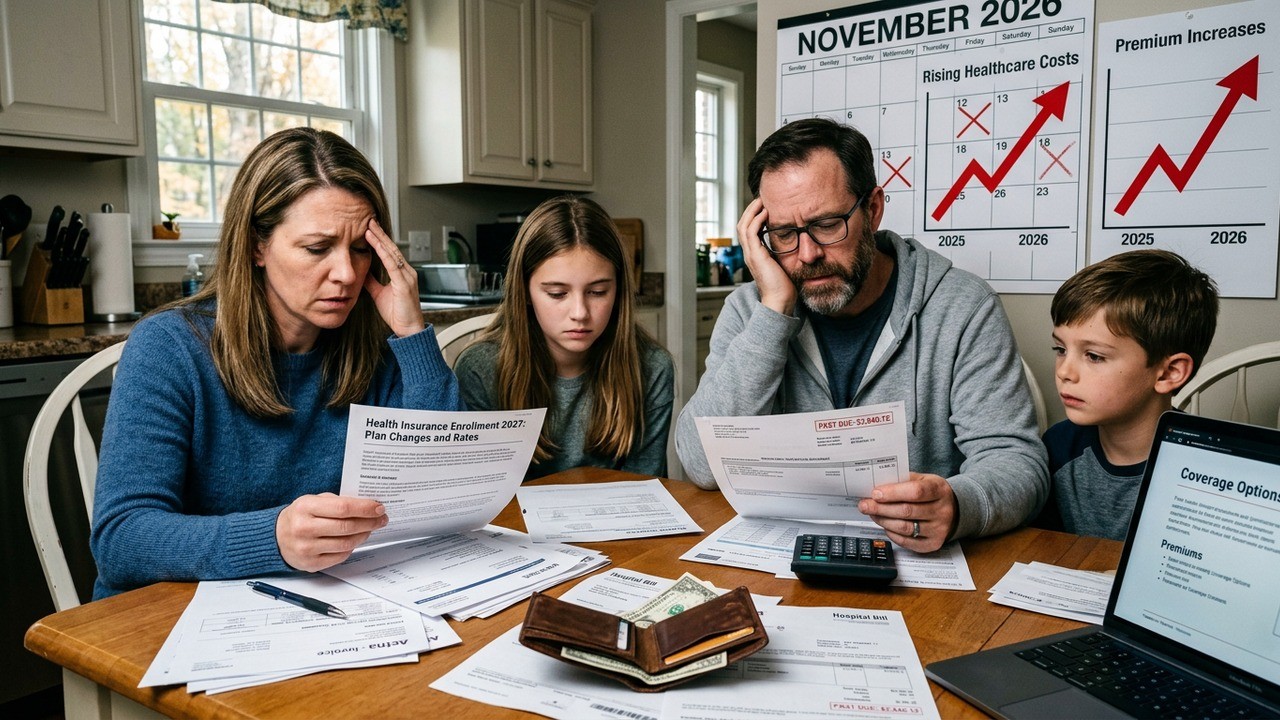

Have you ever opened your health insurance renewal notice and felt your stomach drop at the new monthly premium? For millions of Americans relying on the Affordable Care Act marketplace, that shock is hitting hard right now. What was once made more manageable through extra federal help has suddenly become a lot more expensive, and the ripple effects could be massive.

As we move through 2026, fresh analysis suggests that enrollment in these plans might tumble by around 5 million people compared to last year. That’s not just a number on a spreadsheet. It represents real families, freelancers, early retirees, and small business owners who are being forced to make tough decisions about protecting their health.

The End of Enhanced Support Changes Everything

When those extra premium subsidies expired at the end of 2025, it didn’t just tweak the system. It fundamentally altered the economics for a huge portion of the people who depend on marketplace coverage. What many hoped would be a temporary bridge after the pandemic years has now ended, leaving folks to shoulder much more of the load themselves.

In my view, this shift highlights how delicate the balance is between government assistance and personal responsibility in healthcare. One year you’re paying what feels reasonable, and the next, the same plan costs nearly double. It’s the kind of change that forces people to rethink their entire budget.

Understanding the Scale of the Drop

Projections indicate marketplace enrollment could settle around 17.5 million this year, down from 22.3 million in 2025. That’s a drop of more than 20 percent. While some people managed to sign up during open enrollment, a significant chunk are expected to drop coverage later in the year when the bills become too much to handle.

This isn’t happening in a vacuum. Healthcare costs have been climbing for years, but the lapse of enhanced subsidies has accelerated the pressure dramatically. Many households that were previously shielded from the full sticker price are now feeling every dollar of the increase.

The steepest single-year drop in raw numbers since the ACA Marketplaces launched.

Those words from policy researchers capture the moment perfectly. It’s not just a slow decline we’re seeing, but something sharper and more immediate.

Why Premiums Jumped So Much

Before the subsidies ended, many people paid relatively low amounts each month thanks to the extra federal support. Now, without that help, the average premium has climbed significantly. Initial estimates suggested increases as high as 114 percent if everyone stayed in the exact same plan, though real-world behavior softened that blow somewhat.

People adapted by shopping around and choosing different options. The reported average monthly premium rose to about $178 from $113 previously. Still a hefty 58 percent jump that stings for budgets already stretched thin. I’ve talked to enough people in similar situations to know that even a $50 or $60 monthly increase can push some families over the edge.

- Many switched to plans with lower monthly premiums but higher deductibles

- Households facing the biggest increases were more likely to drop coverage entirely

- Bronze plans saw a noticeable uptick in popularity

This last point matters a lot. Bronze plans are the most basic option, cheaper upfront but leaving you responsible for a larger share of costs if you need care. Enrollment in these plans jumped from 7.3 million to 9.2 million. It’s a clear sign that people are prioritizing affordability today over comprehensive protection tomorrow.

Deductibles Climb to Record Levels

Along with higher premiums comes another painful reality: bigger deductibles. The average across all plans increased by 37 percent to roughly $3,786. That’s the steepest jump on record. For a family dealing with an unexpected medical issue, that number can feel insurmountable.

Imagine needing to come up with nearly four thousand dollars before your insurance really kicks in. For many middle-class households, especially those without substantial savings, this changes how they approach healthcare. Do you delay that doctor’s visit? Skip the specialist? Hope nothing serious happens?

These aren’t abstract policy questions. They’re daily realities for people trying to do the right thing by staying insured.

Who Is Most Affected by These Changes?

The impact isn’t distributed evenly. Self-employed individuals, gig workers, and early retirees often rely heavily on the marketplace because they don’t have employer-sponsored coverage. These groups tend to have more variable incomes, making sudden premium hikes especially disruptive.

Younger adults sometimes feel healthy enough to go without insurance, even if that’s a risky bet. Older pre-Medicare adults might struggle more with the higher costs relative to their fixed incomes. Rural residents with fewer plan options can face even starker choices.

I’ve always believed that healthcare access shouldn’t be this stressful. When the system pushes people toward going uninsured, we all pay the price eventually through higher uncompensated care costs and worse health outcomes.

How People Are Responding in Real Time

During open enrollment for 2026, about 23 million signed up initially. That’s still a decline of 1.5 million from the previous year. But the real test comes as monthly payments continue throughout the year. Many who enrolled optimistically may find themselves unable to sustain the payments when other bills compete for their limited dollars.

Switching to higher-deductible plans is one common strategy. Others are looking for any available subsidies based on their current income, though the enhanced versions are gone. Some are exploring short-term plans or other alternatives, even if they come with less protection.

- Review all available plans carefully during open enrollment periods

- Calculate total potential costs including deductibles and out-of-pocket maximums

- Consider income changes that might qualify you for different subsidy levels

- Explore whether employer coverage or other options became available

These steps sound straightforward, but they require time, attention, and sometimes a level of financial literacy that not everyone has readily available. The complexity of the system itself becomes another barrier.

Broader Economic and Political Context

Healthcare affordability consistently ranks as one of the top concerns for American households. With premiums rising and deductibles climbing, this issue takes on even more weight. It affects everything from retirement planning to job choices to family stability.

Politically, the topic remains charged. Different approaches have been proposed, from direct payments to health savings account deposits, but finding common ground has proven difficult. The result is that millions are left navigating the current reality as best they can.

Households have cited health costs as a top financial concern.

This observation from recent reporting underscores why this matters beyond just insurance statistics. When healthcare costs squeeze family budgets, it reduces spending elsewhere in the economy and creates stress that touches every part of life.

What Bronze Plans Really Mean for Consumers

The surge in bronze plan selection tells an important story. These plans feature the lowest monthly premiums but require you to pay 40 percent of covered healthcare costs after the deductible. They’re designed for people who want basic protection against catastrophes but are willing to handle routine costs themselves.

While they can make insurance seem affordable on paper, the reality is that a serious medical event could still lead to substantial bills. It’s a trade-off that more people are making this year out of necessity rather than preference. I worry that some may underestimate how quickly those higher out-of-pocket costs can add up.

| Plan Type | Monthly Premium Trend | Deductible Impact | Who Chooses It |

| Bronze | Lowest | Highest | Cost-sensitive buyers |

| Silver | Moderate | Moderate | Balanced approach |

| Gold/Platinum | Higher | Lower | Those who can afford it |

This simplified view shows the spectrum of choices people face. The shift toward bronze plans reflects the pressure to minimize immediate spending even at the risk of higher costs later.

Longer-Term Implications for Healthcare Access

If enrollment does fall as projected, we could see several concerning trends develop. Uninsured rates might rise, particularly among working-age adults who don’t qualify for other public programs. This could lead to delayed care, worsening chronic conditions, and increased emergency room usage.

Hospitals and providers might face more uncompensated care, potentially driving costs higher for everyone with insurance. The individual market could become more expensive as healthier people drop out, leaving a sicker risk pool. These feedback loops are well-understood in health policy but difficult to interrupt once started.

On a personal level, I’ve seen how losing or struggling with insurance coverage creates anxiety that extends far beyond medical bills. It affects mental health, job performance, and family dynamics. No one should have to choose between groceries and prescriptions.

Practical Steps for Those Facing Higher Costs

While the big picture can feel overwhelming, there are actions individuals can take. First, thoroughly review your plan during any available enrollment windows. Compare total estimated costs, not just the premium. Factor in your expected healthcare usage for the year.

Consider whether your income level might still qualify for some assistance. Even without the enhanced subsidies, basic premium tax credits remain available for many. Small changes in reported income or household circumstances can sometimes make a difference.

- Build or maintain an emergency fund specifically for medical costs

- Explore flexible spending accounts or health savings accounts if eligible

- Research prescription assistance programs and generic options

- Look into telemedicine and preventive care services that might lower overall costs

- Discuss options openly with your healthcare providers about payment plans

These aren’t perfect solutions, but they can help stretch limited resources further. Knowledge and proactive planning remain your best tools in a challenging environment.

The Human Stories Behind the Numbers

Behind every statistic is a person or family making difficult choices. The freelance graphic designer who switched to a bronze plan and now worries about a potential surgery. The couple in their late 50s trying to bridge to Medicare while watching their premiums eat into retirement savings. The single parent calculating whether to keep coverage for themselves or prioritize the kids.

These stories remind us that policy decisions have very real human consequences. When we talk about 5 million fewer enrolled, we’re talking about millions of individual decisions driven by financial necessity. Some will remain uninsured and hope for the best. Others will cut back in other areas of life to maintain coverage.

Perhaps the most frustrating aspect is how unpredictable medical needs can be. You might go years without major issues, making the high deductible seem like a smart choice. Then one accident or diagnosis changes everything overnight.

Looking Ahead to Potential Solutions

While the current situation presents real challenges, it also creates opportunities for fresh thinking. Some advocate for more targeted assistance based on income or specific needs. Others suggest structural reforms to bring down underlying healthcare costs rather than just subsidizing premiums.

Innovations in care delivery, price transparency efforts, and competition could all play roles in making the system more sustainable. However, meaningful change typically moves slowly, leaving many to navigate today’s realities as best they can.

I remain cautiously optimistic that awareness of these issues will eventually drive better outcomes. When enough people feel the pinch, pressure builds for solutions. The key is ensuring that the conversation stays focused on practical results rather than political point-scoring.

Staying Informed and Prepared

In times of change like this, information becomes incredibly valuable. Understanding your options, knowing when enrollment periods occur, and tracking how policy shifts might affect you personally can help you make better decisions. Don’t wait until renewal time to start researching.

Communities, employers, and local organizations sometimes offer resources or group discussions that can make the process less isolating. Sharing experiences with others in similar situations often reveals strategies you might not have considered.

Ultimately, protecting your health and financial wellbeing requires vigilance. The ACA marketplace remains an important option for many, even with its current challenges. Learning to navigate it effectively has never been more important.

As this year unfolds, we’ll get clearer data on how many people ultimately maintain coverage and how the system adapts. For now, the message is clear: costs are up, choices are harder, and planning is essential. The 5 million enrollment drop projection serves as both a warning and a call to action for individuals and policymakers alike.

Have you felt the impact of these changes in your own household? Many are in the same boat, trying to balance quality coverage with what their budget can realistically handle. The coming months will reveal how this story develops, but one thing is certain – healthcare affordability will remain a central concern for American families well into the future.

By staying informed, exploring all available options, and planning ahead where possible, you can better position yourself and your loved ones to weather these shifts. The system may not be perfect, but understanding its current state is the first step toward making the best decisions possible in 2026 and beyond.