Have you ever wondered why some investors seem to squeeze more out of the same manager and similar strategies? Lately, a clear pattern has emerged in the world of collective investments. Many are discovering that one structure consistently edges ahead in returns, even when the person calling the shots is identical.

It’s not magic or insider secrets. It comes down to how the vehicle is built. In turbulent times marked by inflation spikes and market swings, that structural difference can translate into meaningful extra pounds in your pocket over the years. But before you rush to switch everything, it’s worth digging deeper into what’s really driving those numbers and whether they suit your own situation.

Why the Structure Matters More Than You Might Think

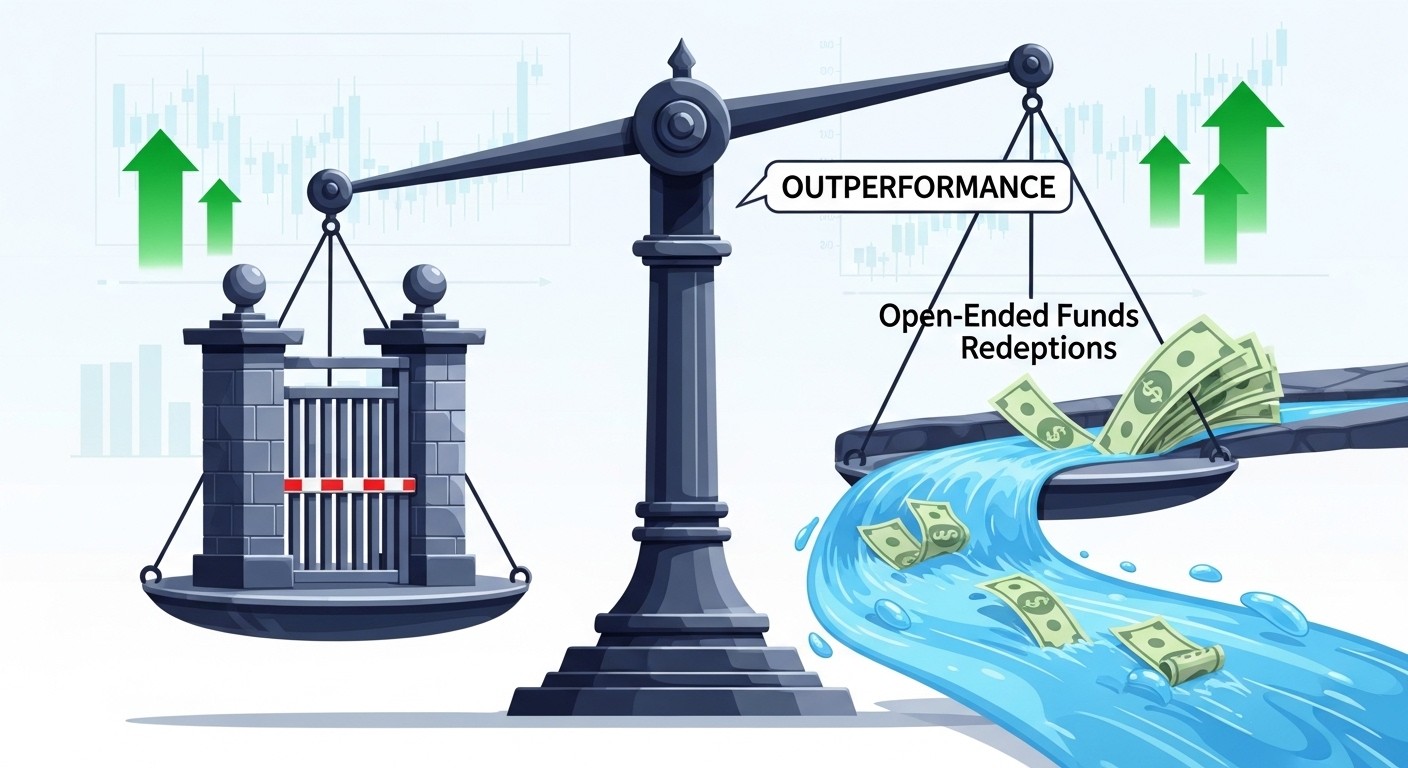

Let’s start with a simple truth I’ve noticed after following markets for years: the wrapper around your investment can influence outcomes as much as the assets inside it. Investment trusts operate as closed-ended vehicles. Once the initial pool of capital is raised through shares listed on the stock exchange, the number of shares stays fixed. Managers aren’t constantly dealing with money flowing in and out as new investors join or others cash out.

Open-ended funds, on the other hand, expand or shrink daily based on investor demand. That flexibility sounds convenient until markets turn choppy. Suddenly, a flood of redemption requests can force the manager to sell holdings, sometimes at the worst possible moment. I’ve seen this dynamic play out in past downturns, and it rarely ends well for remaining investors.

Recent figures highlight just how significant this difference can be. Across numerous matched pairs where the same team runs both a trust and a corresponding open-ended fund, the closed-ended version came out ahead in the vast majority of cases over longer horizons. Specifically, around 77 percent of investment trusts outperformed their sister funds when looking back a full decade. That’s not a small edge.

The closed-ended structure lets managers buy and sell when it makes strategic sense rather than when investors demand their money back.

– Industry research observation

This freedom opens doors to opportunities that might otherwise stay closed. Think about smaller companies or even stakes in private businesses. These assets often lack the daily liquidity that open-ended funds require to handle redemptions smoothly. A trust can hold them patiently, waiting for the right exit without panic selling.

Quantifying the Outperformance Edge

Numbers tell a compelling story, but context makes them meaningful. Over the past ten years, the typical investment trust in these matched pairs generated an additional £31 for every £100 invested compared with its open-ended counterpart. That compounds nicely over time.

Breaking it down further, the average annual outperformance sat around 1.3 percentage points. Not earth-shattering on its own, but consistent enough to make a real difference in retirement pots or long-term wealth building. Shorter periods show even stronger relative results in some cases. One-year data pointed to an extra £5 per £100, while three years delivered roughly £6 more.

| Time Period | Outperformance Rate | Extra Return per £100 | Avg Annual Edge |

| 1 Year | 82% | £5 | 4.5% |

| 3 Years | 72% | £6 | 1.8% |

| 5 Years | 53% | £3 | 0.5% |

| 10 Years | 77% | £31 | 1.3% |

Notice how the five-year figure looks more modest. Part of that comes down to how market sentiment affects pricing. When investor confidence dips, trusts can trade at wider discounts to their underlying net asset value. That gap widened noticeably from earlier levels around 4 percent to something closer to 14 percent in recent periods. Discounts act like a headwind in the short run but can flip into a tailwind when sentiment improves and they narrow again.

In my experience, these valuation swings separate patient investors from the rest. If you can look past temporary noise and focus on the underlying portfolio performance, the structural benefits tend to shine through over full market cycles.

The Power of Gearing and Long-Term Thinking

Another tool in the investment trust toolkit is gearing – essentially borrowing money to invest more than the actual shareholder capital. Open-ended funds generally can’t do this to the same degree because of regulatory constraints tied to daily liquidity needs. When used wisely, gearing amplifies positive returns. Of course, it also magnifies losses during tough times, so it’s not something to take lightly.

Managers of trusts often employ modest levels of gearing strategically, perhaps increasing exposure when they see undervalued opportunities. This ability to take a longer view without daily cash flow pressures allows for more conviction in stock picking or sector allocations. I’ve always found it fascinating how the same team can deliver noticeably different results simply because one vehicle gives them more breathing room.

Investment trusts won’t beat open-ended funds every single year, especially in sharp downturns when discounts can widen dramatically. Yet over complete market cycles, those structural edges frequently support stronger compounded performance.

Beyond gearing, the closed structure encourages holding less liquid but potentially higher-reward assets. Smaller companies, niche sectors, or even venture-style opportunities become more feasible. Open-ended funds must keep enough cash or easily sellable holdings ready for redemptions, which can dilute returns in rising markets.

Discounts and Premiums: The Double-Edged Sword

Here’s where things get interesting – and sometimes frustrating. Because investment trusts trade like regular shares on the stock market, their price can diverge from the value of the assets they hold. When trading at a discount, you’re essentially buying the underlying portfolio for less than it’s worth. Narrowing of that discount later can boost your total return beyond what the assets themselves deliver.

The flip side? Discounts can widen unexpectedly, especially during periods of market stress or when sentiment toward a particular sector sours. That’s one reason why shorter-term performance comparisons sometimes look less impressive. Investors who buy at wide discounts and hold through volatility often fare best, but it requires nerves of steel and a clear time horizon.

Premiums are rarer but do occur in popular trusts. Buying at a premium means paying more than the net asset value, which can erode returns if the premium shrinks. Savvy investors track these metrics closely rather than chasing recent performance blindly.

- Monitor average discount levels over time for your chosen trust

- Consider historical ranges before committing capital

- Factor potential narrowing or widening into your return expectations

- Remember that discounts don’t affect the underlying manager’s stock selection skill

Costs, Fees, and Other Practical Considerations

Performance isn’t the only factor. Fees matter, and they can vary between the two structures. Investment trusts often have slightly different cost profiles, partly because they’re listed and involve stockbroking charges. However, for larger portfolios or buy-and-hold strategies, the overall expense can sometimes work out lower than repeated dealing in open-ended funds.

Stamp duty applies when buying shares in investment trusts, adding a small upfront cost that open-ended funds avoid. On the other hand, platform fees or regular savings plans might make open-ended options more convenient for monthly investors who prefer pound-cost averaging without worrying about share prices.

Dividend handling differs too. Trusts can retain earnings in good years to smooth payouts later, offering more predictable income streams in some cases. Open-ended funds typically distribute what they receive, which can lead to more variable payments depending on market conditions.

When Open-Ended Funds Might Still Make Sense

It would be unfair to paint investment trusts as universally superior. In highly liquid global equity markets, low-cost passive open-ended funds or ETFs can deliver efficient exposure without the complications of discounts or gearing. For investors who prioritize simplicity and don’t want to monitor share prices daily, the open-ended route often feels more straightforward.

Specialist areas like UK smaller companies have historically shown stronger trust outperformance, while broad global mandates sometimes favor the flexibility and lower costs of open structures. There’s no shame in blending both approaches. Many successful portfolios use trusts for niche or illiquid exposures and open-ended vehicles for core, liquid holdings.

Perhaps the most important question is your own risk tolerance and time horizon. If you’re comfortable with extra volatility from gearing and discount movements, trusts can reward patience. If you prefer predictability and ease, open-ended funds might align better with your style.

The closed-ended structure can be incredibly powerful because managers aren’t forced to sell assets during stressful periods to meet redemptions.

Real-World Implications for Different Investor Types

Let’s bring this down to earth with some practical scenarios. A young professional starting a long-term ISA might benefit from the growth potential of geared trusts focused on smaller companies or emerging themes. The ability to invest with conviction without daily liquidity worries could compound nicely over decades.

Retirees seeking steady income might appreciate certain income-focused trusts that can smooth dividends by holding back earnings in bumper years. However, they’d need to accept the possibility of capital volatility from discount swings. Balancing that with more stable open-ended bond or multi-asset funds could create a smoother overall experience.

For those building wealth through regular monthly contributions, open-ended funds often win on convenience. Setting up direct debits is simple, and there’s no need to worry about bid-offer spreads or timing purchases around market hours. Yet even here, a portion allocated to quality trusts could enhance long-term results.

- Assess your investment time horizon – longer favors trusts

- Evaluate comfort with additional volatility from gearing

- Review current discount or premium levels carefully

- Consider how the holding fits within your overall asset allocation

- Factor in personal tax wrappers like ISAs where stamp duty might not apply

Risks That Deserve Honest Attention

No investment discussion is complete without acknowledging downsides. Gearing works both ways. In falling markets, it can accelerate losses and increase stress levels. Discounts can persist or widen for extended periods, testing even the most disciplined investor’s resolve.

Liquidity in the trust’s own shares can sometimes be lower than in popular open-ended funds, although major trusts usually trade with reasonable volume. Management fees and other costs still apply, so it’s essential to compare total expense ratios apples-to-apples.

Market cycles also play a role. During prolonged bull runs driven by mega-cap stocks, simpler passive open-ended funds can look very attractive. Trusts that take active bets or hold more diverse, smaller positions might lag temporarily. The key is understanding these dynamics rather than chasing last year’s winner.

Building a Balanced Approach

Rather than viewing this as an either-or decision, many experienced investors treat trusts and open-ended funds as complementary tools. Use trusts where their structural advantages shine brightest – illiquid or specialist areas, income smoothing, or when attractive discounts appear. Rely on open-ended vehicles for core diversified exposure or when simplicity is paramount.

Diversification across structures can itself reduce some risks. If discounts widen across the trust universe during a correction, your open-ended holdings might provide more stability. Conversely, when sentiment recovers and discounts narrow, trusts could deliver an extra boost.

I’ve come to believe that the best portfolios reflect the investor’s personality as much as market conditions. Some people thrive on analyzing discount trends and manager conviction levels. Others prefer set-it-and-forget-it simplicity. Neither approach is inherently wrong if it matches your goals and sleep-at-night factor.

Looking Ahead: What Might Change the Landscape

Regulatory environments evolve, and investor preferences shift. Greater awareness of trust advantages could narrow persistent discounts over time as more capital flows in. Technological improvements in trading and information access might reduce some of the perceived complexity around listed vehicles.

Meanwhile, the growth of private markets and alternative assets continues. Trusts are often better positioned to participate meaningfully in these areas without liquidity mismatches. That could widen the performance gap further in certain segments.

Inflation and interest rate cycles will keep testing both structures differently. Open-ended funds might face more redemption pressure during rate hikes, while trusts can maintain strategic allocations more steadily. No one can predict exact future performance, but understanding the mechanics helps tilt probabilities in your favor.

Practical Steps to Get Started

If you’re intrigued by the potential of investment trusts, start small. Research a few sectors where trusts have historically shown strong relative performance, such as specialist equity areas. Compare several options with similar mandates to understand discount history and gearing policies.

Consider speaking with a financial adviser who understands both structures deeply. They can help model how different allocations might behave across various market scenarios. Remember that past outperformance doesn’t guarantee future results, especially when economic conditions change.

- Review your current portfolio for any obvious gaps that trusts could fill

- Analyze at least five years of discount and performance data

- Stress test potential holdings against different economic backdrops

- Ensure overall portfolio risk level remains comfortable

- Rebalance periodically as discounts and market conditions evolve

Ultimately, the choice between investment trusts and open-ended funds comes down to aligning structure with strategy. The data suggests closed-ended vehicles have delivered meaningful advantages for many investors willing to embrace their unique characteristics. Yet success still hinges on selecting skilled managers, maintaining appropriate diversification, and staying disciplined through market ups and downs.

Markets will always surprise us, but understanding these fundamental differences gives you a clearer framework for decisions. Whether you lean toward trusts, prefer open-ended simplicity, or mix both, the goal remains the same: building wealth thoughtfully over time while managing risks that match your personal circumstances. The extra returns from structural edges can be rewarding, but only if they fit comfortably within your broader financial plan.

In the end, there’s no universal “best” choice. What matters most is making informed selections that reflect both the opportunities and the realities of each investment wrapper. With patience and a clear-eyed view of both the benefits and the trade-offs, many investors have found that including investment trusts has enhanced their overall results without taking on unacceptable extra risk.

The conversation around these vehicles continues to evolve as more data accumulates and market conditions shift. Staying curious and periodically reviewing your approach can help ensure your portfolio remains well-positioned for whatever comes next. After all, successful investing is less about finding perfect solutions and more about making consistently good choices over many years.