Have you ever pulled up to the gas pump, seen the price, and wondered why it feels so disconnected from what you hear about oil markets on the news? It seems like crude oil prices hover around certain levels, yet filling up your tank still stings more than expected. I’ve thought about this a lot, and the truth is more nuanced than most quick takes suggest.

The energy system that delivers fuel to our cars isn’t a straight line from well to wheel. It’s a complex web full of moving parts, each capable of creating friction that affects what we ultimately pay. When someone points to similar oil prices from years ago and questions why gasoline costs more now, they often overlook the hidden pressures building up behind the scenes.

The Real Forces Shaping What You Pay at the Pump

Let’s start with a simple truth I’ve observed over years of following these markets: gasoline is not crude oil. It’s a refined product that goes through multiple transformations and logistical challenges before it reaches your local station. This distinction matters more than many realize, especially during periods of tight capacity or global uncertainty.

Back in 2011, different conditions prevailed across the supply chain. Refineries operated with more flexibility in some regions, and certain geopolitical factors hadn’t yet created the lasting bottlenecks we see today. Fast forward to now, and the picture has shifted in important ways that directly impact your wallet.

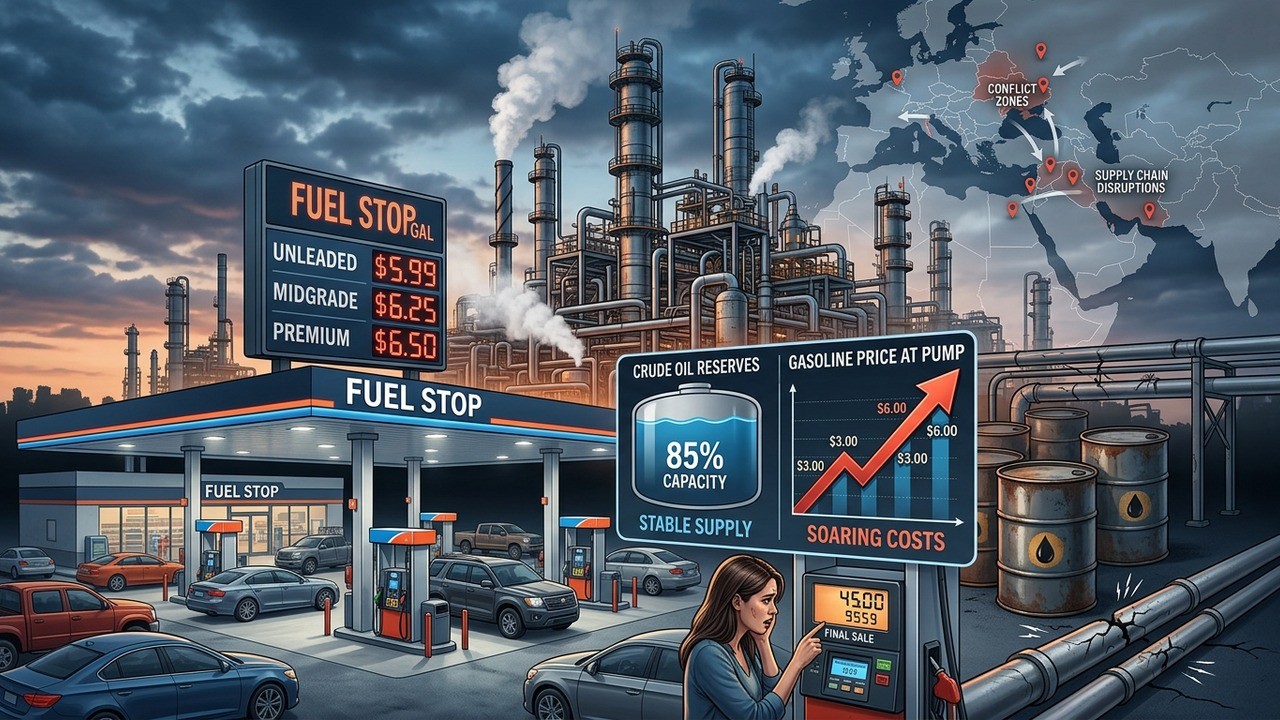

Refining Capacity: The Often Ignored Bottleneck

One of the biggest changes involves how much fuel we can actually produce from available crude. Over the past decade, several factors led to reduced refining capabilities in key areas. Some facilities closed permanently, others shifted focus toward different outputs, and investment in new capacity slowed considerably.

Meanwhile, demand bounced back strongly after pandemic disruptions. This combination means refineries often run near maximum capacity – think mid-90% utilization rates on a consistent basis. At those levels, there’s virtually no cushion when something unexpected happens.

This tightness shows up clearly in something called the crack spread – essentially the difference between crude oil costs and the value of refined products like gasoline and diesel. When processing capacity gets constrained, these margins widen naturally as the market signals the need for more careful allocation of limited resources.

The energy supply chain behaves like a finely tuned machine. Push it too hard in one area, and the effects ripple through everything else.

In practical terms, this means you can have relatively stable crude prices but still face higher pump prices because the system struggles to convert that oil into usable fuel efficiently. It’s not about greed in the simplistic sense, but rather the physical realities of production limits.

Geopolitical Disruptions and Their Hidden Costs

Global events add another layer of complexity that pure price charts fail to capture. Conflicts and tensions in critical shipping regions don’t just affect the headline cost of crude. They change routes, increase insurance premiums, delay deliveries, and force refineries to adapt to different types of oil than they were optimized for.

Refineries are incredibly specialized facilities. Each one is designed around processing particular grades of crude. When supply patterns shift dramatically – due to sanctions, regional instability, or trade route issues – operators may need to use less ideal feedstocks. This can lower gasoline yields per barrel and raise overall costs.

- Longer shipping distances increase transportation expenses

- Higher insurance costs get passed down the chain

- Logistical delays create temporary shortages at key points

- Suboptimal crude processing reduces efficiency

These factors compound over time, creating a situation where the final price at the pump reflects much more than just the raw material cost. It’s like trying to bake the same cake with different ingredients and a smaller oven – the end result simply costs more to produce.

Learning From Past Disruptions

This isn’t the first time we’ve seen such divergences. Consider major hurricanes in the past that took refining capacity offline. In some cases, crude prices actually eased because less processing meant less immediate demand for raw oil. Yet gasoline prices shot up due to actual shortages of finished product in affected regions.

The system operates as an interconnected chain. Strengthen or weaken one link, and the entire structure adjusts accordingly. Today’s pressures come not from a single storm but from a combination of structural changes and ongoing international developments.

Perhaps the most interesting aspect is how quickly markets can shift. What looks like profiteering from the outside often represents the market’s attempt to balance supply and demand under real physical constraints. I’ve seen this pattern repeat enough times to recognize when surface-level explanations fall short.

Profits in Context: Cause or Effect?

Energy companies do report healthy profits during these periods, which naturally draws attention. However, it’s crucial to distinguish between correlation and causation. High prices driven by constraints tend to generate higher margins as a result, not the other way around.

If companies could simply choose higher prices without regard to market conditions, we’d expect more consistent behavior across different periods. Instead, we see prices responding to specific pressures in the supply chain. Strong profits reflect the market rewarding those who can navigate these challenges effectively.

High prices are often symptoms of underlying constraints rather than evidence of manipulation.

This distinction matters tremendously for policy responses. Suggestions like special taxes on profits might feel satisfying, but they risk discouraging exactly the kind of investment needed to ease future bottlenecks. It’s a delicate balance that requires careful thought.

The Infrastructure Investment Challenge

Building and maintaining energy infrastructure takes significant time and capital. Refineries represent multi-billion dollar commitments with decades-long operational horizons. When policy uncertainty or regulatory hurdles increase, companies naturally become more cautious about committing those resources.

We’ve witnessed this dynamic play out over recent years. Some facilities were repurposed or shuttered amid shifting priorities toward alternative energy sources. While long-term transitions have their place, the immediate effect was reduced capacity precisely when demand recovered strongly.

- Assess current refining utilization rates and identify pinch points

- Evaluate midstream infrastructure needs for efficient distribution

- Consider permitting processes that affect new project timelines

- Balance environmental goals with reliable supply requirements

Finding the right approach here isn’t easy. We need reliable fuel supplies today while also progressing toward future energy mixes. Getting this balance wrong could lead to even more volatile price swings down the road.

Global Market Dynamics at Play

Energy markets operate on a truly international scale. What happens in one region reverberates elsewhere, sometimes in unexpected ways. Demand growth in developing economies, production decisions by major exporters, and shifting trade patterns all influence the final price consumers face.

Consider how specialized the entire supply chain has become. Different crude grades serve different refining configurations. When availability of preferred types changes, adjustments throughout the system create additional costs and inefficiencies that accumulate.

In my experience following these issues, the most persistent challenges often stem from these kinds of structural factors rather than any single villain in the story. Understanding that complexity helps explain why simple comparisons across years can mislead.

What Effective Solutions Might Look Like

If the goal is genuinely lower and more stable fuel prices, the focus should shift toward addressing root causes. This means thinking seriously about capacity, infrastructure resilience, and reducing unnecessary frictions in the system.

Encouraging investment in key parts of the supply chain could help build more slack into the system. Streamlining certain regulatory processes without compromising safety standards might accelerate needed projects. Diversifying supply sources and strengthening logistical networks would add valuable resilience.

| Factor | Impact on Prices | Potential Solution |

| Refining Capacity | High when tight | Targeted infrastructure investment |

| Geopolitical Events | Disruptive and unpredictable | Diversified sourcing strategies |

| Logistics Efficiency | Variable cost driver | Modernized transportation networks |

These aren’t quick fixes, and they require coordinated effort across government and industry. But they stand a better chance of delivering meaningful results than approaches that misdiagnose the fundamental issues.

Looking Beyond Headlines

It’s tempting to seek simple villains when prices rise. The reality, however, usually involves a web of interconnected factors that no single actor fully controls. Crude oil prices matter, of course, but they represent just one piece of a much larger puzzle.

Consumers deserve honest conversations about these dynamics. Policymakers particularly need to grapple with the technical realities rather than convenient narratives. Getting the diagnosis right matters because it determines whether proposed remedies will actually help or potentially make things worse.

In the end, stable and affordable energy requires acknowledging physical limits, incentivizing necessary investments, and maintaining a pragmatic approach to global realities. Ignoring these elements won’t make the challenges disappear – it only delays finding real solutions.

The next time you hear comparisons between current gas prices and previous periods, consider asking what else might have changed in the system. The answer often reveals more than any single price chart could show. Understanding these nuances empowers better decisions, whether as consumers, voters, or engaged citizens following energy issues.

Energy markets will always involve some level of volatility given their global nature and the massive infrastructure involved. But by focusing on capacity, efficiency, and resilience, we can work toward a system that better serves everyone in the long run. That’s ultimately the conversation worth having.

As we navigate these ongoing challenges, keeping an open mind about the technical details helps cut through the noise. The goal isn’t to defend any particular industry but to seek genuine understanding of what drives the prices we all experience. In that spirit, examining the full picture rather than isolated data points offers the clearest path forward.