Have you ever opened your mortgage statement and felt that sudden pit in your stomach? You thought locking in a fixed rate would keep things predictable, yet here comes another increase in your monthly payment. You’re not alone in this frustration, and it’s happening more often than many realize.

The reality is that a fixed-rate mortgage doesn’t shield you from every cost associated with homeownership. For most people, that payment includes more than just principal and interest. Those extra pieces tucked into an escrow account are where the real surprises often hide, especially lately.

The Hidden Side of Your Monthly Mortgage Payment

When you signed on the dotted line for your home loan, the lender probably set up an escrow account to handle property taxes, homeowners insurance, and possibly mortgage insurance. This setup makes life easier by spreading those big annual bills into manageable monthly chunks. But what happens when those underlying costs shoot up faster than expected?

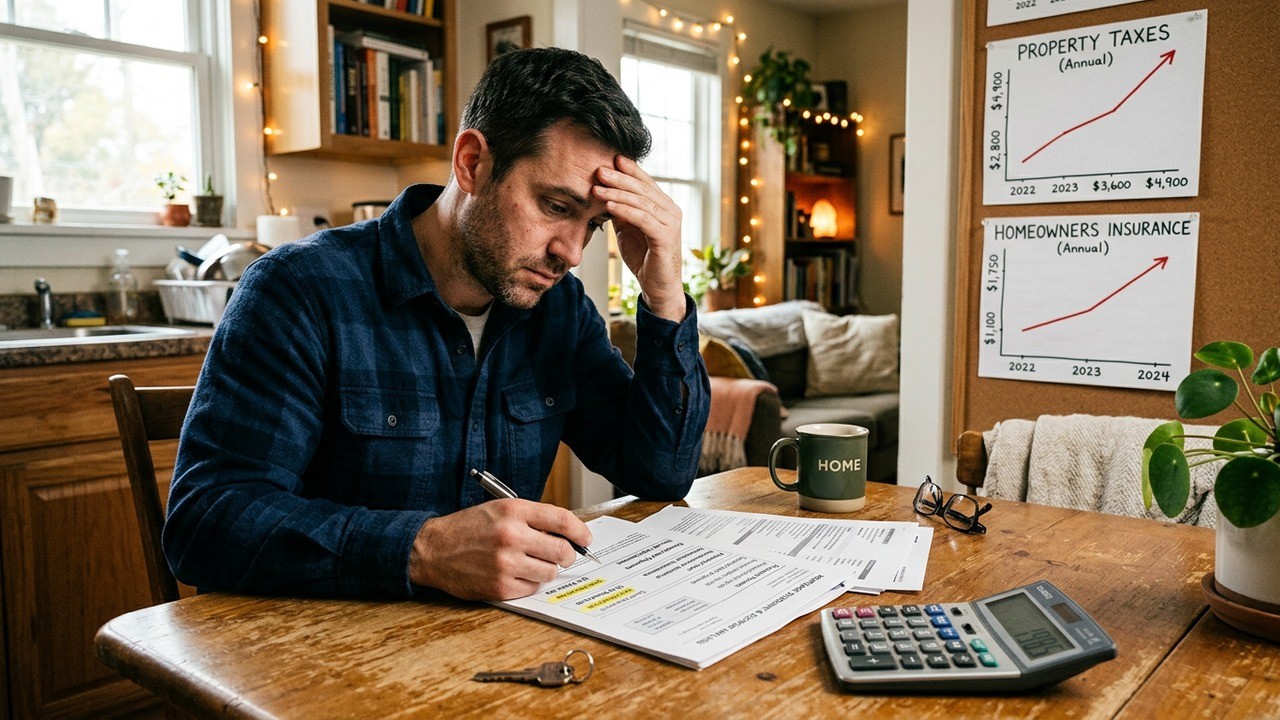

Recent years have brought some significant shifts. Insurance premiums have climbed sharply due to more frequent severe weather events, while home values pushing higher have pulled property tax assessments along for the ride. The result? Many escrow accounts now show shortfalls that get passed back to homeowners through higher payments.

I’ve spoken with enough homeowners over the years to know this can feel like a betrayal of the “fixed” promise. Yet understanding the mechanics helps you respond smarter instead of just feeling stuck.

How Escrow Accounts Actually Work

Escrow isn’t some mysterious bank trick. It’s essentially a holding account managed by your mortgage servicer. Each month, a portion of your payment goes in to cover upcoming bills for taxes and insurance. Once a year, they review the account, project future expenses, and adjust your monthly contribution accordingly.

If the projections show they’ll come up short, they recalculate. That $2,000-plus average shortage many are facing this year doesn’t hit all at once. Lenders typically spread it over the next twelve months, which means a noticeable bump in what you send each month.

The key thing to remember is that your principal and interest stay fixed, but the escrow portion is designed to flex with real-world costs.

This system protects both you and the lender. Without it, you’d face massive lump-sum bills twice a year that could catch anyone off guard. Still, when adjustments happen repeatedly, it starts to feel like your budget is on a rollercoaster.

Why Costs Have Jumped So Dramatically

Let’s talk numbers that matter. Homeowners insurance costs have risen substantially across the country. Factors like increased natural disasters, rebuilding expenses after storms, and inflation in construction materials all play a role. In certain states hit hard by weather patterns, the increases feel particularly painful.

Property taxes tell a similar story. As home prices climbed over recent years, local assessors took notice. Higher valuations usually translate to higher tax bills. Even if millage rates stay stable, the base value going up means you pay more.

Combined, these two big-ticket items have pushed escrow requirements notably higher for a large percentage of borrowers. What used to feel like a small add-on to your mortgage payment now commands serious attention in family budgets.

Real Impact on Homeowners Like You

Picture this: A family in a suburban neighborhood budgets carefully each month. They thought they had breathing room after buying during a period of relatively stable rates. Then the annual escrow analysis arrives, and suddenly their payment jumps by nearly two hundred dollars. That might mean cutting back on dining out, delaying a family vacation, or rethinking contributions to savings goals.

In my experience working with personal finance topics, these increases hit hardest for those on tighter budgets or living in high-cost or high-risk areas. Retirees on fixed incomes face particular challenges when these adjustments roll through.

- Young families stretching to afford their first home

- Middle-aged homeowners balancing kids’ activities and aging parents’ needs

- Retirees hoping for predictable expenses in their golden years

Each group feels the pressure differently, but the common thread is the surprise element that disrupts carefully laid plans.

Options When Your Escrow Falls Short

When the notice arrives, you usually have choices. The most common path is accepting the higher monthly payment spread over the next year. It keeps things manageable but extends the pain. Some lenders let you pay the shortage in one lump sum if you have the cash available.

Paying upfront can make sense if you have solid emergency reserves. It stops the monthly creep and lets you reset your budget around the new baseline costs. However, don’t drain your safety net just to avoid higher payments. Financial peace matters more than short-term relief.

Sometimes the smartest move is spreading the shortage while simultaneously looking for ways to lower the ongoing expenses.

That balanced approach prevents panic while still addressing root causes.

Tackling Rising Homeowners Insurance

Insurance represents one of the fastest-growing pieces of the escrow puzzle lately. Shopping around for better rates can yield real savings. Different companies assess risk differently, so quotes vary more than you might expect.

Consider raising your deductible if you have enough savings to cover a larger out-of-pocket expense. Bundling policies or improving home security features might unlock discounts too. Small changes add up when premiums have climbed as much as they have.

Of course, don’t sacrifice proper coverage just to save money. The goal is finding the sweet spot between protection and affordability. Review your policy annually rather than automatically renewing.

Navigating Property Tax Increases

Property taxes feel particularly personal because they reflect your home’s assessed value. If you believe the assessment seems too high compared to recent sales of similar properties, you might have grounds for an appeal. Success requires solid evidence and patience with local processes.

Many areas offer exemptions or reductions for certain groups. Seniors, veterans, or those with disabilities sometimes qualify for relief. Checking eligibility doesn’t cost anything and could provide meaningful savings.

- Gather recent comparable sales data in your neighborhood

- Document any issues with your property that might affect value

- File the appeal within the required timeframe

- Be prepared to explain your case clearly

Even if an appeal doesn’t fully succeed, the process often clarifies how your taxes get calculated.

Longer-Term Strategies for Housing Costs

Beyond immediate fixes, thinking strategically about your overall financial picture helps. Could refinancing make sense if rates drop? Maybe adding energy-efficient improvements could lower insurance rates or increase home value thoughtfully.

Building a larger emergency fund specifically earmarked for housing surprises provides peace of mind. Many experts suggest aiming for at least six months of expenses, but when it comes to homeownership, having closer to a year’s worth might feel more comfortable given recent volatility.

I’ve always believed that true financial security comes from understanding where your money goes rather than just trying to earn more. Tracking housing-related expenses separately from other bills brings clarity that helps with future decisions.

What This Means for Future Homebuyers

If you’re still shopping for a home, factor these realities into your calculations. Don’t stretch your budget assuming taxes and insurance will remain flat. Build in a cushion for potential increases over time.

Consider locations carefully. Areas with stable tax policies or lower disaster risk might offer more payment predictability. Working with knowledgeable real estate professionals who understand local cost trends can prevent nasty surprises down the road.

Staying Proactive With Your Mortgage Servicer

Communication matters. If you anticipate difficulty with an increased payment, reach out to your servicer early. They sometimes have flexibility or can explain options you might have missed. Ignoring the issue only leads to late fees and stress.

Keep good records of all communications. Understanding exactly how your escrow gets calculated empowers you during annual reviews. Some homeowners even request more frequent analyses if costs seem especially volatile in their area.

| Expense Type | Recent Trend | Potential Action |

| Homeowners Insurance | Significant increases | Shop quotes annually |

| Property Taxes | Rising with values | Review assessments |

| Escrow Shortfall | Common in 2026 | Choose lump sum or spread |

Tools like this help visualize where your money flows and where opportunities for control exist.

Balancing Homeownership Dreams With Financial Reality

Owning a home remains a powerful goal for many, offering stability and potential appreciation. Yet the past several years have shown that costs don’t always behave predictably. Adapting to these changes rather than fighting them marks the difference between stressed homeowners and those who thrive despite challenges.

Perhaps the most valuable lesson here is building flexibility into your financial life. Whether through side income, better budgeting, or simply cultivating a mindset that expects some variability, preparation beats reaction every time.

I’ve come to appreciate how these unexpected bumps can actually force positive changes. Families review spending habits more carefully. They explore ways to make their homes more efficient. Some even discover new skills or opportunities while figuring out solutions.

Looking Ahead in an Evolving Housing Market

While current pressures feel intense, markets tend to cycle. Insurance companies and policymakers continue working on ways to manage risk better. Home values may stabilize in some regions. Understanding these broader patterns helps maintain perspective when your specific payment notice arrives.

For those planning retirement, these housing cost dynamics deserve special attention. Many envision their home as a cornerstone of their later years, either by aging in place or through eventual sale. Unexpected ongoing increases can impact both quality of life and long-term projections.

Consider consulting with financial professionals who understand both real estate and retirement planning. They can help model different scenarios and suggest adjustments before problems compound.

Practical Steps You Can Take This Month

- Review your latest mortgage statement carefully

- Gather insurance quotes from multiple providers

- Check eligibility for property tax relief programs

- Build or review your housing emergency fund

- Explore energy efficiency upgrades that might lower costs

- Discuss the changes openly with your family or partner

Small, consistent actions prevent feeling overwhelmed by larger adjustments. Start where you are with what you have available right now.

Remember that knowledge itself serves as a powerful tool. By understanding why your payment changed, you regain some control in a situation that might otherwise feel completely external.

Finding Opportunity Amidst the Challenges

While nobody enjoys higher housing costs, these moments can spark creativity. Some homeowners invest in skills like basic maintenance to reduce future expenses. Others reconsider their space needs and explore downsizing options that better fit current realities. A few discover that renting out a portion of their property creates helpful income streams.

The key lies in staying curious rather than defeated. Ask questions. Explore options. Connect with others facing similar situations. The shared experience often reveals solutions you wouldn’t have considered alone.

In my view, homeownership still offers tremendous value despite these hurdles. The sense of security, ability to customize your living space, and potential for building equity continue motivating many people. Navigating the costs successfully just requires more awareness than previous generations needed.

Preparing for Future Adjustments

Since costs rarely move in straight lines, plan on seeing periodic reviews and possible adjustments. Build this expectation into your annual budgeting process. Set aside a little extra each month specifically for potential escrow changes. That buffer reduces the emotional impact when adjustments arrive.

Technology also helps modern homeowners track these expenses better than ever. Apps that connect with your accounts can flag unusual patterns early. Some mortgage servicers now offer more transparent portals showing exactly where escrow money goes.

Use these tools to your advantage. The more visibility you have, the better equipped you become to make informed decisions about your largest monthly expense.

Transparency in financial matters always leads to better outcomes for families.

That principle applies especially well to something as significant as your home payment.

As we move through this period of higher costs, staying informed and proactive will serve you well. Your home represents more than just shelter. It stands as a central piece of your financial life and future security. By understanding the forces affecting your mortgage payment, you position yourself to protect that investment thoughtfully.

The coming months and years will likely bring more changes across the housing landscape. Those who adapt wisely, maintain realistic expectations, and take consistent action will navigate these waters most successfully. Your fixed-rate mortgage still provides valuable stability. The escrow adjustments simply remind us that homeownership involves multiple moving pieces requiring ongoing attention.

Take a deep breath if your payment just increased. You’re facing a common challenge right now, but with the right approach, you can manage it effectively while still enjoying the benefits of owning your home. The key is information, preparation, and a willingness to adjust course when needed.

What steps will you take first to address your own situation? Small decisions today can create significant relief over time. You’ve got this.