Have you ever looked at the latest economic headlines and felt like they were talking about some parallel universe? The stock market hits records, unemployment stays low, yet your grocery bill still stings and saving feels impossible. You’re not alone in that disconnect. Lately, I’ve noticed more people whispering about how the recovery just doesn’t feel real for most families. And economists are starting to give that feeling a name: the E-shaped economy.

It’s a subtle but important shift from what we heard so much about last year—the K-shaped recovery, where the wealthy soared upward while everyone else lagged behind. Now, in 2026, the picture has more layers. Three distinct groups are emerging in how people spend, save, and stress about money. The top keeps powering ahead, the middle holds on tightly, and the bottom leans heavily on credit. Understanding this new shape isn’t just academic; it explains why so many feel trapped despite “good” numbers on paper.

The Rise of the E-Shaped Economy in 2026

What exactly does an E-shaped economy look like? Picture the letter E: one strong upward line at the top representing high earners, then two horizontal bars below—one flat for the middle class barely staying afloat, and one dipping or struggling at the bottom. Unlike the simpler K split of recent years, this model captures a more nuanced reality. The top 20 percent or so drives most consumption growth, while the middle and lower groups face mounting pressure from prices that never really came back down.

I’ve followed economic trends for years, and this feels different. It’s not a full collapse, but it’s also not the broad-based boom many hoped for after the turbulence of prior years. Instead, we see pockets of strength alongside quiet strain. Consumer confidence surveys keep trending lower, even as spending overall holds up. That paradox points directly to the uneven way recovery has unfolded across income levels.

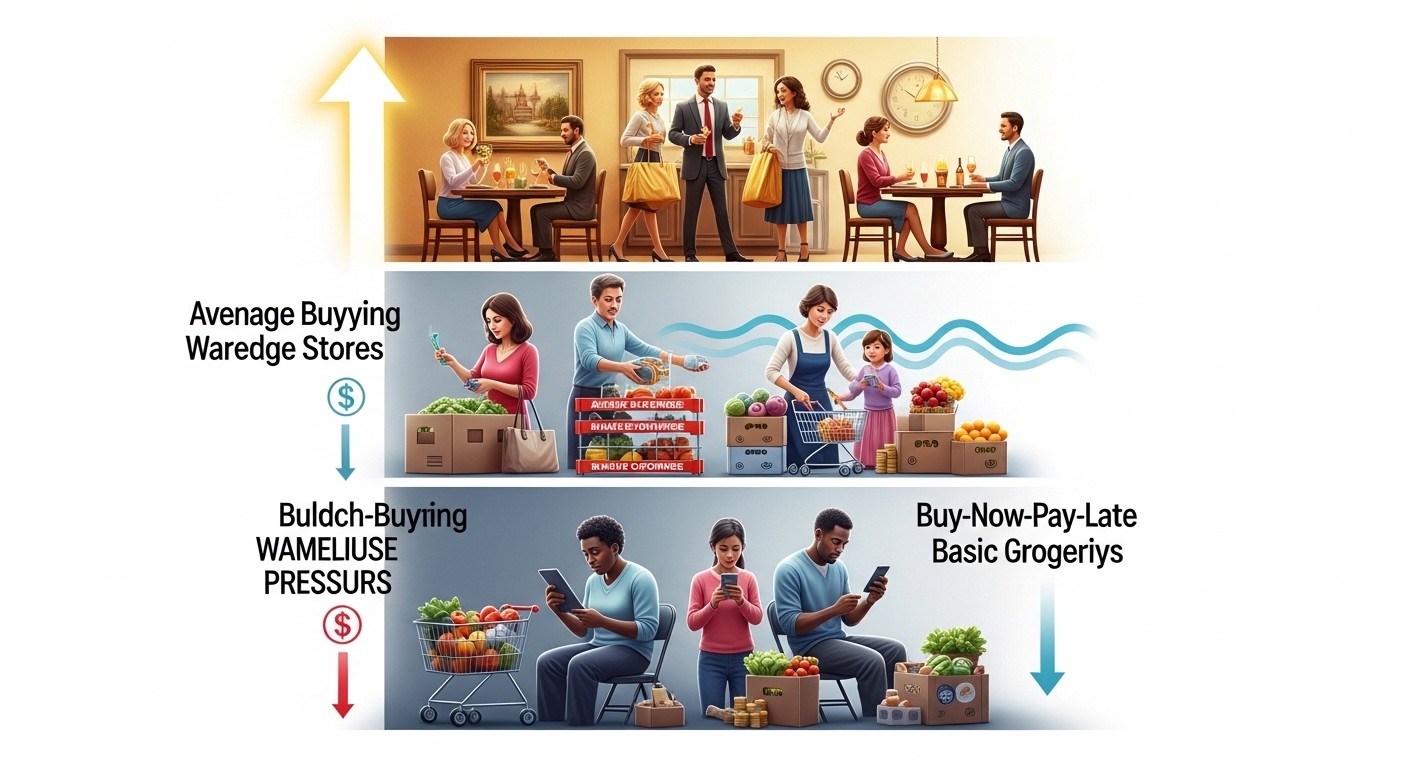

Top Tier: High Earners Keep Driving the Engine

At the top of this E shape sit the highest earners—households comfortably above six figures, often much higher. These are the people still booking premium vacations, upgrading to luxury versions of everyday items, and generally not sweating price tags too much. Recent analyses show this group accounts for nearly 60 percent of total consumer spending in the country. That’s a staggering concentration of purchasing power.

Businesses have noticed. Airlines, hotels, restaurants, and even credit card companies roll out more exclusive perks and higher-end offerings. Annual fees on premium cards climb higher, yet demand stays strong among those who qualify. It’s smart business—catering to the segment that can and will pay more. In a way, it’s fascinating to watch. Companies move upmarket because that’s where the reliable growth lives right now.

But here’s a personal observation: this top tier’s strength masks weakness elsewhere. When headlines celebrate robust consumption, they’re often reflecting decisions made in boardrooms and luxury boutiques rather than at kitchen tables across suburbia. That disconnect breeds frustration. People read about economic strength and wonder why their own budget feels tighter than ever.

The wealthiest consumers continue fueling growth, but their habits don’t reflect the daily reality for most households.

— Economic observer

Exactly. The top keeps the aggregate numbers looking healthy, yet it leaves huge swaths of the population feeling overlooked.

Middle Tier: Treading Water in the Costco Economy

Now we reach the flat bar in the middle—the group that defines so much of the E shape. These are middle-income households, often earning between roughly $50,000 and $150,000 depending on location and family size. They’re not destitute, but they’re far from secure. Necessities eat up most of each paycheck, leaving little margin for error or enjoyment.

One term I’ve seen gaining traction is the “Costco economy.” Families stock up in bulk, hunt for deals, switch to generic brands, and generally stretch every dollar. It’s not panic buying, but it’s careful, almost nervous spending. They still purchase what they need—groceries, gas, school supplies—but discretionary purchases get delayed or downsized. Eating out becomes a rare treat rather than routine.

- Bulk shopping at warehouse clubs becomes the default for staples

- Subscription services get scrutinized and often canceled

- Home-cooked meals replace restaurant visits whenever possible

- Impulse buys give way to deliberate comparison shopping

- Many delay major purchases like appliances or car repairs

This cautious approach keeps bills paid, but it also creates a constant low-level stress. Every few months, something spikes—beef one month, utilities the next, car insurance after that. It’s like playing whack-a-mole with inflation. Wages haven’t kept pace with these jumps, so families feel stuck running in place.

In my view, this middle group carries the heaviest emotional load. They’re close enough to the top to see what’s possible, yet far enough from stability to feel perpetually vulnerable. That tension shows up in surveys: consumer sentiment remains stubbornly low despite headline economic wins. People know the data says things are “fine,” but their lived experience tells a different story.

Bottom Tier: Relying on Debt to Bridge the Gap

At the lower end of the E, things get tougher. Lower-income households face the steepest challenges. Wages stagnate relative to costs, so many turn to credit cards, installment loans, and buy-now-pay-later plans to cover essentials. It’s not luxury spending—it’s groceries, rent, utilities, and sometimes medical bills.

Data shows higher rates of carrying credit card balances among lower earners. Buy-now-pay-later usage has surged for everyday items, with some surveys noting a jump in people using these tools for food. Late payments also rise in this group, signaling real strain. It’s a fragile way to manage, and one missed paycheck or unexpected expense can tip the balance.

Tax refunds offer temporary relief for some. Many plan to use at least part of any refund to pay down debt. Yet even sizable checks provide only short-term breathing room. The underlying affordability issues—housing, health care, education—persist year after year. Without structural changes, the bottom tier remains vulnerable.

Debt becomes a lifeline when income can’t cover basics, but it often creates a cycle that’s hard to escape.

That’s the harsh truth. Short-term fixes rarely solve long-term mismatches between earnings and expenses.

Why the Shift from K to E Matters So Much

The move from a K-shaped to an E-shaped picture isn’t just semantics. It highlights how the middle class—long considered the backbone of the economy—is now showing distinct signs of fatigue. In the K model, the divide felt binary: winners and losers. Now we see three groups, and the middle one’s behavior reveals growing cracks.

Perhaps the most concerning aspect is the erosion of financial confidence. When people feel they must shop nervously, delay dreams, or rely on credit for necessities, optimism fades. That mindset affects everything—spending decisions, job mobility, family planning, even mental health. A nervous middle class doesn’t invest in the future the same way; they protect what they have.

Businesses feel it too. Retailers catering to the middle see slower sales on standard items while premium lines boom. Discount chains gain traffic, but overall growth becomes lopsided. An economy overly dependent on the top tier risks instability if that group ever pulls back—even slightly.

- Track personal spending patterns to identify “nervous” habits early

- Build a small emergency fund, even if contributions are modest

- Reevaluate subscriptions and recurring costs ruthlessly

- Explore side income streams to ease pressure on main earnings

- Consider debt consolidation or balance transfers if carrying high-interest balances

- Stay informed about economic shifts without obsessing over daily headlines

- Focus on long-term financial health over short-term comfort

These aren’t revolutionary ideas, but in an E-shaped world, small disciplined steps matter more than ever. Waiting for broad relief may take too long.

Looking Ahead: Can the Middle Catch a Break?

So where does this leave us in the months and years ahead? Optimists point to cooling inflation, potential policy adjustments, and possible wage gains in certain sectors. Pessimists warn that structural issues—housing shortages, health care costs, education debt—won’t vanish quickly. Reality likely lies somewhere in between.

One hopeful sign: tax season sometimes delivers meaningful refunds that help chip away at debt or rebuild savings. But refunds aren’t income; they’re delayed earnings. Sustainable improvement requires wages to outpace prices consistently, something that hasn’t happened broadly in recent memory.

In my experience watching these cycles, the middle class has incredible resilience. Families adapt, innovate, and find ways to stretch resources. Yet resilience has limits. If the E shape hardens—top pulling further away, middle flattening more, bottom sinking deeper—social and economic stability could suffer.

That’s why conversations about the E-shaped economy matter. They force us to look beyond averages and recognize real differences in lived experience. Only then can we push for policies, business practices, and personal strategies that narrow the gaps rather than widen them.

At the end of the day, economic shapes are just metaphors. They help us visualize complex realities. But behind every data point is a person making tough choices—whether to splurge on premium coffee, buy generic cereal, or put groceries on credit. Recognizing the E shape doesn’t solve those dilemmas, but it at least validates the feeling that something’s off. And sometimes, simply knowing you’re not imagining the strain is the first step toward navigating it better.

What do you think—does the E-shaped description match your own financial reality right now? I’d love to hear how you’re coping in the comments below.