Have you ever wondered what happens when Wall Street’s biggest players decide to bridge traditional finance with cutting-edge blockchain technology? The recent collaboration between JPMorgan, Mastercard, and Ripple offers a fascinating glimpse into that very future. In a groundbreaking pilot, these financial giants successfully tested the redemption of tokenized U.S. Treasury funds using the XRP Ledger while integrating smoothly with conventional banking rails. It’s the kind of development that makes you sit up and pay attention to where money movement is headed.

This isn’t just another blockchain experiment. It represents a tangible step toward making high-value financial transactions faster, more efficient, and accessible across borders. As someone who’s followed the evolution of digital assets for years, I find this particular test particularly compelling because it demonstrates practical utility rather than hype. The implications stretch far beyond crypto enthusiasts into the daily operations of global institutions.

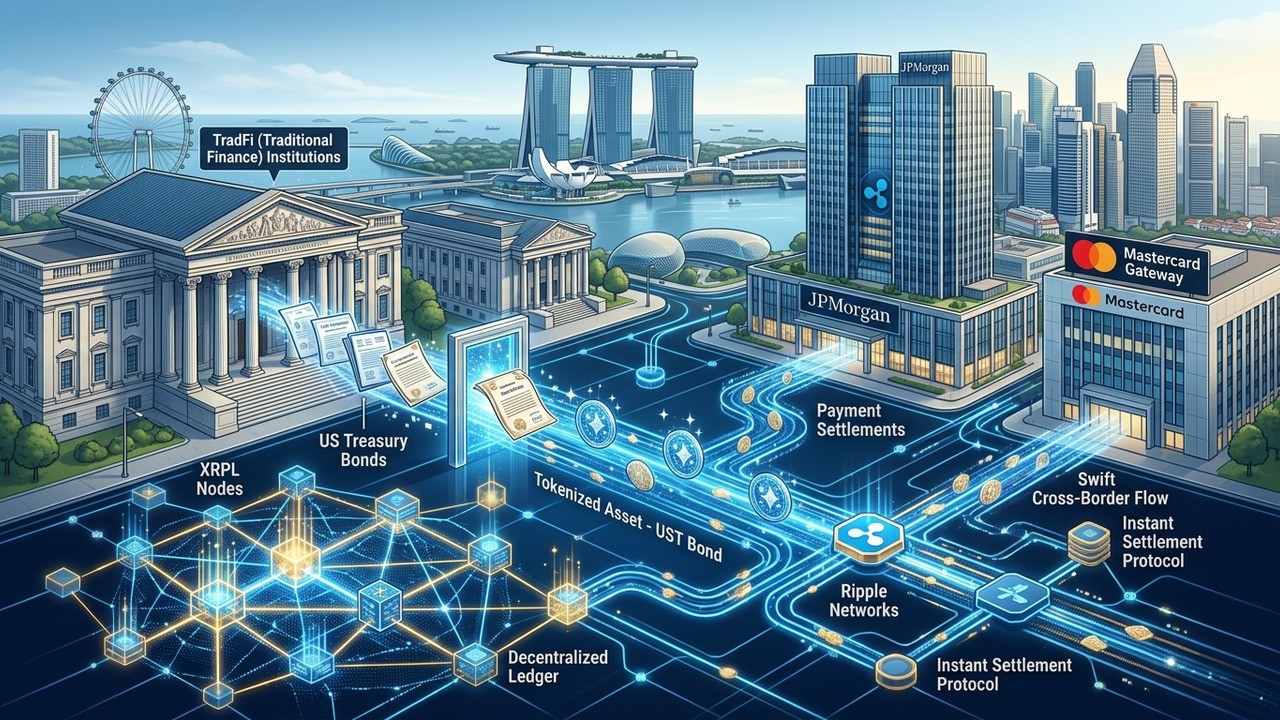

A New Era for Tokenized Assets in Traditional Finance

The pilot centered around Ondo Finance’s OUSG fund, which represents tokenized short-term U.S. government Treasuries. Ripple redeemed a portion of its holdings directly on the XRP Ledger. Meanwhile, Mastercard’s Multi-Token Network handled settlement instructions that flowed to Kinexys by J.P. Morgan. The fiat side of the transaction then moved through JPMorgan’s correspondent banking network, ultimately landing in Ripple’s Singapore bank account.

What makes this transaction stand out is the speed and seamlessness. The asset leg processed on the blockchain in under five seconds. That’s remarkably fast compared to traditional settlement processes that often involve delays, manual interventions, and strict banking hours. In my view, this kind of efficiency could eventually transform how institutions manage liquidity and cross-border operations.

Understanding the Technical Flow

Let’s break down what actually happened in this test. On one side, we have the public blockchain handling the digital asset representation. On the other, established banking infrastructure managed the fiat currency movement. This hybrid approach seems to be the sweet spot that many institutions are exploring right now.

Ripple’s redemption of OUSG on XRPL triggered corresponding instructions through Mastercard’s network. These instructions reached JPMorgan’s Kinexys platform, which then executed the dollar transfer through traditional channels. The entire process bridged two worlds that historically operated separately. The result? Near real-time settlement outside conventional banking windows.

This milestone represents the first time tokenized U.S. Treasuries have settled across borders and banks in near real time and outside traditional banking windows.

– Industry participant involved in the pilot

Such statements highlight the significance. For years, tokenized assets remained mostly conceptual or confined to limited testing environments. This pilot shows they’re ready for more serious applications. The involvement of household names like JPMorgan and Mastercard adds substantial credibility to the entire ecosystem.

Why Tokenized Treasuries Matter Right Now

Tokenized U.S. Treasuries have emerged as one of the largest segments within real-world asset tokenization. Their appeal is straightforward: they combine the stability and yield of government securities with the programmability and efficiency of blockchain technology. Investors get exposure to trusted assets while benefiting from faster transfers and reduced intermediaries.

In uncertain economic times, having quick access to liquid, yield-bearing assets becomes particularly valuable. Institutions can potentially manage cash positions more dynamically. Imagine settling international payments or managing treasury operations with the speed of digital assets but backed by the full faith of U.S. government securities. That’s the promise beginning to materialize.

- Enhanced liquidity through faster settlement cycles

- Reduced counterparty risk via transparent on-chain records

- 24/7 operational capability beyond banking hours

- Improved capital efficiency for participating institutions

- Potential for new financial products and use cases

These benefits aren’t theoretical. The pilot demonstrated several of them in action. The cross-border element particularly stands out because international transfers have long been plagued by delays, high costs, and opacity. Connecting blockchain rails with traditional banking could address many of these longstanding pain points.

The Role of XRPL in Institutional Adoption

The XRP Ledger brings specific advantages to this type of use case. Its design focuses on speed, scalability, and reliability for value transfer. These characteristics make it well-suited for handling tokenized securities that require quick confirmation and settlement. The public nature of the ledger also provides transparency that regulated institutions increasingly demand.

Unlike some newer blockchain networks, XRPL has years of operational history. This track record matters when dealing with significant financial value. Institutions need systems they can trust not just for functionality but for consistent performance under real-world conditions. The successful redemption in this pilot suggests XRPL is meeting those expectations.

I’ve observed over time that enterprise blockchain adoption often favors networks with proven enterprise features. The integration with existing financial infrastructure demonstrated here aligns with what many large organizations actually need — evolution rather than complete replacement of their current systems.

Broader Implications for Real World Asset Tokenization

This pilot doesn’t exist in isolation. It fits into a larger trend of financial institutions exploring tokenization across various asset classes. From real estate to bonds and equities, the movement toward digital representation of real-world value continues gaining momentum. Treasuries serve as a natural starting point because of their relative simplicity and high demand.

The total value locked in tokenized real-world assets has grown substantially. While exact figures fluctuate, the sector clearly represents billions in distributed value. This growth reflects genuine institutional interest rather than speculative retail activity. When major banks participate actively, it signals a maturing market.

The transaction shows how tokenized assets can connect with banking systems without replacing them.

That balanced approach seems key to wider acceptance. Complete disruption would face too much resistance. Instead, these hybrid models allow gradual integration. One part of the transaction happens on-chain while the fiat elements use familiar rails. Over time, more components might migrate to blockchain, but the transition feels measured and practical.

Challenges and Regulatory Considerations

Despite the exciting progress, significant hurdles remain. Regulatory clarity stands out as perhaps the most important factor for scaling these solutions globally. Different jurisdictions approach digital assets differently, creating complexity for cross-border applications.

Settlement finality, legal recognition of on-chain transactions, and risk management protocols all need careful attention. International coordination becomes crucial when transactions span multiple countries and regulatory regimes. The pilot successfully navigated these waters in a controlled environment, but widespread adoption requires more comprehensive frameworks.

Industry observers note that clearer rules could unlock substantially more capital. Until then, many institutions remain in observation or limited testing mode. The success of this JPMorgan-Mastercard-Ripple collaboration provides valuable data points for policymakers and regulators evaluating appropriate guardrails.

How This Affects Different Market Participants

For traditional banks, this pilot demonstrates ways to leverage blockchain without abandoning core infrastructure. They can enhance service offerings while maintaining compliance and risk controls developed over decades. The ability to offer clients faster settlement or new treasury management tools creates competitive advantages.

Asset managers and funds gain new tools for efficiency. Tokenized products can potentially lower operational costs and improve investor experiences through faster redemptions and more transparent holdings. The yield component of Treasury products makes them particularly attractive in portfolios seeking stability with digital efficiency.

Technology providers and blockchain networks benefit from proven use cases. Successful pilots attract more developers, users, and institutional partners. This creates positive feedback loops that accelerate innovation across the ecosystem.

- Institutions test specific use cases in controlled environments

- Successful outcomes build confidence and attract more participants

- Increased participation drives further technical improvements

- Regulatory frameworks evolve based on real-world evidence

- Broader adoption leads to new financial products and services

The Singapore Connection and Global Reach

The choice of Singapore for Ripple’s bank account in this test carries significance. The city-state has positioned itself as a forward-thinking financial hub with supportive policies for digital assets. Its regulatory environment encourages innovation while maintaining stability — qualities that make it attractive for such experiments.

Cross-border elements highlight how tokenized assets could reshape international finance. Traditional correspondent banking involves multiple intermediaries, time zones, and potential delays. Blockchain connections promise to streamline these processes significantly. The near real-time aspect opens possibilities for more responsive global treasury operations.

Companies operating across multiple jurisdictions might eventually manage cash positions more effectively. Liquidity can move where needed faster, potentially reducing the amount of idle capital held in various locations. For multinational corporations, these efficiency gains could translate into meaningful cost savings and improved financial agility.

Comparing Traditional vs Tokenized Settlement

| Aspect | Traditional Settlement | Tokenized Approach |

| Speed | Days or business hours | Near real-time (seconds) |

| Availability | Banking hours only | 24/7 potential |

| Transparency | Limited visibility | On-chain auditability |

| Intermediaries | Multiple banks involved | Reduced through direct connections |

| Cost Structure | Higher fees for cross-border | Potential for lower operational costs |

This comparison illustrates why so many players show interest. The tokenized path doesn’t win in every category yet, but the advantages in speed and availability address real business needs. As technology matures and integration deepens, the gap in other areas may narrow further.

Future Possibilities and Industry Momentum

Looking ahead, this pilot points toward several exciting developments. We might see expanded use of tokenized Treasuries for collateral, liquidity management, or even as settlement assets in other blockchain applications. The programmability of tokens opens creative structuring opportunities that traditional securities struggle to match.

Other financial market infrastructures are also advancing tokenization initiatives. Major clearing houses and exchanges explore similar technologies, suggesting the industry is moving systematically toward digital asset integration. The involvement of diverse players — banks, payment networks, blockchain firms, and asset managers — creates a rich environment for innovation.

Perhaps most importantly, these tests generate practical learnings about what works and what needs refinement. Each successful pilot reduces uncertainty and builds the knowledge base necessary for larger deployments. The path from experiment to production becomes clearer with every transaction completed.

Risk Management in the New Paradigm

Any discussion of tokenized assets must address risk considerations. While blockchain offers transparency and immutability benefits, it also introduces new technical and operational risks. Smart contract vulnerabilities, oracle dependencies, and bridge security all require careful attention in hybrid systems.

Institutions participating in these pilots typically implement multiple layers of controls. They maintain traditional risk frameworks while adding blockchain-specific monitoring. This combined approach helps ensure that innovation doesn’t come at the expense of stability — a crucial balance for systemic financial infrastructure.

Regulatory bodies worldwide watch these developments closely. Their guidance will shape how quickly and in what forms tokenization scales. The goal remains protecting market integrity and investors while allowing beneficial innovation to flourish. Getting this balance right could determine the pace of adoption for years to come.

What This Means for Individual Investors and Smaller Players

While this pilot involves large institutions, the effects may eventually reach retail and smaller professional investors. More efficient markets and new product structures could create opportunities for broader participation in previously inaccessible or inefficient asset classes.

Tokenization potentially lowers barriers through fractional ownership and improved liquidity. However, these benefits will likely emerge gradually as infrastructure develops and regulations evolve. Early signals from institutional activity often precede wider availability, giving attentive observers time to prepare.

In my experience following financial innovation, the most sustainable advances combine institutional backing with genuine utility. This tokenized Treasury pilot appears to check both boxes. It solves real problems while leveraging trusted counterparties and established assets.

The collaboration between JPMorgan, Mastercard, and Ripple marks more than a single successful test. It exemplifies the maturing relationship between traditional finance and blockchain technology. As these experiments continue and expand, we edge closer to a financial system that combines the best of both worlds — stability and innovation, trust and efficiency.

The road ahead contains challenges, but the direction seems clear. Tokenized assets, particularly Treasuries, will likely play an increasingly important role in global finance. How quickly and comprehensively this transformation occurs depends on continued technical progress, thoughtful regulation, and sustained collaboration across the industry.

For now, this pilot stands as encouraging proof that practical integration is not only possible but already happening. The financial landscape is evolving, and developments like this remind us that the future of money is being built through careful, deliberate steps by major market participants working together.

As more institutions gain comfort with these hybrid models, we can expect to see expanded use cases, improved technology, and eventually broader accessibility. The tokenized Treasury settlement on XRPL represents one significant milestone on a longer journey toward more efficient, inclusive, and responsive financial systems worldwide.

The excitement lies not just in what was achieved in this specific transaction, but in what it enables for the future. Faster, more transparent, and more connected financial markets could benefit businesses, governments, and individuals alike. We’re witnessing the early chapters of what might become a fundamental reshaping of how value moves around the globe.