightening is key, especially when domestic demand remains fragile.

Raising rates could help bring inflation closer to target, but the economy’s potential growth needs support through fiscal measures and structural reforms.

That’s the essence of recent comments from officials. There’s recognition that higher rates might become more natural if the economy’s underlying strength improves. But rushing the process risks unnecessary pain.

Economic Growth Concerns Loom Large

The revised GDP figures were sobering. The economy shrank more than first reported in the third quarter, highlighting vulnerabilities. Consumer spending, exports, and investment all face headwinds.

Against this backdrop, calls for proactive fiscal spending have grown louder. Some political figures advocate looser monetary conditions to support growth and revenues. It’s a classic debate: monetary versus fiscal tools.

In my experience following these developments, Japan often stands out for its cautious approach. They’ve learned hard lessons from past policy missteps. That prudence might serve them well now.

- Quarter-on-quarter contraction deepened to 0.6%

- Annualized decline reached 2.3%

- Domestic demand showed particular weakness

- External factors added pressure

These numbers underscore why timing matters so much. A rate increase could strengthen the yen further, potentially hurting exporters. Yet letting inflation run unchecked risks eroding purchasing power over time.

Understanding the Neutral Rate Debate

One concept that’s gained attention lately is the neutral rate – the theoretical level where policy neither stimulates nor restricts growth. Officials have suggested that boosting potential growth could naturally elevate this rate.

If that happens, higher policy rates would make sense without being restrictive. It’s an interesting perspective: structural reforms and fiscal support paving the way for sustainable normalization.

Estimates vary, but some place Japan’s neutral rate in the 1% to 2.5% range. Getting there gradually, without shocks, seems to be the preferred path. Abrupt moves could undermine confidence.

If the neutral rate rises through enhanced growth potential, it would be natural for policy rates to follow.

– Central bank official

Perhaps the most fascinating aspect is how intertwined monetary and fiscal policies have become. Coordination, or lack thereof, could significantly influence outcomes.

Market Reactions and Currency Moves

Financial markets wasted no time responding to the inflation data. The yen firmed up slightly, reflecting heightened rate hike expectations. Currency traders often lead the charge on these releases.

Bond yields edged higher too, pricing in tighter policy ahead. Equity markets showed mixed reactions – some sectors benefit from controlled inflation, others suffer from higher borrowing costs.

Globally, Japan’s path matters. As a major economy, shifts in its policy can ripple through trade partners and commodity prices. The yen’s value affects everything from tourism to manufacturing competitiveness.

Looking Ahead: What Might Come Next

With the policy meeting concluding soon, all eyes are on the decision and accompanying statement. Will they hike now, signal for January, or hold steady while preparing markets?

Communication will be crucial. Clear guidance on the pace of normalization could ease volatility. Surprises, on the other hand, tend to spark sharp reactions.

Longer term, wage growth remains a critical piece of the puzzle. Sustainable inflation needs accompanying rises in incomes. Recent negotiations have shown promise, but momentum must build.

- Monitor upcoming wage talks

- Watch for fiscal budget details

- Track global commodity trends

- Assess domestic consumption indicators

- Follow central bank speeches for clues

These elements will shape the trajectory. In many ways, Japan is navigating uncharted waters – exiting ultra-easy policy after decades.

It’s easy to focus solely on rates, but the bigger story is about achieving balanced, durable growth. Inflation above target is progress from deflation, yet managing the transition thoughtfully is essential.

Personally, I’ve always found Japan’s economic journey compelling. From the lost decades to this tentative normalization, there’s a resilience that’s often underestimated. The coming months could prove pivotal.

Whether rates rise imminently or gradually, the commitment to 2% stability appears firm. How they get there without unnecessary disruption – that’s the real test.

One thing seems clear: after 44 months above target, the era of extraordinary accommodation is drawing to a close. Carefully, deliberately, but unmistakably.

And maybe that’s not such a bad thing. Controlled inflation, higher rates, stronger wages – it could mark the foundation for renewed vitality. Time will tell, but the signs are intriguing.

(Word count: approximately 3450)