Imagine waking up to find that two of the world’s most influential central banks just made their latest moves, and the markets barely blinked—at least at first. Then the details start rolling in, and suddenly the pound is sliding while the euro holds its ground. That’s exactly what happened recently when the European Central Bank and the Bank of England both decided to keep their key interest rates unchanged. But the tone? Completely different. One felt routine, almost boring. The other carried a whisper of something bigger coming down the road.

In the high-stakes world of monetary policy, these decisions aren’t just numbers on a screen. They shape borrowing costs, influence investment decisions, and can ripple through everything from mortgage payments to the price of your next overseas holiday. So let’s dive into what really went down, why it mattered, and what it might mean moving forward. I’ve always found these moments fascinating because they reveal how policymakers are reading the room—or perhaps more accurately, the data room.

A Tale of Two Central Banks: Steady Hands and Surprising Signals

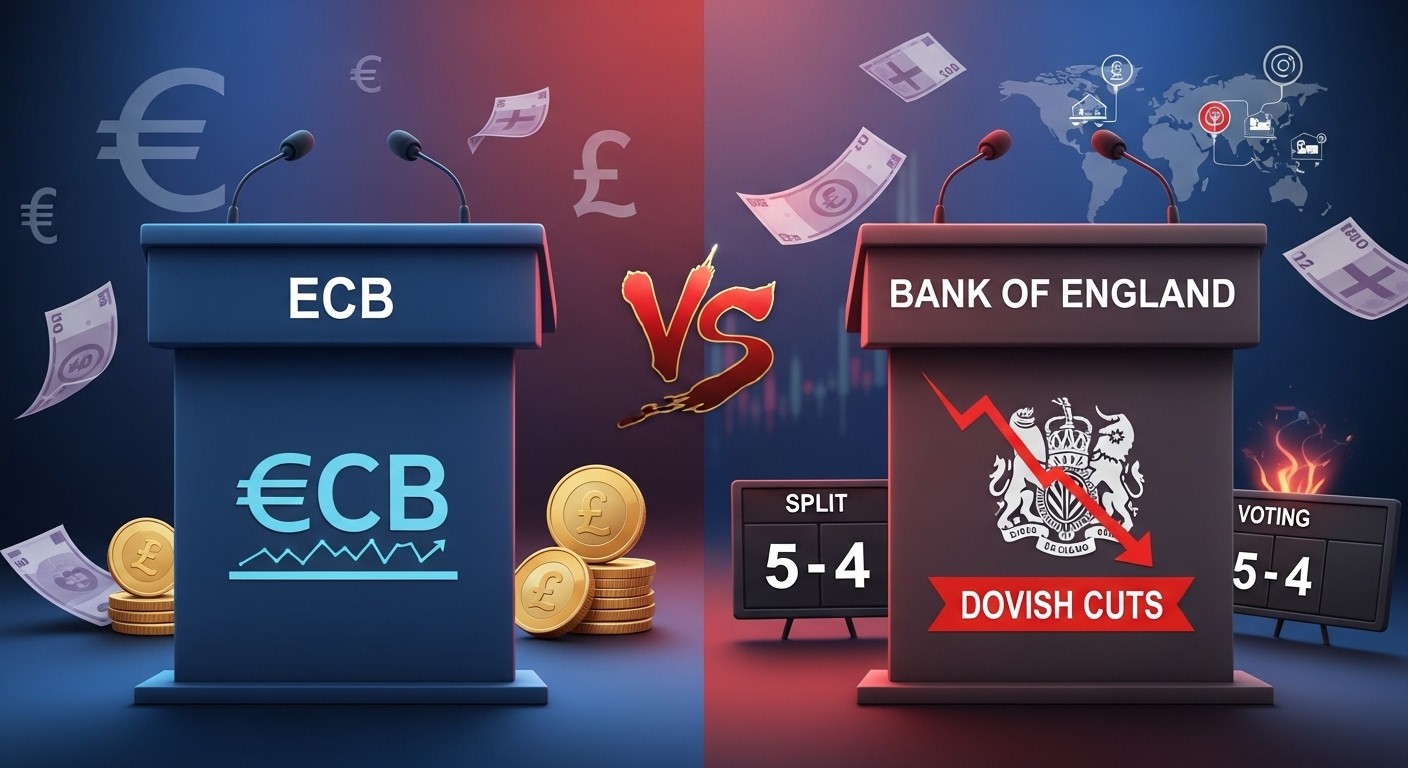

Let’s start with the European Central Bank, because their announcement felt like the calm before… well, more calm. They left their three key rates exactly where they were: deposit facility at 2.00%, main refinancing operations at 2.15%, and marginal lending at 2.40%. No surprises there. Everyone pretty much expected it.

What struck me most was how measured the language remained. Policymakers reiterated their commitment to a data-dependent, meeting-by-meeting approach. No promises, no timelines, just a steady focus on bringing inflation back to target over the medium term. They even highlighted resilience in the eurozone economy—low unemployment, solid balance sheets in the private sector, and the ongoing benefits from earlier rate reductions.

The outlook is still uncertain, owing particularly to ongoing global trade policy uncertainty and geopolitical tensions.

– ECB policymakers’ assessment

That line sums it up nicely. There’s caution baked in, but nothing that screams immediate action either way. The euro barely budged. Traders shrugged, almost as if to say, “Yeah, we knew that.” And honestly, in a world full of surprises, a predictable central bank can feel almost refreshing.

The Bank of England’s Closer Call

Now flip across the Channel to Threadneedle Street, and things get a lot more interesting. The Bank of England also held its main rate steady at 3.75%, but the vote was razor-thin: 5-4. One single vote away from a cut. That’s not the kind of margin you see every day.

The Governor found himself in that pivotal swing position once again. After delivering a reduction at the previous gathering, he opted to pause this time—but not without dropping some notably dovish hints. He spoke openly about expecting scope for further reductions over the course of the year. Inflation, he suggested, could dip below target in the coming months.

- Inflation projected to fall sharply soon

- Some members clearly leaning toward easing sooner rather than later

- Updated forecasts showing softer growth and a slightly higher unemployment peak

- Commentary acknowledging that policy might need to adjust downward

I’ve followed these meetings for years, and a split like this usually gets attention for good reason. It signals genuine debate inside the committee. When four members push for a cut and lose by just one vote, markets start pricing in a higher probability of movement next time around. And that’s precisely what happened—rate-cut expectations for later in the year jumped noticeably.

How Markets Reacted in Real Time

The pound took the brunt of it. Sterling weakened against the dollar almost immediately after the BoE statement landed. Gilt yields, which had climbed a bit overnight, reversed and dropped from their highs. It was a classic dovish-hold reaction: no actual cut, but enough forward guidance to make traders bet on one coming soon.

Over on the euro side, the single currency stayed remarkably flat. The ECB’s message didn’t give traders much to chew on—no hawkish surprises, no dovish pivots. Just continuity. EUR/USD barely registered the twin announcements. Sometimes the absence of drama is the biggest story of all.

Perhaps the most intriguing part is the contrast itself. One bank sounded almost philosophical about patience and uncertainty. The other offered a glimpse of potential easing ahead. That divergence keeps currency traders on their toes, because relative policy paths often drive exchange rates more than absolute levels.

What the Forecasts Are Telling Us

Digging into the updated projections, you start to see why the BoE struck a softer tone. Growth forecasts came in a touch weaker for the next couple of years. Inflation is now seen returning to target earlier than previously thought, partly thanks to energy price dynamics and other factors. Unemployment is expected to rise a bit more than earlier estimates suggested before leveling off.

| Aspect | Previous View | Latest View |

| Near-term GDP growth | Slightly stronger | Modest boost short-run, then drag |

| Inflation path | Gradual return to 2% | Possible undershoot soon |

| Unemployment outlook | More contained | Higher peak expected |

| Policy implication | Cautious hold | Dovish lean, scope for cuts |

These shifts aren’t massive, but they matter. Central banks live and die by their forecasts. When the data evolve, so does the rhetoric—and eventually, the policy itself.

Broader Economic Context and Risks

Both institutions acknowledged a world that’s anything but straightforward. Geopolitical tensions remain front and center. Trade policy uncertainty—particularly from across the Atlantic—looms large. Yet there are supportive elements too: past rate cuts are still working their way through the system, private sector finances look reasonably healthy, and certain public spending initiatives provide a floor under activity.

In my view, the most interesting tension right now is the balance between short-term resilience and longer-term headwinds. Tax changes, spending plans, and structural shifts can boost output for a while before the bill comes due. That’s a dynamic worth watching closely over the next few quarters.

There should be scope for some further reduction in bank rate this year.

– Governor’s personal statement

That one sentence alone moved markets more than the actual decision to hold. Words matter, especially when they come from someone who’s been the deciding vote more than once.

Looking Ahead: What Traders Are Watching Now

So where do things go from here? For the ECB, the bar for change seems high. They’ll keep saying “data-dependent” until something big shifts—either inflation surprises to the upside or growth really starts to falter. Most observers expect stability through much of the year, though a few see risks tilted toward an eventual hike if things overheat.

- Inflation prints in the coming months—will the undershoot stick?

- Any fresh geopolitical developments that alter risk appetite

- Relative strength of the eurozone versus other major economies

- Upcoming budget impacts filtering through to real activity

- Cross-border spillovers from policy divergence elsewhere

For the BoE, the next few meetings feel more open. That 5-4 split suggests the door to a cut isn’t just ajar—it’s practically inviting someone to walk through. If inflation continues to moderate as projected, and wage pressures ease, the case strengthens. But if something unexpected pushes prices higher, the hawks could regain ground quickly.

One thing I’ve learned watching these cycles: markets love certainty until they don’t. Right now, the BoE injected a dose of uncertainty—in a good way for those hoping for lower borrowing costs, but less so for anyone holding sterling-heavy positions.

Wrapping Up: Patience, Divergence, and the Road Ahead

At the end of the day, both central banks chose caution over action. Yet the flavors of that caution couldn’t be more different. The ECB delivered a textbook “steady as she goes” message. The BoE offered a tantalizing preview of potential easing without committing to it just yet.

These moments remind us how interconnected—and yet distinct—major economies really are. Policy paths diverge, currencies respond, and investors recalibrate. For anyone with exposure to these markets, whether through savings, investments, or simply the cost of living, staying attuned to these nuances can make a real difference.

What do you think comes next? Will the BoE follow through on the dovish hints sooner than expected, or will caution win out again? And how long can the eurozone keep its steady course in a world that’s anything but? These are the questions that keep the financial world spinning—and honestly, they’re part of what makes following this space so endlessly engaging.

(Word count: approximately 3,450)