Have you ever wondered what happens when cutting-edge technology collides with established industry giants? The telecom world is buzzing right now, and not necessarily in a good way for some of the big names we’ve relied on for years. As SpaceX prepares to make its public debut on the stock market, traditional broadband providers are feeling the heat from an ambitious satellite-based internet service that’s gaining serious momentum.

It’s a fascinating shift that’s got investors rethinking their positions. Just recently, one major investment firm took a closer look at the competitive landscape and decided it was time to adjust expectations for a telecom heavyweight. This isn’t just another minor market adjustment – it signals deeper changes that could reshape how we access the internet in the years ahead.

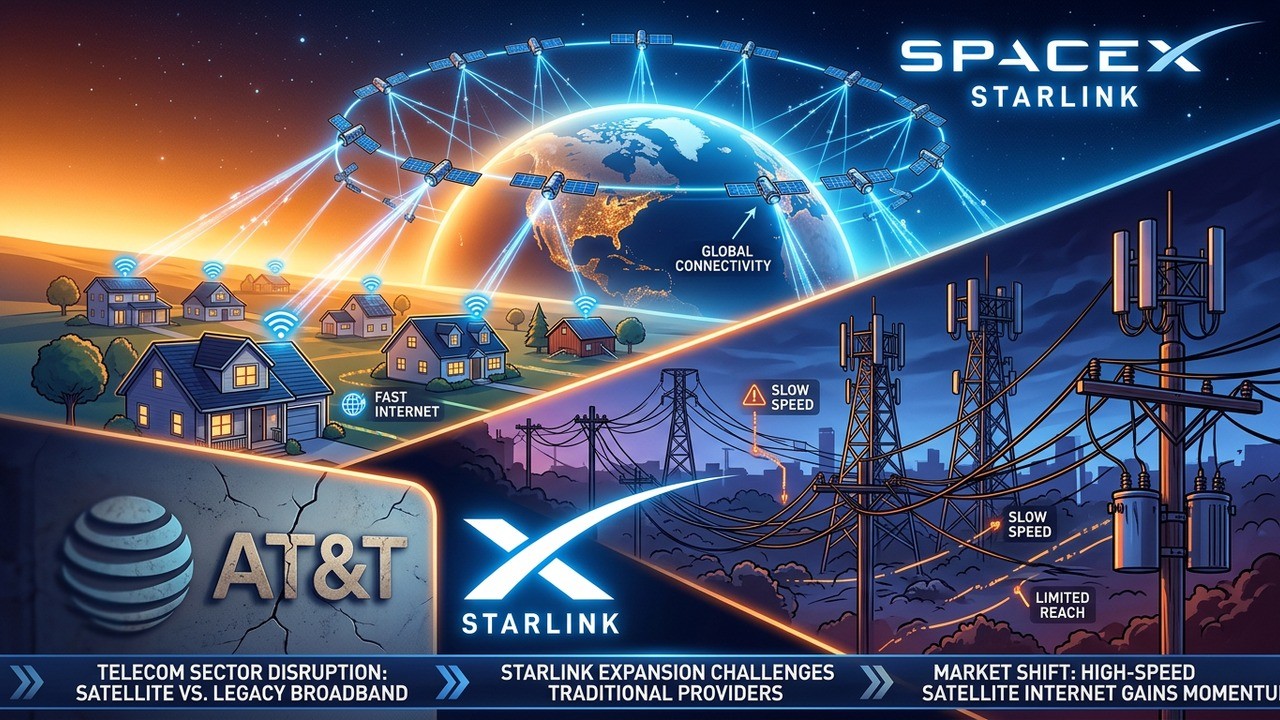

The Satellite Revolution That’s Changing Everything

Low-Earth orbit satellites have moved from science fiction to practical reality faster than most people anticipated. Companies are launching thousands of these small satellites that promise high-speed internet with surprisingly low latency. For people in remote areas or those frustrated with traditional cable and fiber limitations, this technology feels like a genuine breakthrough.

What makes this moment particularly interesting is the regulatory environment. Recent decisions by communications authorities have opened doors for expanded spectrum use, potentially multiplying the capacity of satellite systems. This isn’t happening in isolation – it’s part of a broader push toward more innovative connectivity solutions that could benefit consumers but challenge legacy infrastructure players.

In my view, we’ve reached a tipping point where the old ways of delivering broadband are going to face real tests. The convenience and expanding coverage of satellite options could attract customers who previously had few alternatives. But even in established markets, the pressure is building.

Why AT&T Finds Itself in the Crosshairs

AT&T has built an impressive network over decades, investing heavily in fiber optics and wireless infrastructure. Yet analysts are now highlighting vulnerabilities. With less diversified exposure compared to some peers, the company appears more exposed to shifts in the broadband space. Verizon and T-Mobile, for instance, have different mixes of business that might cushion potential blows.

The downgrade from a prominent bank wasn’t based on current performance alone. Instead, it reflects forward-looking concerns about subscriber growth. As satellite services improve and prices potentially become more competitive, traditional fixed broadband could lose ground. This isn’t an overnight collapse, but a gradual erosion that smart investors need to consider.

We think longer-term broadband subscriber growth and eventually mobile is at risk from rising threat of satellite constellations.

– Investment analyst perspective

That sentiment captures the mood among some market watchers. It’s not about today’s numbers but tomorrow’s possibilities. Space-based internet providers are positioning themselves to deliver not just broadband but also direct-to-device communications, which could extend their reach into mobile territories traditionally dominated by cellular networks.

Understanding the SpaceX Factor

SpaceX isn’t just another player – it’s a company that’s redefined space access with reusable rockets and massive satellite deployments. Their Starlink service has already connected users in places where laying cables was economically unfeasible. With an IPO reportedly targeting a lofty valuation, the public markets will soon have a direct way to bet on this vision.

Reports suggest the company aims for a significant share price that reflects enormous confidence in its future. This public listing could bring more scrutiny but also additional capital to accelerate deployments. For competitors, the visibility alone serves as a wake-up call about the seriousness of the threat.

- Rapid constellation expansion increasing coverage areas

- Improving latency making satellite viable for more applications

- Potential for direct integration with consumer devices

- Growing partnerships and regulatory approvals worldwide

These elements combine to create a formidable challenge. While early versions of satellite internet had drawbacks like higher costs and weather sensitivity, iterative improvements are addressing many of these issues. Consumers are noticing, and adoption rates in certain segments are climbing.

Short-Term Resilience Meets Long-Term Concerns

It’s important to maintain perspective. Traditional broadband providers aren’t going to disappear tomorrow. Cable and fiber still offer advantages in densely populated areas where infrastructure is already in place. Pricing for satellite services remains a factor that keeps many customers with established options for now.

However, the trajectory is what matters for investors. If new fiber construction slows as predicted by some analysts, the entire supply chain supporting traditional builds could face headwinds. Equipment makers, installers, and related businesses might all feel the effects over time.

I’ve followed these markets for quite a while, and one pattern stands out: technology disruptions rarely follow linear paths. They accelerate once critical mass is reached. We’re potentially approaching that inflection point with satellite broadband.

Breaking Down the Competitive Dynamics

Let’s examine what makes satellite constellations particularly disruptive. Unlike fixed infrastructure that requires massive upfront capital for physical networks, satellites can scale coverage by launching more units. This flexibility allows faster expansion into new territories without proportional ground costs.

| Technology Type | Deployment Speed | Geographic Reach | Upfront Cost |

| Satellite LEO | High | Global | Medium-High |

| Fiber Optic | Low | Urban Focused | Very High |

| Fixed Wireless | Medium | Suburban/Rural | Medium |

This comparison illustrates why excitement around space-based solutions continues to build. Of course, each approach has trade-offs, but the momentum clearly favors innovation in orbit.

Investor Implications and Market Reactions

AT&T shares have shown some weakness in recent months, trailing broader market performance. This downgrade adds to the narrative of caution. Yet markets are forward-looking, and savvy investors will look beyond immediate headlines to assess true long-term value.

Diversification becomes key here. Companies with strong wireless businesses or international exposure might navigate these waters differently. Meanwhile, pure-play broadband providers face tougher questions about adaptation strategies.

Operators are expanding connectivity through innovative means that were unimaginable just years ago.

– Communications policy observation

Regulatory support for satellite services reflects a desire to bridge digital divides. This public policy angle could accelerate adoption and create additional tailwinds for new entrants. For established telcos, the challenge lies in evolving their offerings or finding complementary roles in the ecosystem.

Technological Advancements Driving the Change

The engineering behind modern satellite internet deserves appreciation. Phased array antennas, advanced signal processing, and inter-satellite laser links all contribute to performance that rivals or exceeds older systems in many scenarios. Latency has dropped dramatically, making everything from video calls to online gaming more feasible.

Future iterations promise even better capabilities. As manufacturing scales and launch costs continue declining, the economics improve. This virtuous cycle of innovation and cost reduction is what keeps analysts up at night when evaluating traditional telecom investments.

- Initial deployment focused on underserved regions

- Performance improvements attracting urban customers

- Integration with mobile devices expanding use cases

- Potential enterprise applications adding revenue streams

Each step builds on the last, creating network effects that are difficult for slower-moving competitors to match. It’s a classic case of disruptive innovation playing out in real time.

What This Means for Consumers

Beyond Wall Street, everyday users stand to gain from increased competition. More options often translate to better service and potentially lower prices over time. Rural communities particularly benefit as satellite coverage fills gaps that fiber economics could never justify.

Yet challenges remain. Data caps, installation requirements, and reliability during extreme weather are factors consumers must weigh. The ideal outcome would be a healthy mix of technologies coexisting and complementing each other based on specific needs and locations.

Perhaps the most interesting aspect is how this forces all providers to innovate. Complacency isn’t an option when customers have viable alternatives appearing on the horizon.

Risk Management for Telecom Investors

For those holding telecom stocks, this development calls for careful portfolio review. Assessing exposure to broadband revenues versus wireless or enterprise services can highlight relative strengths. Companies actively experimenting with their own satellite partnerships or hybrid solutions might fare better.

It’s also worth considering the broader investment thesis. Demand for connectivity continues growing with remote work, streaming, and IoT applications. The pie is expanding even as the slicing method changes.

Key Factors to Watch: - Satellite adoption rates in key markets - Regulatory developments on spectrum - Pricing trends across technologies - Infrastructure investment announcements

Monitoring these indicators can provide early signals about the pace of disruption. Patient investors might find opportunities in both established players adapting successfully and newer entrants proving their models.

Broader Industry Transformations

This isn’t isolated to one company or even one sector. The entire communications industry is evolving with 5G, edge computing, and now orbital infrastructure playing larger roles. Convergence of technologies creates both threats and synergies that smart businesses can leverage.

SpaceX’s success could inspire more competition in the satellite space too, further accelerating progress. Multiple constellations operating could enhance redundancy and capacity while driving down costs through rivalry.

From an investment standpoint, it’s reminiscent of previous tech cycles where early movers captured significant value. Timing and execution will determine winners and losers as the market matures.

Preparing for an Uncertain Future

No one has a crystal ball, but the signals suggest increased volatility in telecom valuations as satellite stories gain traction. The upcoming IPO will likely amplify media attention and market awareness, potentially affecting sentiment across the sector.

Companies that communicate clear adaptation strategies – whether through partnerships, technology upgrades, or service differentiation – may reassure investors. Those appearing reactive could face continued pressure.

In my experience analyzing market shifts, the most successful players are those who embrace change rather than resist it. The broadband wars are entering a new chapter, and adaptability will be crucial.

Looking Ahead: Opportunities and Challenges

As we move forward, several scenarios could unfold. Optimistic views see satellite technology complementing existing networks, creating a more robust overall infrastructure. Pessimistic takes warn of significant market share losses for traditional providers unable to pivot quickly enough.

Reality will likely land somewhere in between, varying by geography and use case. Urban centers might stick with high-capacity fiber while rural and suburban areas embrace satellites. Mobile services could see hybrid approaches emerge.

- Potential for new revenue streams in space-based services

- Need for substantial R&D investment to stay competitive

- Regulatory uncertainty remaining a key variable

- Consumer behavior shifts as options multiply

Each of these elements adds layers of complexity to investment decisions. Thorough research and diversified holdings help manage risks in such dynamic environments.

The excitement around SpaceX’s public offering reflects broader enthusiasm for space economy growth. From internet access to potential future applications, the implications extend far beyond today’s headlines. For telecom investors specifically, vigilance and flexibility will serve well as the competitive landscape continues evolving.

While challenges are clear for companies like AT&T, they also possess significant assets – established customer bases, spectrum holdings, and operational expertise that could prove valuable in a multi-technology world. The coming years will test their ability to innovate and defend market positions against nimble, well-funded newcomers.

Ultimately, this story reminds us that markets reward foresight. Those who recognized the potential of satellite constellations early are positioning accordingly. For everyone else, the recent analyst moves serve as timely prompts to reevaluate assumptions about the future of connectivity.

The broadband battle is heating up, and with a major IPO on the horizon, expect more attention and volatility. Smart observers will watch closely as technology, regulation, and consumer preferences interact to shape the next era of internet access. The opportunities are there for those willing to navigate the complexities.

Expanding on these themes further, consider how global events influence technology adoption. Supply chain improvements, international partnerships, and even geopolitical factors play roles in how quickly satellite networks can scale. Companies with strong execution capabilities across borders may hold advantages.

Additionally, environmental considerations are entering the conversation. While satellites reduce the need for extensive ground infrastructure, concerns about space debris and launch emissions require responsible management. Firms addressing these responsibly could gain public and regulatory favor.

From a financial modeling perspective, analysts are adjusting growth projections, discount rates, and competitive moat assessments. This recalibration affects not just individual stocks but sector ETFs and related industries. The ripple effects are widespread.

It’s also worth noting that consumer education will play a part. Many people still associate satellite internet with outdated slow services. As real-world performance data spreads through reviews and word-of-mouth, perceptions are shifting positively for modern implementations.

Service bundles combining satellite with other offerings could emerge as winning strategies. Providers that make switching easy and deliver consistent quality will likely capture more market share. Loyalty programs and superior customer support remain timeless differentiators even in high-tech industries.

Taking a step back, this situation exemplifies creative destruction in action. Joseph Schumpeter’s concept feels particularly relevant as innovative space technology challenges century-old business models. Investors familiar with historical tech transitions know both fortunes were made and lost during such periods.

The key takeaway remains balancing enthusiasm for new technologies with realistic assessments of implementation challenges and timelines. Hype cycles can create short-term distortions while fundamental improvements drive long-term value.

As the IPO approaches, expect increased coverage and speculation. This spotlight could benefit the entire sector by raising awareness about connectivity’s future but might also amplify short-term stock movements based on sentiment rather than fundamentals.

Remaining grounded in data while staying open to paradigm shifts offers the best path forward. The telecom industry has reinvented itself before – from landlines to mobile, dial-up to broadband – and will likely do so again. Those who adapt thoughtfully stand the best chance of thriving.