Have you ever stopped to wonder what happens to the life you’ve built when it’s time to pass it on to your loved ones? For many New Yorkers, that question just got a lot more complicated—and a lot more expensive—if certain proposals in Albany gain traction.

Picture this: a hardworking family in Queens or Brooklyn finally pays off their modest home after decades of sacrifices. Maybe they’ve tucked away some savings in retirement accounts or invested wisely over the years. In the current system, they could reasonably expect to leave most of that to their children without the government taking a massive bite. But a bold new idea floating around could change everything, dropping the protected amount way down and ramping up the rates on what’s left.

I’ve been following fiscal debates in big cities for years, and this one stands out because it feels personal. It isn’t just about balancing books on paper—it’s about how we value hard-earned success and the simple act of providing for the next generation. Let’s dive into what’s being suggested, why it’s happening, and what it might really mean for everyday people.

The Big Idea Shaking Up New York’s Fiscal Landscape

New York City is staring down a significant budget challenge, with projections showing gaps in the billions for the coming years. In response, city leadership has put forward a series of revenue ideas to state officials, hoping to bridge shortfalls without solely relying on local property adjustments or reserve draws.

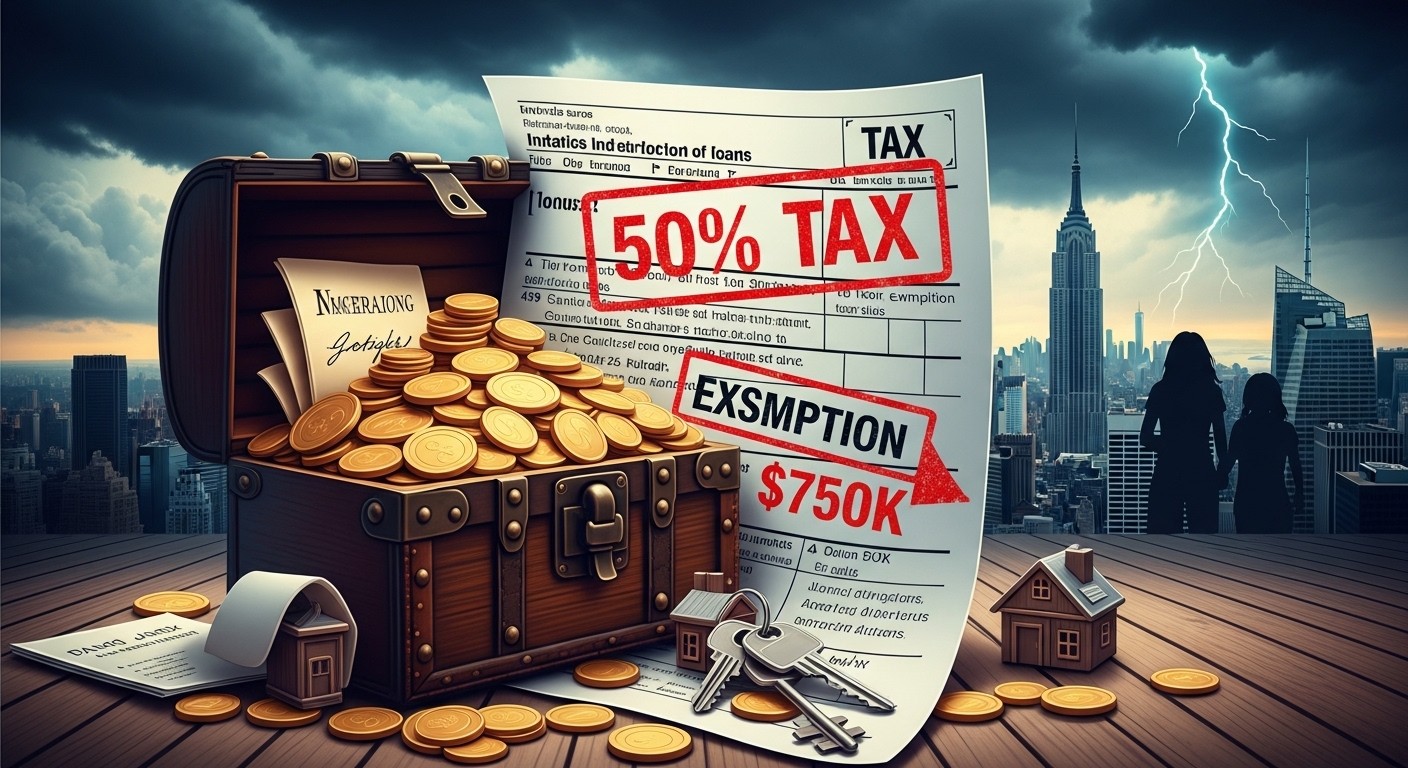

Among the most striking suggestions is a major rewrite of how the state handles estate taxes. Currently, estates below a certain high threshold—roughly over seven million dollars—pass to heirs with little to no state-level tax hit. The proposal would slash that safe zone dramatically, potentially exposing many more families to taxation right from the start.

At the same time, the top rate on larger amounts could jump substantially. Think of it like moving the goalposts in a game where the stakes involve your family’s future security. I’ve always believed that tax policy should encourage building wealth, not punish those who manage to accumulate a nest egg through years of effort.

The way we tax inheritances says a lot about what kind of society we want to be—one that rewards diligence or one that keeps redistributing at every turn.

This isn’t abstract policy talk. For a homeowner in a decent neighborhood where property values have climbed steadily, that family residence alone could push an estate over the new proposed line. Add in life insurance, savings, or a small business, and suddenly middle-class families find themselves in the crosshairs of what was traditionally aimed at the ultra-wealthy.

Breaking Down the Proposed Changes

Let’s get specific without getting lost in jargon. The current setup allows a generous exemption before any state estate tax kicks in. Under the new vision, that floor drops sharply to around three-quarters of a million dollars. That’s a reduction of nearly ninety percent in the protected amount.

On top of that, the highest marginal rate could rise from sixteen percent all the way to fifty percent. Combined, these shifts are estimated to pull in several billion dollars annually if enacted. Proponents see it as a fair way to ask more from those with greater resources during tight budget times.

But here’s where it gets tricky—and where my skepticism creeps in. Tax systems often have “cliffs,” meaning once you cross a threshold, the rate applies to the entire estate, not just the excess. That mechanic could create painful surprises for families who never considered themselves rich by any stretch.

- Exemption threshold slashed from over $7 million to $750,000

- Top tax rate potentially tripling to 50 percent

- Broader impact on homes, savings, and small business assets

- Projected revenue in the billions for state and city coffers

Imagine a retired couple whose apartment in a rising market is now valued at $900,000, plus $300,000 in other assets. Under the old rules, they might skate by tax-free at the state level. Under the new ones? A substantial bill could land on their heirs at a time when they’re already grieving.

Why This Push Now? Understanding the Budget Pressure

Cities like New York don’t operate in a vacuum. Expenses for everything from education and housing support to public services keep climbing, sometimes outpacing revenue growth even when the local economy shows strength in areas like finance.

Recent forecasts point to a gap of at least $5.4 billion that needs closing in the near term, with longer-term cumulative shortfalls potentially reaching much higher. Credit watchers have taken notice, shifting outlooks to reflect concerns about structural imbalances and less room to maneuver if things tighten up economically.

In my view, persistent deficits like these force tough conversations. Do you keep raising the bar on what counts as “wealthy” and extract more, or do you look harder at spending priorities and efficiency? The proposals on the table lean heavily toward the former.

Other ideas circulating alongside the estate changes include adjustments to business taxes targeted at the city level, tweaks to how certain business owners offset personal liabilities, and higher income contributions from top earners. There’s also talk of surcharges on high-value real estate deals and even removing exemptions on precious metals purchases.

Taken together, these could generate several billion more each year according to city estimates. Yet the estate piece feels especially weighty because it touches on something deeply human: the desire to provide stability beyond your own lifetime.

Potential Ripple Effects on Families and the Economy

Let’s think practically. New York already has one of the more aggressive approaches to estate taxation compared to many other states. Lowering the bar this much could make it one of the toughest nationally. Families might start reconsidering where they live, work, or invest as retirement approaches.

I’ve spoken with folks in financial planning circles who worry this could accelerate out-migration of successful professionals and entrepreneurs. Why build substantial assets here if a big chunk disappears upon transfer? That kind of brain and capital drain isn’t easy to reverse.

Tax policy isn’t just numbers—it’s incentives that shape behavior over decades.

On the flip side, supporters argue that public services benefit everyone, and those who’ve done well should contribute more when the city faces genuine strains. Schools, transit, and social programs don’t fund themselves, after all. The debate often boils down to fairness: what does “fair share” really look like in practice?

Consider a small business owner who poured everything into their company for forty years. The business might be valued modestly by corporate standards but enough to trigger the new rules. Heirs could face liquidity issues just to pay the tax bill, sometimes forcing sales or loans at inopportune times.

- Immediate hit to family wealth transfer

- Possible incentives to relocate assets or residency

- Challenges for illiquid estates like family homes or businesses

- Broader questions about long-term economic competitiveness

Comparing to Federal Rules and Other States

It’s worth noting that the federal estate tax has its own exemption, currently much higher and subject to its own political winds. But states can layer on additional burdens, and New York’s proposal would make its version notably more punitive at lower levels.

Some states have no estate tax at all, creating a patchwork that already influences where people choose to retire or establish trusts. A move like this could widen those differences further, potentially making neighboring areas more attractive for wealth preservation.

Perhaps the most interesting aspect is how these changes interact with inflation and rising asset prices. What felt like a comfortable cushion years ago might not hold the same value today, yet tax thresholds don’t always keep pace unless deliberately adjusted.

Real-World Scenarios That Hit Close to Home

Let’s walk through a couple of hypothetical but realistic examples. First, a teacher and a nurse couple who bought their Staten Island home decades ago. Through appreciation and careful saving, their estate sits around $1.2 million at passing. Under current rules, likely no state estate tax. Under the proposal? A taxable event that could reduce what their kids receive by a meaningful percentage.

Or take a small retail shop owner in the Bronx whose business and property together total $2 million. The family might need to scramble to cover taxes, possibly disrupting continuity or forcing a quick sale. These aren’t tales of billionaires dodging responsibility—they’re stories of ordinary ambition meeting unexpected government claims.

| Scenario | Current Exemption Impact | Proposed Change Impact |

| Modest family home + savings ($1M total) | Usually tax-free at state level | Potentially taxable with high marginal rate |

| Small business estate ($3M) | Protected below threshold | Large tax bill possible on full amount |

| High-value urban property ($6M+) | Taxed only on excess | Higher rates and lower floor amplify burden |

Numbers like these make the abstract feel concrete. They remind us that policy decisions ripple outward in ways that affect daily lives and long-term planning.

Other Revenue Ideas on the Table

The estate overhaul doesn’t stand alone. There’s discussion around lifting corporate rates for firms based in the city, with financial companies facing one level and others another. Unincorporated businesses above certain earnings might see modest bumps too.

Then come adjustments to pass-through credits that currently help business owners manage their overall tax load. Scaling those back could bring in hundreds of millions more. And for high earners, an increased local income tax contribution remains on the wishlist, potentially adding billions if approved.

Real estate gets attention as well: surcharges on luxury sales or cash transactions, plus tweaks to mansion-style taxes. Even the sales tax treatment of gold and precious metals could shift, closing what some see as a loophole.

Each piece aims to spread the load, but critics worry the cumulative effect could discourage investment and entrepreneurship precisely when the city needs them most to generate organic growth.

Credit Concerns and Longer-Term Fiscal Health

Rating agencies have flagged worries about these persistent gaps. A recent shift to a negative outlook highlights how expenses seem to outrun revenues structurally, even in relatively good economic times. Using reserve funds helps in the short run but leaves less buffer for downturns.

I’ve found that when fiscal flexibility shrinks, cities sometimes double down on tax ideas rather than reforming spending or seeking efficiencies. Whether that’s the wisest path depends on your perspective, but the signals from bond watchers suggest caution is warranted.

Over four years, some analyses point to cumulative pressures exceeding $28 billion. That kind of figure doesn’t get resolved with one-time fixes—it requires sustained attention to both sides of the ledger.

What This Could Mean for Your Personal Planning

If you’re reading this and thinking about your own situation, now might be a good moment to review estate strategies with professionals. Tools like trusts, gifting during life, or life insurance policies structured carefully can sometimes mitigate impacts, though rules can change and nothing is guaranteed.

Younger professionals building careers here should consider how these dynamics might affect their future decisions about staying or moving when family responsibilities grow. Location choices increasingly factor in tax climates alongside lifestyle and opportunity.

Perhaps most importantly, these conversations highlight broader questions about incentives. Do we want a system where success is celebrated and preserved across generations, or one where the state plays a heavier redistributive role at every stage?

In my experience, people respond to carrots more enthusiastically than to sticks when it comes to long-term economic behavior.

The Political and Practical Realities Ahead

As budget negotiations unfold, not every idea makes it through. Some legislative bodies have shown interest in income and corporate adjustments but appear cooler on the most aggressive estate revisions so far. Governors and lawmakers weigh competing priorities, including economic competitiveness and voter sentiment.

Still, the fact that these concepts are on the table at all signals a willingness to push boundaries. Public reaction has been mixed, with some praising the focus on equity and others warning of unintended consequences like reduced philanthropy or accelerated exits by high-net-worth individuals.

Watch closely as details evolve. Small tweaks in language can have outsized effects once laws pass and implementation begins.

Broader Lessons for Tax Policy Nationwide

New York often serves as a bellwether for urban policy experiments. What happens here can influence thinking in other high-cost cities facing similar pressures from housing, migration, and service demands.

The tension between raising revenue aggressively and maintaining an environment where people want to create and retain wealth is universal. Get the balance wrong, and you risk slower growth that ultimately hurts the very programs taxes are meant to support.

I’ve come to believe that sustainable fiscal health comes from broadening the economic base rather than narrowing the definition of who pays more. Encouraging investment, innovation, and retention tends to grow the pie instead of just slicing it differently.

- Encourage long-term residency and business formation

- Balance revenue needs with growth incentives

- Protect core family wealth transfer mechanisms

- Monitor real-world behavioral responses carefully

As we move forward, keeping these principles in mind could lead to smarter, less disruptive solutions.

Wrapping Up: A Moment for Reflection

This proposal to dramatically lower estate tax protections and raise rates isn’t just another line item in a budget memo. It strikes at the heart of what many work so hard to achieve: the ability to build something lasting for their children and grandchildren.

Whether you see it as necessary tough medicine or an overreach that could backfire, one thing is clear—the conversation about how we fund our cities matters deeply. It affects where people live, how they plan their finances, and ultimately the kind of opportunities available to future generations.

I’ll be keeping an eye on how these ideas progress through the process. In the meantime, it might be worth having your own family discussions about legacy planning. Because in uncertain fiscal times, being proactive can make all the difference.

What are your thoughts on where the line should be drawn between public needs and private inheritance? These are the kinds of questions that define not just budgets, but the character of a place.

(Word count: approximately 3,450. The piece draws on publicly discussed policy ideas and aims to provide balanced context for readers navigating complex financial landscapes.)