Have you noticed gas prices creeping up again lately? Just when many of us were hoping for some relief at the pump, reports show US gasoline inventories are dropping sharply. This isn’t some minor fluctuation either. The combination of surging exports and surprisingly strong domestic demand has created a noticeably tight situation in the market.

As someone who follows energy trends closely, I’ve seen these dynamics play out before, but the current pace feels particularly intense. We’re heading into the heart of summer driving season with stockpiles already well below normal seasonal levels. This raises important questions about where prices might go next and how it could affect everything from family road trips to broader economic pressures.

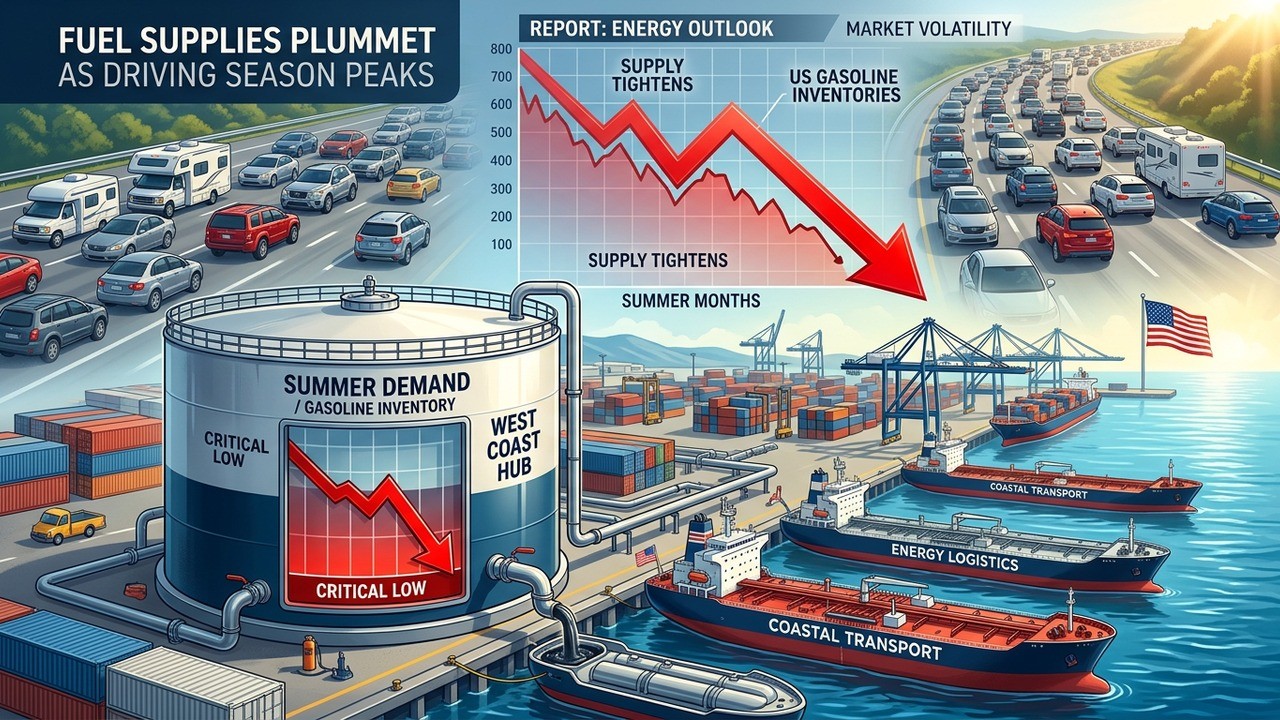

The Tightening Gasoline Market in Focus

The numbers tell a compelling story. Since early April, gasoline inventories have been drawing down at an average rate of around 0.7 million barrels per day. That’s a rapid pace that has pushed levels about 5% below their typical seasonal median. For context, this kind of consistent draw isn’t something that happens without significant underlying forces at work.

What makes this situation particularly interesting is how multiple factors are converging at once. It’s not just one thing causing the decline but rather a perfect storm of export strength, steady home consumption, and refinery decisions favoring other products. Understanding each piece helps paint a clearer picture of why the market feels so stretched right now.

Surging Net Exports Draining Domestic Supply

One of the biggest contributors to lower inventories has been the sharp rise in US gasoline exports. On a four-week average basis, net exports are up roughly 0.34 million barrels per day compared to the same period last year. That’s a substantial increase that effectively pulls product away from the domestic market.

Why are so much more barrels heading overseas? The answer lies in price differences. Currently, wholesale gasoline prices in the United States sit approximately 15% higher than in Asia and Europe. This creates a strong incentive for exporters to ship product where margins are attractive internationally. While this benefits refiners in the short term, it contributes to tighter conditions at home.

The export pull has been relentless, removing supply that would otherwise help rebuild inventories during what is typically a rebuilding period.

In my experience following these markets, when exports ramp up this aggressively, it often signals underlying strength in global demand or specific regional shortages abroad. Either way, the effect on US stockpiles is direct and measurable.

Domestic Demand Proving Remarkably Resilient

Despite higher prices, American drivers aren’t cutting back significantly. Gasoline demand is holding up remarkably well, sitting only about 0.2 million barrels per day below year-ago levels. This resilience comes as we enter the peak summer driving season, traditionally a time of high consumption for vacations, road trips, and general travel.

It’s worth noting that we haven’t seen clear signs of demand destruction yet. Many households appear to be absorbing the higher costs rather than altering their driving habits dramatically. This could reflect strong employment, pent-up travel desires after previous years of disruption, or simply the necessity of commuting in many parts of the country where alternatives remain limited.

- Strong summer driving season expectations

- Limited immediate behavioral changes despite prices

- Regional variations in consumption patterns

This steady demand adds another layer of pressure to already declining inventories. When you combine it with heavy exports, the math becomes challenging for maintaining comfortable buffer stocks.

Refinery Incentives Shifting Production Mix

Refineries aren’t just passive players in this story. Strong margins for jet fuel and diesel have encouraged operators to adjust their yields, producing more of those products at the expense of gasoline. This makes perfect economic sense for the facilities but further constrains gasoline supply availability.

The economics here are straightforward. When distillate products command better returns, refiners optimize their operations accordingly. The result is less gasoline entering the market even as demand and exports pull from existing stocks. It’s a classic example of market signals directing production decisions in real time.

Price Implications and International Comparisons

On the pricing front, the tightness is already visible. US wholesale gasoline prices stand notably higher than equivalent benchmarks in other major regions. This spread not only encourages exports but also keeps upward pressure on domestic retail prices. Current retail levels are hovering just fifty cents per gallon below all-time highs.

I’ve found that these kinds of price differentials often persist until inventories rebuild or other market balances shift. For consumers, it translates to higher costs at the pump during what should be a peak travel period. The situation bears watching closely as it could influence everything from inflation readings to consumer confidence.

Broader Oil Market Context

While gasoline takes center stage here, the wider crude oil picture provides important background. Brent and WTI futures have shown strength recently, supported by various geopolitical factors and overall market tightness. However, some counterbalancing elements like strategic releases and demand adjustments elsewhere have kept prices from exploding higher.

International agencies have noted significant supply deficits in recent periods, though estimates vary somewhat depending on the source. Demand revisions, particularly in certain regions and product categories, have played a role in shaping expectations. Supply from key producing areas has also surprised to the upside in some cases, adding nuance to the overall balance.

Global inventories are under pressure, but regional dynamics and government actions create a complex picture for traders and analysts alike.

US production has also shown resilience, with recent quarterly figures beating expectations in both exploration and production segments as well as from larger operators. This domestic output helps offset some international uncertainties but doesn’t fully resolve the product-specific tightness in gasoline.

Potential Policy Responses and Risks

As retail gasoline prices climb, discussions around potential policy interventions naturally arise. While export restrictions aren’t the base expectation, their probability increases alongside price pressures. Such measures would represent a significant shift and could have wide-ranging implications for both domestic and international markets.

Government inventory releases have played a role in recent months, with strategic petroleum reserves providing some offset, primarily on the crude side rather than refined products. This distinction matters because it highlights where the most acute pressures exist in the current environment.

- Monitoring price thresholds that might trigger policy debate

- Assessing the effectiveness of past release programs

- Considering longer-term impacts on market signals

In my view, the preference remains for market-driven adjustments whenever possible. However, sustained high prices at the consumer level often bring political considerations into play, creating additional uncertainty for energy producers and traders.

What This Means for Summer and Beyond

With driving season upon us, the current inventory trajectory suggests continued vigilance on prices. Families planning vacations might face higher fuel costs than anticipated. Businesses reliant on transportation could see margin pressures build if the tightness persists.

Looking further ahead, several variables could shift the balance. Refinery maintenance schedules, weather impacts on demand, potential resolutions to geopolitical tensions, and evolving consumption patterns all play a part. The market’s ability to respond flexibly will determine whether this tightness proves temporary or signals a more prolonged period of elevated prices.

One aspect I find particularly noteworthy is how resilient US demand has remained. It speaks to the fundamental role petroleum products still play in our daily lives and economy. While transitions to other energy sources continue, the immediate reality is one where gasoline demand isn’t fading away quickly.

Understanding Refinery Operations and Yields

To appreciate the current situation fully, it helps to understand how refineries work. These complex facilities process crude oil into various products through fractional distillation and other processes. The yield of each product can be adjusted within certain limits based on market signals and equipment configuration.

When jet fuel and diesel margins strengthen considerably, operators maximize those outputs. This often means less gasoline produced from each barrel of crude. Combined with strong export pull, the domestic gasoline pool shrinks faster than it can be replenished. It’s a textbook case of profit maximization at the refinery level creating upstream and downstream effects.

| Factor | Impact on Inventories | Current Status |

| Net Exports | Decreasing | Significantly Higher YoY |

| Domestic Demand | Decreasing | Near Year-Ago Levels |

| Refinery Yields | Decreasing Gasoline | Shifted to Distillates |

This dynamic isn’t new, but the intensity this year stands out. Analysts will be watching closely to see if margins rebalance or if the current pattern holds through the summer months.

Global Demand Nuances and Revisions

While the US gasoline story dominates domestic headlines, global oil demand estimates have seen adjustments. Certain regions and product categories have shown softer consumption than previously forecasted. This includes areas like China where strategic measures and economic factors influence overall usage.

However, other segments demonstrate strength, particularly in the US where diesel and gasoline have surprised positively. These regional differences highlight why a one-size-fits-all view of the oil market often misses important details. Supply responses from major producers add yet another layer of complexity.

The role of storage capacity and logistical constraints also can’t be overlooked. Some producing regions have managed higher output than expected, possibly due to better management of storage limitations than initially anticipated.

Consumer Perspective and Practical Implications

For the average driver, this all translates to higher costs that hit the wallet during a time when many look forward to summer travel. Planning ahead, combining trips, and maintaining vehicles for better efficiency become even more relevant strategies. Small changes can help mitigate the impact of elevated prices.

Beyond individual consumers, industries like trucking, aviation, and shipping watch these developments closely. Their cost structures depend heavily on fuel prices, and those costs often get passed along through higher prices for goods and services. The ripple effects extend throughout the economy.

Perhaps the most interesting aspect is how markets eventually self-correct. Higher prices encourage more production, discourage excessive consumption, and attract imports when profitable. The question is always about timing and magnitude of these adjustments.

Looking Ahead With Cautious Optimism

While the current inventory situation warrants attention, it’s important to maintain perspective. Energy markets are inherently cyclical, and today’s tightness could pave the way for future balance as participants respond to the signals. Monitoring key indicators like weekly inventory reports, refinery utilization rates, and export trends will provide ongoing clues.

In my experience, the most successful approach involves staying informed without overreacting to short-term volatility. The fundamentals suggest a tight near-term picture for gasoline, but longer-term factors including production growth, technological changes, and policy developments will shape the years ahead.

Drivers might want to keep an eye on regional price variations and consider flexible travel plans where possible. For those in the industry, the current environment rewards careful risk management and attention to shifting margins across the product slate.

As we move through the summer months, this gasoline market story will likely continue generating interest. The interplay between exports, domestic needs, and global factors creates a rich tapestry for analysis. While challenges exist, they also highlight the adaptability and depth of modern energy systems.

Ultimately, staying attuned to these developments helps all of us better understand the forces shaping our daily costs and economic landscape. The plunging inventories serve as a reminder of how interconnected our energy choices remain, both at home and on the global stage. The coming weeks and months will reveal how these tensions resolve and what new balances emerge.

The situation underscores the importance of diversified energy strategies and continued investment in reliable supply chains. Whether you’re filling up your tank for a weekend getaway or analyzing broader market trends, the current gasoline inventory dynamics offer plenty to consider. Keep watching the data as it unfolds.