Have you ever wondered what happens when one of the world’s most critical energy chokepoints suddenly shuts down? The ongoing conflict involving Iran has done exactly that, and the ripple effects are already reshaping how nations and industries think about their energy future. As someone who’s followed these markets for years, I find the responses from top oil executives particularly telling—they’re not just reacting to short-term chaos but outlining fundamental, long-lasting transformations.

The closure of the Strait of Hormuz has removed vast quantities of crude from circulation, creating shortages that grow more severe with each passing day. This isn’t some abstract geopolitical event. It’s hitting wallets, supply chains, and strategic planning rooms across the globe right now. What struck me most while reviewing recent earnings discussions is how leaders in the sector see this as a catalyst for deeper change rather than just another crisis to weather.

The Wake-Up Call for Energy Security

Governments worldwide are suddenly treating energy security as far more than a buzzword. It’s become a top priority that influences policy at the highest levels. When key shipping routes can be blocked, the vulnerability of relying too heavily on specific regions becomes painfully obvious. Executives from major oilfield services companies have emphasized this shift repeatedly in recent weeks.

One CEO described the situation as driving fundamental structural change across the entire energy landscape. It’s no longer sufficient to have abundant supply somewhere in the world if it can’t reliably reach consumers. This new reality is pushing countries to build more resilient systems with built-in redundancies.

It’s going to drive fundamental structural change across the energy landscape.

– Oilfield services CEO

In my view, this represents one of those rare moments where a crisis forces long-overdue conversations. Nations dependent on Middle Eastern supplies are now urgently reassessing their exposure. The days of assuming smooth sailing for tankers through critical passages may be over for the foreseeable future.

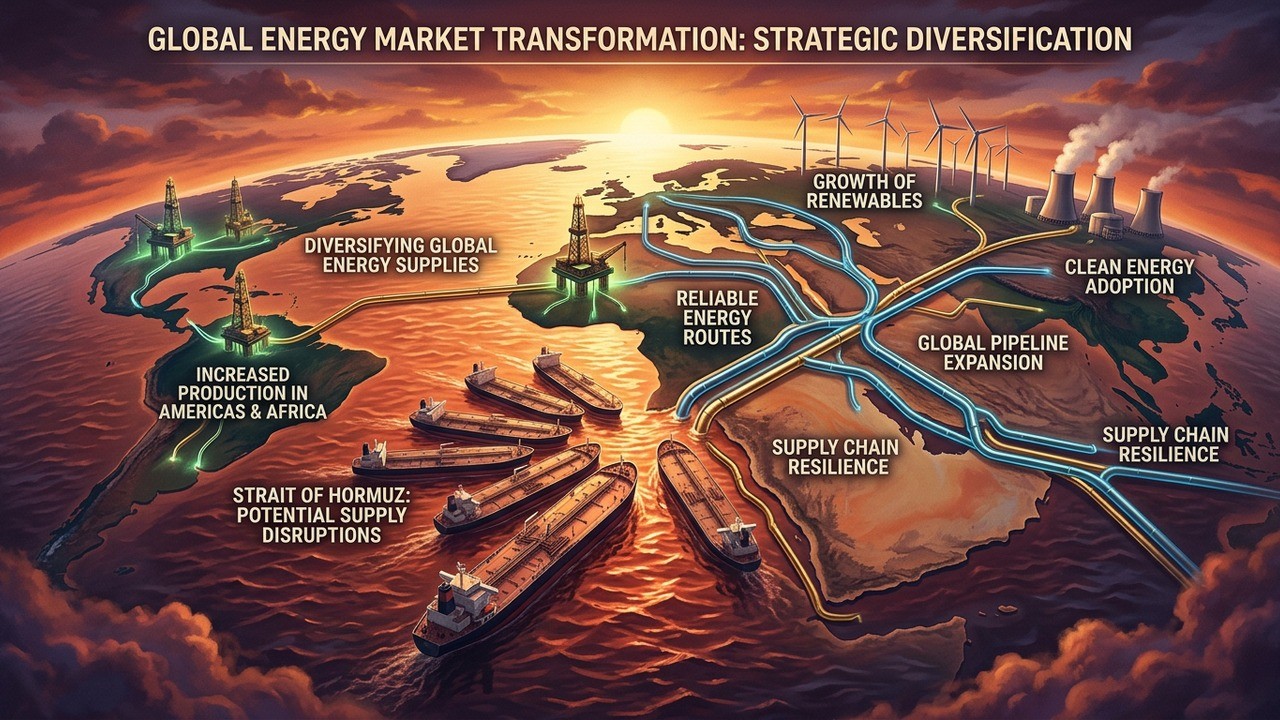

Diversifying Supply Sources Becomes Essential

Perhaps the most immediate response involves diversifying where energy comes from. Asian economies, in particular, have traditionally leaned heavily on Middle Eastern crude and liquefied natural gas. That dependence is now under scrutiny like never before. Companies and governments alike are looking for ways to spread their risks more evenly.

This doesn’t mean completely abandoning traditional suppliers, but rather building additional streams that can act as buffers during disruptions. U.S. crude, for instance, has gained even more prominence as a reliable alternative during this period. Exports from American producers have reached new heights, highlighting the country’s growing role in stabilizing global supplies.

- Rebuilding strategic stockpiles to levels above historical averages

- Developing new trade partnerships across different regions

- Investing in infrastructure that supports multiple supply routes

- Encouraging domestic production where geologically feasible

The market has shifted dramatically from expectations of potential surpluses to concerns about significant deficits. This tightness supports the case for sustained higher prices even after the immediate conflict resolves. Higher prices, while challenging for consumers, create the economic incentives needed for fresh investments in production capacity.

Investment Surge Expected in Oil and Gas Exploration

Don’t expect investment in traditional oil and gas to dry up anytime soon. Quite the opposite, actually. The current disruptions are likely to encourage more capital flowing into exploration and production activities. Offshore and deepwater projects, in particular, stand to benefit as companies seek resources outside politically volatile regions.

Africa emerges as one especially promising area according to industry leaders. With its substantial underdeveloped resources, the continent could see increased attention and portfolio allocations in the coming years. Similar opportunities exist in parts of the Americas and Asia where geological potential meets improving investment climates.

Africa represents one of the most compelling long-term opportunities, with a significant base of underdeveloped oil and gas resources.

– SLB CEO

What I find interesting is how this renewed focus on conventional resources doesn’t necessarily come at the expense of other energy forms. Instead, it seems to reflect a more pragmatic, all-of-the-above approach to meeting demand while managing risks. The fragility exposed by recent events makes a compelling case for having multiple pillars supporting the global energy system.

The Continued Role of Low Carbon Solutions

Interestingly, the push for energy security hasn’t sidelined investments in lower carbon alternatives. Executives highlighted ongoing commitments to technologies like geothermal, nuclear power, and grid modernization. These aren’t competing with oil and gas in this new environment but rather complementing them as part of a more robust overall infrastructure.

The goal extends beyond simply increasing total supply. It’s about creating systems with greater redundancy and resilience. Diversifying not just geographically but also technologically helps reduce dependence on any single type of asset or route. This balanced perspective acknowledges both immediate needs and longer-term environmental considerations.

Grid modernization, for example, allows for better integration of various generation sources while improving reliability during periods of stress. Nuclear and geothermal provide stable baseload power that can help offset some of the variability inherent in other renewables. The current crisis seems to be reinforcing the wisdom of maintaining a diverse energy mix.

Impact on Oil Prices and Market Dynamics

The supply disruptions have fundamentally altered near-term market expectations. What was anticipated as a potential surplus environment has transformed into one facing notable deficits. This shift naturally puts upward pressure on prices, creating a more supportive backdrop for producers once stability returns.

Elevated prices following resolution of the conflict would likely sustain investment momentum. Companies that have been cautious about committing capital in recent years may find renewed justification for expanding operations. This cycle of disruption leading to higher prices leading to more supply is a familiar pattern in energy markets, though the scale here feels particularly significant.

| Factor | Pre-Conflict Outlook | Current Reality |

| Global Supply Balance | Potential Surplus | Significant Deficit |

| Strategic Stockpiles | Stable | Depleted, Need Rebuilding |

| Investment Appetite | Cautious | Increasing Focus |

| Regional Importance | Middle East Dominant | Diversification Priority |

Beyond the immediate price effects, the conflict is accelerating certain trends that were already underway. The importance of U.S. shale production, for instance, has been magnified. American operators have demonstrated their ability to respond to global needs, strengthening the case for policies that support domestic energy development.

Geopolitical Lessons and Strategic Realignments

One of the subtler but important outcomes involves how nations view their alliances and dependencies. Energy has always been intertwined with geopolitics, but events like the Hormuz blockade bring these connections into sharper focus. Countries are likely to pursue more active diplomatic efforts aimed at securing reliable supply agreements.

This could manifest in everything from new trade pacts to joint infrastructure projects designed to bypass vulnerable routes. For companies, it means carefully evaluating political risks when planning long-term investments. The executives I’ve referenced seem acutely aware of these dynamics and are positioning their organizations accordingly.

I’ve always believed that true energy security requires thinking several moves ahead. The current situation validates that approach. Rather than simply replacing one supplier with another, the smarter path involves creating networks of options that can adapt to changing circumstances. This resilience doesn’t come cheap or easy, but the alternative—repeated vulnerability—proves far costlier.

Opportunities in Offshore and Deepwater Development

With renewed emphasis on supply diversity, offshore opportunities are attracting fresh interest. These projects often require substantial upfront investment and technical expertise, but they can deliver significant volumes from areas less prone to certain types of disruption. Industry leaders specifically mentioned prospects in Africa, the Americas, and parts of Asia.

Deepwater capabilities have advanced considerably in recent decades, making previously marginal fields more economically viable. As prices find support at higher levels, the threshold for approving these capital-intensive projects becomes easier to clear. This could lead to a meaningful uptick in offshore activity over the next few years.

- Technological improvements reducing operational costs

- Higher price environment improving project economics

- Strategic need for non-traditional supply sources

- Partnerships between international companies and local governments

The offshore sector also tends to benefit from the specialized expertise of companies like those whose executives have been vocal lately. Their services—from seismic analysis to drilling operations—become even more valuable as activity ramps up in challenging environments.

Rebuilding Inventories and Managing Volatility

One direct consequence of the supply squeeze has been the drawdown of global inventories. Replenishing these buffers will require sustained production above demand levels for some time. This process won’t happen overnight and will influence market balances well into the future.

Executives anticipate inventories being rebuilt to levels that provide greater comfort during future crises. This represents both a challenge and an opportunity for producers who can reliably deliver volumes. The focus on security means buyers may be willing to pay premiums for contracts that guarantee delivery even under stressed conditions.

Volatility itself may become a more permanent feature as the world adjusts to these new realities. Markets have always had their ups and downs, but the added layer of geopolitical risk from key regions could amplify those swings. Companies with strong balance sheets and flexible operations will likely navigate this environment more successfully.

Broader Implications for Energy Transition Efforts

While the immediate focus remains on securing adequate supplies of traditional fuels, the conversation around energy transition continues. The difference now is that security and resilience are weighted more heavily alongside emissions reduction goals. This more nuanced approach may actually accelerate certain aspects of the transition by highlighting the need for diverse, reliable clean energy sources.

Nuclear power, for example, offers steady output independent of weather conditions or shipping routes. Geothermal provides similar baseload characteristics with minimal environmental footprint in suitable locations. Investments in these areas complement rather than replace oil and gas development in the current environment.

It’s not just about increasing energy supply. It’s about the robust and resilient energy infrastructure and greater redundancy.

– Baker Hughes CEO

The grid itself needs strengthening to handle both traditional and renewable inputs more effectively. Modernization efforts that were already planned may now receive additional urgency and funding. In this sense, the crisis could ultimately support a more balanced and practical path forward for global energy systems.

What This Means for Investors and Businesses

For investors, the evolving situation creates both risks and opportunities. Companies positioned in U.S. shale, offshore services, or inventory management solutions may see increased demand for their capabilities. Conversely, those overly exposed to disrupted regions face greater challenges.

Businesses across sectors should consider how energy price volatility and potential supply issues might affect their operations. Manufacturers, transportation companies, and even data centers all depend on reliable, affordable energy. Proactive planning and hedging strategies become more important than ever.

From my perspective, the most successful players will be those who balance short-term responses with long-term strategic thinking. The energy world is changing, and adaptability will be key. This includes embracing new technologies while maintaining core competencies in resource extraction and delivery.

Looking Ahead: A More Resilient Energy Future?

As the situation continues to unfold, several key themes stand out. First, the importance of diversification cannot be overstated—whether in geographic sources, technological approaches, or infrastructure routes. Second, investment in production capacity remains crucial even as cleaner alternatives advance. Third, resilience and redundancy are moving from desirable to essential characteristics of energy systems.

The executives who’ve shared their insights recently paint a picture of an industry rising to meet extraordinary circumstances. Their focus on both immediate challenges and structural changes suggests confidence in the sector’s ability to adapt. While the human and economic costs of conflict are undeniably tragic, the forced reevaluation of energy strategies may yield positive outcomes in terms of long-term security.

Countries that act decisively to strengthen their energy independence and partnerships will be better positioned moving forward. Companies that innovate and invest thoughtfully should find opportunities amid the uncertainty. For all of us who depend on stable energy supplies—essentially everyone—these developments matter profoundly.

The coming months and years will test many of these predictions and strategies. Markets will fluctuate, policies will evolve, and new technologies may emerge. Yet the core lesson seems clear: energy security demands attention, investment, and international cooperation. Ignoring it is no longer an option, if it ever truly was.

In reflecting on these shifts, I’m reminded that energy has always been the lifeblood of modern economies. When that flow faces serious threats, the responses reveal both vulnerabilities and strengths in our global systems. The Iran conflict has exposed the former while encouraging development of the latter. How effectively we learn from this experience will shape energy markets—and by extension, global prosperity—for decades ahead.

The transformation won’t be simple or painless, but necessity has a way of driving progress. As oil leaders have indicated, we’re likely entering a period of more deliberate, security-conscious energy development. That could ultimately benefit consumers through more reliable supplies and businesses through clearer investment signals. Only time will tell exactly how it all unfolds, but the direction seems set.

This evolving story deserves close attention from anyone interested in global economics, investment opportunities, or simply understanding forces shaping our daily lives. The interplay between geopolitics and energy has rarely been more evident, and the stakes have seldom been higher. Staying informed and considering the broader implications will help navigate whatever comes next.