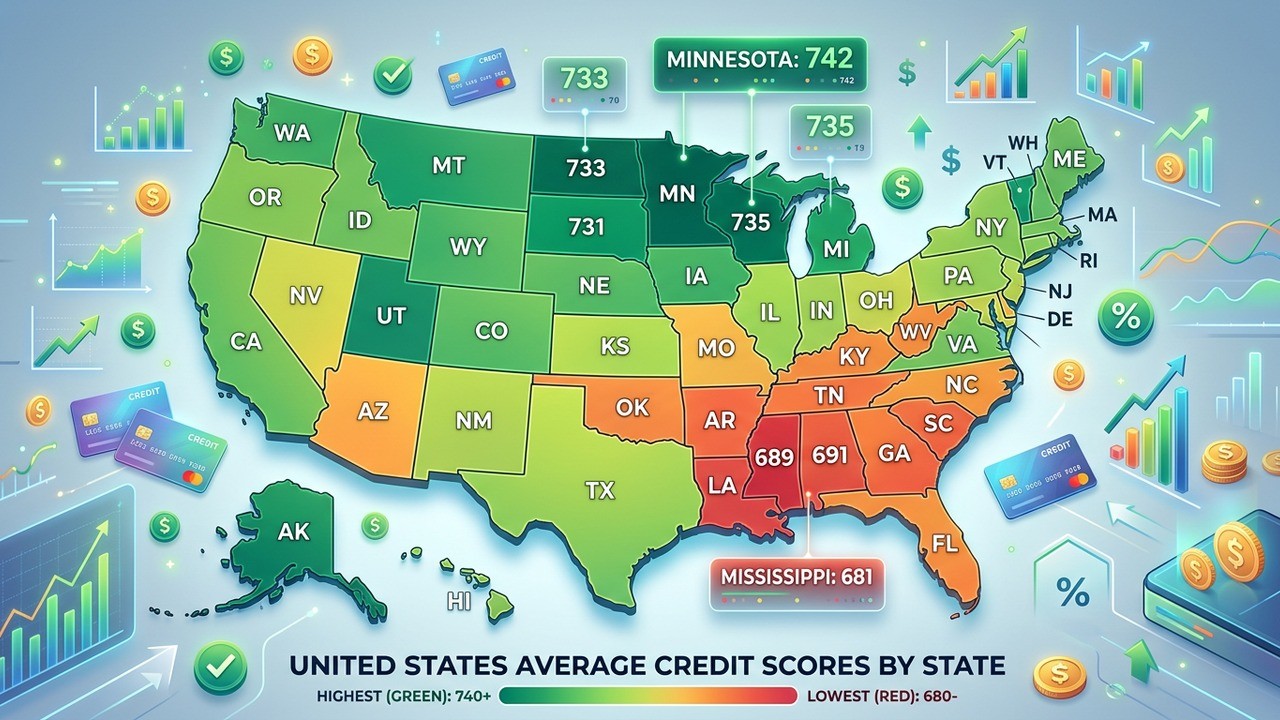

Have you ever wondered how your credit score stacks up against your neighbors across the country? The latest figures for 2026 paint a fascinating picture of America’s financial health, with some states pulling ahead while others face tougher challenges. The national average FICO score sits at 714, showing remarkable stability even as economic pressures continue to test households everywhere.

I remember chatting with a friend from Minnesota who proudly mentioned his state’s top ranking. It got me thinking about what really drives these differences and, more importantly, what any of us can do to improve our own standing regardless of where we live. The gap between the highest and lowest states spans a full 66 points, which can translate into thousands of dollars in interest over a lifetime.

Understanding the National Credit Landscape in 2026

The Spring 2026 FICO Score Credit Insights report shows the country holding steady after minor fluctuations. While the average dipped by just one point from the previous year, nearly half of all consumers now boast scores of 750 or higher. That’s encouraging news, but it also highlights growing inequality in financial wellness across regions.

What fascinates me most is how geography seems to correlate with credit health. Factors like local economies, education levels, employment opportunities, and even cultural attitudes toward debt appear to play significant roles. Of course, these are broad trends rather than hard rules — plenty of individuals in lower-ranking states maintain excellent credit, just as some in top states struggle.

Let’s dive deeper into the data and explore what it means for you.

States Leading the Pack With Impressive Scores

Minnesota takes the crown this year with an impressive average of 742. Residents in the North Star State consistently demonstrate strong financial habits that contribute to this leadership position. Vermont follows closely at 740, with Wisconsin, New Hampshire, and Washington rounding out the top five.

These Upper Midwest and New England states share certain characteristics. Many have robust local economies, higher education attainment rates, and perhaps a more conservative approach to borrowing. In my experience talking with people from these areas, there’s often greater emphasis on living within one’s means and planning ahead.

- Minnesota: 742 — Strong job market and community values support excellent credit management.

- Vermont: 740 — Rural lifestyle paired with careful financial planning.

- Wisconsin: 739 — Balanced economy helps maintain steady scores.

- New Hampshire: 738 — Low taxes and fiscal responsibility shine through.

- Washington: 736 — Tech industry wages contribute to better debt management.

One thing I’ve noticed is that these high-scoring states often benefit from more stable employment. When people have predictable income, they’re better positioned to handle bills on time and keep credit utilization in check.

States Facing Greater Challenges

On the other end of the spectrum, Mississippi holds the lowest average at 676. Louisiana, Alabama, Georgia, and Oklahoma complete the bottom five. The southern cluster of lower scores points to systemic economic factors that deserve attention rather than judgment.

These numbers reflect real struggles with higher poverty rates, medical debt, and sometimes limited access to traditional banking services in certain communities. The 66-point spread between top and bottom isn’t just a statistic — it represents meaningful differences in borrowing costs and financial opportunities.

The difference of even 50 points can mean significantly higher interest rates on everything from car loans to mortgages.

I’ve seen how a lower credit score can create a cycle that’s hard to break. Higher interest payments eat into budgets, making it tougher to build savings or pay down debt faster. Breaking that cycle requires both personal action and sometimes broader support.

What Exactly Is a FICO Score?

Before we go further, let’s make sure we’re all on the same page about what these numbers actually mean. Your FICO Score is the most widely used credit scoring model in the United States, appearing in over 90% of lending decisions.

Scores range from 300 to 850 and fall into these categories:

- Very Poor: 300-579

- Fair: 580-669

- Good: 670-739

- Very Good: 740-799

- Excellent: 800-850

A higher score opens doors to better interest rates and loan approvals. Someone with excellent credit might save hundreds or even thousands on a mortgage compared to someone in the fair range. That’s real money that affects your daily life and long-term wealth building.

The Five Factors That Determine Your Score

Understanding how scores are calculated gives you the power to improve them. FICO looks at five main areas with different weights.

Payment history makes up 35% of your score. Simply put, do you pay your bills on time? This is the single biggest factor because it shows lenders your reliability. Even one late payment can hurt, especially if it’s recent.

Amounts owed accounts for 30%. This is your credit utilization ratio — how much of your available credit you’re actually using. Keeping balances below 30% of your limits is generally smart, and under 10% is even better.

Length of credit history contributes 15%. Older accounts help because they show a track record. New credit makes up 10%, while your mix of credit types (cards, loans, mortgages) rounds out the final 10%.

Consistency beats perfection when it comes to building credit. Small, steady improvements compound over time.

Why Regional Differences Exist

Several factors help explain why credit scores vary so much by state. Economic conditions play a huge role. Areas with higher median incomes and lower unemployment naturally tend to have stronger credit profiles.

Education levels matter too. States with more college graduates often show higher scores, possibly because higher education correlates with better financial literacy in many cases. Though I’ve met plenty of self-taught financial wizards without degrees who manage their money exceptionally well.

Access to healthcare and the prevalence of medical debt also influence outcomes. Unexpected medical bills can devastate credit if they’re not covered by insurance. Cost of living differences affect how much people need to borrow just to maintain basic lifestyles.

Cultural attitudes toward debt vary regionally as well. Some communities emphasize saving and paying cash, while others rely more heavily on credit for major purchases.

How Your Credit Score Impacts Daily Life

A strong credit score isn’t just about bragging rights. It affects everything from renting an apartment to getting a job in certain fields. Insurance companies often check scores when setting premiums, and utilities sometimes require deposits from those with thinner credit files.

Perhaps most significantly, your score determines the interest rates you’ll pay on big purchases. A difference of 100 points on a mortgage can mean paying tens of thousands more over the life of the loan. That money could have gone toward retirement, education, or simply enjoying life more.

| Score Range | Mortgage Rate Impact | Potential Extra Cost (30yr $300k) |

| Excellent (800+) | Lowest available | $0 |

| Good (670-739) | Moderate increase | $15,000+ |

| Fair (580-669) | Significant premium | $40,000+ |

These numbers aren’t exact for everyone, but they illustrate why improving your score deserves attention.

Practical Steps Anyone Can Take to Boost Their Score

The good news? Your location doesn’t determine your destiny. You have more control than you might think. Here are some proven strategies that work regardless of which state you call home.

Start With Free Credit Monitoring

Knowledge is power. Check your reports regularly from all three major bureaus. Look for errors that might be dragging your score down unfairly. Dispute inaccuracies promptly — many people find mistakes that improve their numbers once corrected.

Focus on Payment Reliability

Set up automatic payments for at least your minimum amounts. Even better, pay more than the minimum whenever possible. Your payment history carries the heaviest weight, so protecting it should be priority number one.

Manage Credit Utilization Wisely

Aim to keep your balances low relative to limits. If you’re carrying high balances, consider balance transfer options during promotional periods, but read the fine print carefully. Sometimes requesting a credit limit increase (without spending more) can help lower your utilization ratio.

Build Positive Payment History With Utilities

Services like Experian Boost can add on-time utility, phone, and streaming payments to your credit file. For many people, this provides a quick boost without any additional cost. Results vary, but the average reported increase is around 13 points for those who qualify.

Consider Balance Transfer Cards Strategically

If credit card debt is weighing you down, moving it to a card with a long 0% introductory APR period can save substantial interest. Just make sure you have a realistic payoff plan before the promotional rate ends.

Professional Help When Needed

For more complex situations involving multiple debts, credit repair services or debt relief programs might make sense. Look for reputable companies that offer transparent pricing and realistic expectations. Remember, you can often handle basic disputes yourself, but professional guidance helps when things get complicated.

Building Better Financial Habits Long-Term

Improving your credit score works best as part of a broader financial wellness strategy. Creating an emergency fund reduces the need to rely on credit cards when surprises hit. Learning to budget effectively helps you live within your means rather than constantly borrowing against future income.

I’ve found that people who track their spending for just one month are often shocked by where their money actually goes. That awareness alone leads to better decisions. Small changes like cooking more meals at home or reviewing subscriptions can free up cash to pay down debt faster.

Consider diversifying your credit mix thoughtfully over time. Having both revolving credit (cards) and installment loans (like auto loans paid responsibly) can help demonstrate your ability to manage different types of debt.

The Role of Financial Education

States with higher average scores often have stronger financial education programs in schools or community resources. Knowledge really is power when it comes to money management. Understanding compound interest, the true cost of minimum payments, and basic investing principles can transform your approach.

Even if your state doesn’t offer formal programs, plenty of free online resources exist. Books, podcasts, and reputable websites can teach you without costing anything except your time and attention.

The best time to start improving your credit was yesterday. The second best time is today.

Looking Ahead: Credit Trends to Watch

As the economy evolves, new factors will influence credit scores. The return of student loan payments affected many borrowers. Rising housing costs continue pressuring younger generations. Technology is changing how we access credit, with some alternative scoring models considering rent payments and utility bills more prominently.

Staying informed and adaptable will serve you well. The fundamentals remain the same — pay on time, don’t overextend yourself, and keep learning.

Taking Action Today

Wherever you live and whatever your current score shows, remember that change is possible. Start by pulling your free credit reports. Pick one area to focus on this month — maybe automating payments or reducing one credit card balance.

Celebrate small wins along the way. Each on-time payment and responsible decision builds momentum. Over time, those improvements compound just like interest, but in your favor this time.

Your credit score is more than a number. It’s a reflection of your financial habits and a tool that can either open doors or create barriers. By understanding the national picture and taking control of your personal situation, you position yourself for greater financial freedom and peace of mind.

Whether your state ranks at the top or bottom, your individual journey matters most. The data gives context, but your daily choices write the real story. What step will you take today toward a stronger financial future?

Improving credit takes patience and consistency, but the rewards are worth it. From better loan terms to increased confidence in your financial decisions, the benefits extend far beyond the score itself. Start small, stay committed, and watch your financial opportunities expand.

The map of average credit scores across America reminds us that while broad trends exist, individual action creates real change. Your score doesn’t define you, but improving it can certainly transform your options.