Have you filled up your tank lately and done a double take at the price? Or maybe you’ve been pricing out a summer trip only to close the browser in disbelief. If so, you’re not alone. What started as geopolitical tensions halfway around the world has quietly worked its way into the fabric of American daily life, touching everything from the morning commute to long-term dreams like buying a home.

I’ve been watching these numbers shift week by week, and the pattern is unmistakable. The conflict involving Iran has disrupted one of the most critical arteries of global energy, and the ripple effects are hitting wallets harder than many expected. Let’s walk through what’s really happening and why it matters to you right now.

The Hidden Costs Reaching Your Pocket

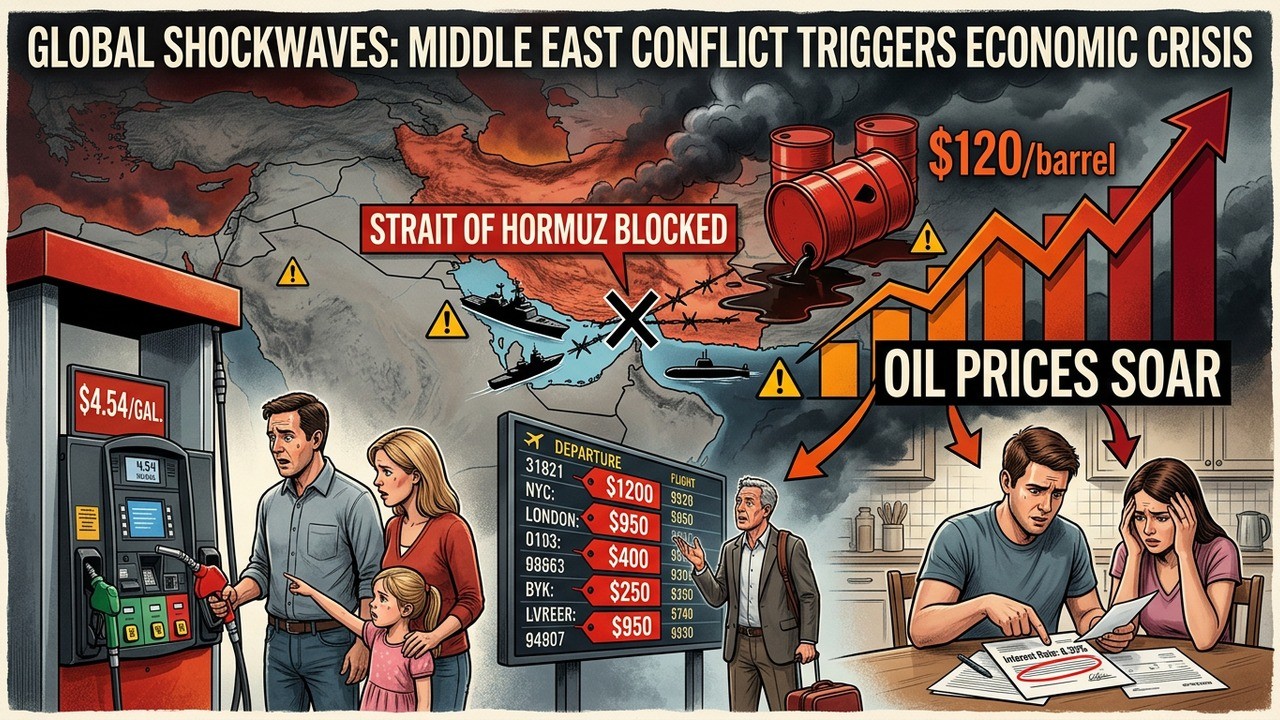

When major shipping routes get squeezed, the first thing that usually reacts is energy. The Strait of Hormuz isn’t just a name on a map — it’s the passage for roughly a quarter of the world’s oil supply. With that flow interrupted, markets went into panic mode almost immediately. Refineries adjusted, traders bid prices up, and before long, the increase landed squarely at local gas stations.

As of early May, the national average for regular gasoline sat at $4.54 per gallon. That’s more than a dollar and a half higher than where it was before the airstrikes began in late February. For a family that drives a typical 1,200 miles a month in a vehicle getting 25 miles per gallon, that single jump adds roughly $75 extra to the monthly budget. Over a year, we’re talking nearly a thousand dollars that could have gone toward groceries, savings, or even a family outing.

Why Energy Prices Moved So Fast

Oil is a global commodity, and fear travels even faster than tankers. Once traders saw the potential for prolonged disruption, futures contracts spiked. Refiners who rely on that crude had to pay more, and they passed a good portion of those costs downstream. It’s basic economics, but when it hits the pump, it feels anything but abstract.

I remember talking to a truck driver last week who said his weekly fuel expense had climbed by almost $400. Small businesses, delivery services, and farms are all absorbing similar blows. Those costs rarely stay isolated — they eventually show up in higher prices for goods on store shelves. So even if you don’t drive much, you’re still paying.

The speed with which energy markets reacted shows just how interconnected our world remains. A bottleneck thousands of miles away can change what you pay for milk and bread within weeks.

Beyond gasoline, jet fuel followed the same upward trajectory. Airlines don’t absorb these increases forever. Within a month, many carriers adjusted fares and added surcharges. The result? Average round-trip domestic flights climbed nearly 24 percent compared to the previous year, while international tickets jumped a staggering 42 percent — from around $775 to over $1,100 on average.

Flying Feels More Expensive Than Ever

Picture planning a long-awaited vacation only to discover the ticket price has ballooned. That’s the reality many families faced this spring. Budget carriers and legacy airlines alike raised base fares, and extra fees for checked bags became even more common. One major airline quietly increased its first-checked-bag fee by $10 on certain routes, a small-sounding change that adds up quickly for a family of four.

What surprises me most is how quickly leisure travel adjusted. People didn’t stop flying entirely, but many shifted to closer destinations or shorter trips. Others simply postponed plans. The hospitality industry in popular international spots is already feeling the slowdown, which creates its own set of economic ripples.

- Higher jet fuel costs passed directly to ticket prices

- Increased ancillary fees for baggage and seat selection

- Reduced flight frequency on less profitable routes

- Shift toward domestic or regional travel alternatives

If you’re someone who travels for work, the impact might feel even more direct. Companies are scrutinizing travel budgets more carefully, sometimes requiring employees to take longer layovers or fly economy on routes they once booked in premium cabins. These small adjustments compound over time.

Mortgage Rates and the Dream of Homeownership

Just when it seemed mortgage rates might ease, the conflict sent them climbing again. Before the escalation, the 30-year fixed rate had dipped to 5.98 percent — the lowest in years. That brief window of hope closed fast. As investors sought safety in government bonds and inflation fears returned, rates pushed toward 6.30 percent and showed little sign of retreating quickly.

For someone buying a $400,000 home with a 20 percent down payment, that one-third of a percent difference adds roughly $70 to the monthly payment. Over a 30-year loan, that’s thousands of extra dollars. First-time buyers who were already stretching their budgets feel this squeeze the most.

I’ve spoken with several young couples who put their home searches on pause. The combination of higher rates and elevated building material costs (themselves influenced by energy prices) made the numbers simply not work. Others are choosing to rent longer or look at more affordable markets farther from city centers.

Interest rate movements might seem distant until you sit down with a lender and realize your qualifying amount just dropped by tens of thousands of dollars.

Broader Inflation Picture

The latest Consumer Price Index reading came in at 3.3 percent year-over-year — the highest since last April. Energy was the primary driver, but the effects spread. Transportation costs, manufacturing inputs, and even some food categories felt the pressure. When oil prices rise, so does the cost of fertilizers, plastics, and shipping everything from coast to coast.

This isn’t the kind of inflation that appears overnight and vanishes. It builds gradually, changing behaviors and expectations. Families start cutting discretionary spending. Businesses delay investments. The whole economy moves a little more cautiously.

| Category | Pre-Conflict Average | Current Average | Change |

| Regular Gas | $2.98 | $4.54 | +$1.56 |

| Intl Round-Trip Flight | $775 | $1,101 | +42% |

| 30-Year Mortgage | 5.98% | 6.30% | +0.32 pts |

Looking at numbers like these makes the abstract feel concrete. Each percentage point carries real stories — a parent choosing between filling the tank or stocking the pantry, a graduate delaying a move because rent plus commuting costs became too much.

How Different Households Are Coping

Not everyone feels these changes the same way. Rural families with long commutes notice the gas price jump immediately. Urban professionals who rely on rideshares see surge pricing more often. Frequent flyers are rethinking loyalty programs and exploring points strategies more creatively than before.

Some households are turning to budgeting apps with renewed seriousness. Others are carpooling, combining errands, or even switching to public transit where available. On the housing side, more buyers are considering adjustable-rate mortgages again, accepting the risk for a lower initial payment. Whether that proves wise remains to be seen.

In my view, the most sensible approach right now is awareness paired with flexibility. Small changes — like adjusting driving habits, booking travel further in advance, or locking in rates if you’re close to buying — can soften the blow. But pretending the situation will resolve itself quickly might lead to unpleasant surprises.

Longer-Term Economic Questions

Sixty-eight days in, it’s still early. Markets hate uncertainty, and prolonged conflict keeps that uncertainty alive. If the disruption to oil flows continues, we could see sustained higher energy prices feeding into core inflation. The Federal Reserve then faces a difficult balancing act between supporting growth and keeping prices in check.

Investors have already rotated toward certain sectors. Energy companies posted strong gains while travel and real estate stocks faced pressure. For everyday people without large portfolios, those market moves translate into higher costs at the store and pump rather than portfolio protection.

Perhaps what stands out most is how quickly global events become local realities. A decision made in a distant capital can change the calculation for a car loan, a family vacation, or the affordability of the neighborhood you hoped to settle in. That interconnectedness is both impressive and, at times, unsettling.

Looking ahead, several factors could ease the pressure. Diplomatic progress, increased production elsewhere, or strategic releases from reserves might help stabilize markets. On the other hand, any escalation could push prices even higher. Most analysts I’ve read suggest preparing for volatility rather than betting on a quick return to pre-conflict levels.

Practical Steps You Can Take Now

- Review your driving and commuting habits — even small reductions help

- Book travel earlier and remain flexible on dates and destinations

- If buying a home, run the numbers at several different rate scenarios

- Build or maintain a buffer in your budget for unexpected cost increases

- Consider energy-efficient upgrades if you own a vehicle or home

These aren’t revolutionary ideas, but they’re practical. In times like these, steady habits often outperform dramatic gestures. I’ve found that simply tracking expenses more closely for a couple of weeks reveals opportunities most people miss.

The situation also highlights the importance of diversified savings and investments. While no one can fully escape macroeconomic forces, having different income streams or assets that perform well during inflation can provide some cushion.

What This Means for Different Generations

Younger adults just entering the housing market face steeper barriers than their parents did at the same age. Millennials and Gen Z who delayed homeownership due to student debt or high rents now confront another obstacle. Some are choosing to invest in themselves — further education, skill development — hoping higher future earnings will offset today’s costs.

Middle-aged families with children feel the dual pressure of rising daily expenses and saving for college or retirement. They’re the ones most likely to cut restaurant meals, delay car replacements, or rethink vacation plans. Seniors on fixed incomes are perhaps the most vulnerable, as even modest inflation erodes purchasing power quickly.

Each group responds differently, yet the underlying challenge remains the same: limited control over forces that shape daily financial reality. Recognizing that limitation can actually be liberating — it shifts focus toward the decisions we can control.

Economic shocks test resilience. Those who adapt thoughtfully tend to weather the storm better than those who wait for conditions to improve on their own.

As the weeks turn into months, the conversation around energy independence, diversified supply chains, and fiscal preparedness will likely intensify. These aren’t just policy topics — they translate into tangible differences in what families can afford.

Staying Informed Without Panic

It’s easy to get overwhelmed by headlines. My approach has been to focus on verifiable data — average prices, official inflation reports, reliable industry updates — rather than speculation. Understanding the mechanics helps separate signal from noise.

Gas prices, for instance, respond to both global events and seasonal factors. Summer driving season could push them higher still, while any resolution in the conflict might bring relief. Mortgage rates depend on bond yields, inflation expectations, and central bank policy. Keeping an eye on these moving pieces provides context.

Ultimately, this period reminds us how interconnected our lives are with global stability. Peace and reliable trade routes aren’t just abstract ideals — they’re foundations for predictable costs and planning. When those foundations shake, we adjust, innovate, and sometimes reconsider priorities.

Whether you’re watching the pump, checking flight deals, or calculating mortgage payments, these shifts matter. They shape decisions big and small. By understanding the “why” behind the numbers, we position ourselves to respond more effectively rather than simply react.

The coming months will reveal more about the duration and depth of these effects. For now, staying flexible, informed, and proactive remains the most practical strategy. Your financial well-being often depends less on predicting the future perfectly and more on preparing thoughtfully for whatever comes.

These changes didn’t happen in isolation, and they won’t resolve in isolation either. The choices made by leaders, businesses, and individuals will determine how long higher prices persist and how deeply they reshape habits and expectations. In the meantime, paying attention and making incremental adjustments can help protect what matters most — your financial stability and peace of mind.