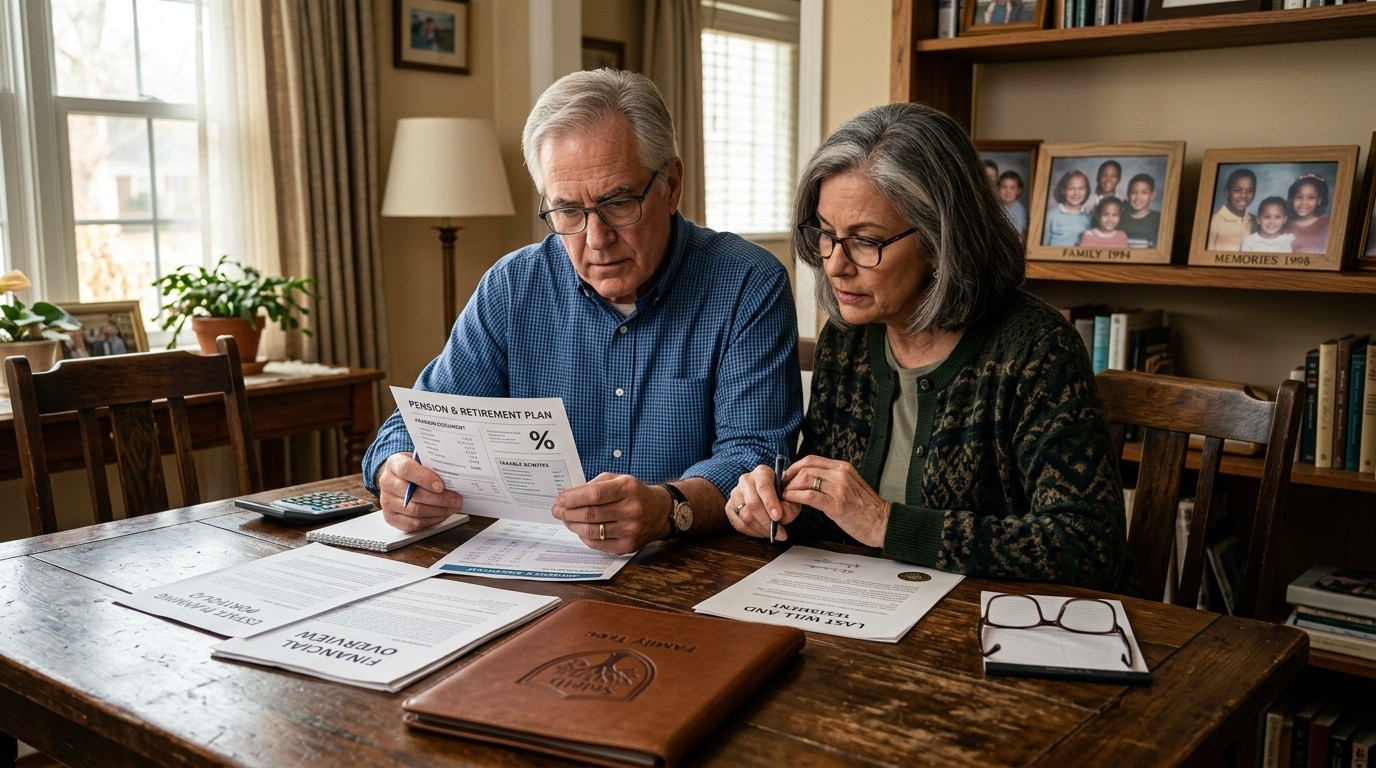

Picture this: you’ve found love again after years on your own. The kids are grown, life feels fresh, and everything seems to be falling into place. Yet beneath the surface of this new chapter lies a financial reality that catches many couples completely off guard. Remarrying later in life doesn’t just blend hearts and households – it can create complex inheritance situations that risk leaving your own children unintentionally sidelined.

I’ve spoken with enough people in this position to know how quickly joy can turn to worry when the topic of estate planning comes up. The numbers tell a striking story too. Marriage rates for those over 50 have climbed significantly, with even sharper increases for people in their sixties. This brings more blended families into the picture than ever before, each with their own unique set of financial hopes and concerns.

The Growing Reality of Blended Families in Later Life

When two people come together later in life, they often bring more than just their personal histories. Children from previous relationships, existing assets, and different expectations about the future all enter the mix. What feels like a beautiful new beginning can quietly set the stage for complications down the road, particularly around what happens to money and property when one partner passes away.

Blended families come in all shapes and sizes. Sometimes it’s his children and her children. Other times one partner has kids while the other doesn’t. The common thread is the need for thoughtful planning that respects everyone’s place in the family without creating unnecessary tension or financial hardship.

Why Inheritance Planning Matters More Than Ever in Second Marriages

Many couples focus so much on making their new relationship work that they put off discussing what happens after they’re gone. I get it – it’s not exactly romantic dinner conversation. But avoiding these talks doesn’t make the issues disappear. In fact, it often makes them more painful for those left behind.

Recent changes to tax rules have added new urgency to these conversations. Starting in 2027, certain pension pots will count toward your estate for inheritance tax purposes. This shift could pull many more families into the tax net than before. For those with children from earlier relationships, the stakes feel particularly high.

Think about it. You’ve worked hard to build up your pension over decades. You want your new spouse to feel secure, but you also want to make sure your own kids aren’t forgotten. Striking that balance requires more than good intentions.

Common Misconceptions That Create Problems

One of the biggest traps I’ve noticed is assuming that everything will automatically sort itself out. People often believe their spouse will naturally do the right thing and pass assets to the children from the first marriage. Sometimes that happens. Sometimes life changes – new relationships, health issues, or simply shifting priorities – lead to different outcomes.

Circumstances can change in ways we never expect, especially over many years.

Another misconception involves thinking that naming your spouse as beneficiary on everything protects the family. While it might avoid immediate tax hits, it hands over complete control. Your spouse could later redirect those assets in ways you didn’t anticipate.

Unmarried couples face even trickier situations since they lack some automatic legal protections that married partners enjoy. But even within marriage, assumptions about what “should” happen often don’t match reality.

The Pension Inheritance Tax Changes Explained

Let’s talk specifically about pensions because these upcoming rules are game-changers for many families. Defined contribution pensions will soon form part of your taxable estate. This means they could be subject to 40% inheritance tax above certain thresholds.

For couples where one or both partners have substantial pension savings, this creates both opportunities and risks. You might want your surviving spouse to benefit from that money during their lifetime. At the same time, you hope some of it eventually reaches your children from before.

The inter-spousal exemption offers real value here. Assets passing to a husband or wife usually avoid inheritance tax on the first death. This can preserve more wealth overall. But it depends heavily on the surviving partner following through with the original wishes later on.

Navigating the Nomination Minefield

Pension nominations require careful thought. These expressions of wish guide trustees but aren’t always binding. That flexibility can be both helpful and dangerous in blended family situations.

If you leave everything to your new spouse, they gain full control. They might face pressure from their own children or simply change their mind years down the line. On the flip side, naming your children directly could leave your spouse financially vulnerable if they need access to those funds.

- Consider what your spouse needs for their lifestyle and security

- Think about protecting assets for your children without creating immediate tax problems

- Balance immediate needs with long-term family wishes

In my experience, families that discuss these matters openly while everyone is healthy tend to reach better solutions. Emotions stay calmer and creative options emerge more easily.

Trust Structures That Offer Real Protection

Trusts aren’t just for the ultra-wealthy. They serve as practical tools for controlling how assets pass between generations while providing for loved ones. Several types might suit blended families particularly well.

Life interest trusts, for example, let your spouse benefit from assets like property or investment income during their lifetime. The capital then passes to your chosen beneficiaries – often your children – afterward. This approach offers security without handing over full ownership.

Discretionary trusts give trustees flexibility to respond to changing family circumstances. They can distribute income or capital as needs arise while keeping assets protected from certain risks like divorce or creditors.

Spousal Bypass Trusts and Their Role Today

These arrangements used to be more common for tax planning. While their tax advantages have evolved, they still provide valuable control. A bypass trust can support your spouse without including the assets in their estate later on.

Some families now use them primarily for the peace of mind rather than pure tax savings. The ability to set clear rules about distributions helps prevent future family disputes.

Of course, no structure eliminates every risk. Life has a way of throwing curveballs – health challenges, new relationships, or simply changing priorities among beneficiaries.

Property Ownership and Family Homes

The family home often represents the largest single asset and the most emotional one. How you own property matters enormously. Tenants in common ownership allows each partner to specify what happens to their share in their will.

This setup makes it possible to create a life interest for your spouse while ensuring the property eventually benefits your children. Without proper ownership structure, assets might pass automatically outside your will entirely.

Practical Steps You Can Take Right Now

Don’t wait for the perfect moment to start planning. Begin with honest conversations. What does security look like for your spouse? How important is it to provide specifically for children from previous relationships? Where might compromises work best?

- Review all your existing wills and beneficiary nominations

- Gather details about pensions, properties, and other major assets

- Consult professionals who understand both legal and financial angles

- Document your wishes clearly while considering different scenarios

- Schedule regular reviews as life circumstances evolve

Professional advice proves invaluable here. Solicitors and financial planners can help craft solutions tailored to your specific family dynamics rather than generic approaches.

Real Family Scenarios and Solutions

Consider Michael, a widower with two adult sons who remarried Sarah, who has one daughter. His substantial pension represented years of careful saving. By using a life interest trust arrangement, he ensured Sarah could benefit from the income while directing the capital toward all three children eventually.

Or take Angela, who worried about her new husband’s children having claims on her property. Through careful will drafting and trust planning, she protected her own children’s inheritance while providing her husband a secure place to live.

These aren’t theoretical cases. They reflect real choices families face every day. The right structure depends on your values, relationships, and financial picture.

Addressing Care Costs and Changing Needs

One often-overlooked aspect involves potential long-term care expenses. Even the most well-intentioned surviving spouse might need to spend down assets for their own health needs. Planning should account for this possibility without leaving anyone vulnerable.

Some families build in provisions for care costs while protecting core inheritance. Others prioritize insurance options or other protective measures. The key lies in thinking through multiple possible futures rather than assuming the best case.

Communication Tips for Difficult Conversations

Bringing up inheritance with your new partner requires sensitivity. Frame it as protecting everyone rather than expressing distrust. Many couples find that discussing values first – what matters most about family and legacy – opens the door to practical solutions.

Involve adult children where appropriate. Transparency can prevent nasty surprises later. While not every detail needs sharing, the broad principles often benefit from open dialogue.

The families who tackle these topics together tend to experience less conflict when the time comes.

Pensions as More Than Just Retirement Savings

While pensions serve primarily to provide income in later life, they increasingly play a role in estate planning too. This dual purpose requires careful balancing. Drawing down pension assets strategically during your lifetime might reduce future tax exposure while still providing for your spouse.

However, don’t treat pensions solely as inheritance vehicles. Their main purpose remains supporting your own retirement. Smart planning considers both current needs and future legacy goals.

The Emotional Side of Financial Planning

Beyond the numbers and legal structures lies the human element. Feelings of loyalty to previous families, guilt about new relationships, and hopes for harmony all influence decisions. Acknowledging these emotions doesn’t make you weak – it makes your planning more realistic and compassionate.

I’ve seen families strengthen their bonds by facing these realities together. The process of planning can actually bring people closer when handled with care and respect.

Updating Plans as Life Changes

Life doesn’t stand still. New grandchildren, health diagnoses, marriages among children, or simply changing relationships all warrant reviews of your arrangements. What made perfect sense five years ago might need adjustment today.

Build regular reviews into your routine – perhaps every few years or after major life events. This keeps your plans aligned with current realities and family dynamics.

Finding the Right Balance for Your Family

Ultimately, there’s no one-size-fits-all solution. Every family has different priorities, relationships, and resources. Some emphasize equal treatment among all children. Others focus more on providing for the surviving spouse first.

The most successful approaches usually combine legal tools with open communication and regular check-ins. They respect the new marriage while honoring previous family commitments.

Remember that fairness doesn’t always mean equality. Different children might have different needs or have already received support at various life stages. Thinking in terms of overall family wellbeing often leads to better outcomes than strict mathematical splits.

Looking Ahead With Confidence

Remarrying brings wonderful opportunities for companionship and shared adventures. With thoughtful planning, you can protect that new relationship while safeguarding your broader family’s future. The investment in professional advice and careful documentation pays dividends in peace of mind.

Don’t let fear of difficult conversations prevent you from taking action. Most families find that addressing these matters actually reduces anxiety rather than creating it. Knowledge and preparation replace worry with confidence.

As you build this next chapter of your life, give yourself permission to plan for all the people you love. Your new partner and your children from before don’t have to compete for your care and attention. Smart structures make it possible to support everyone meaningfully.

The landscape continues evolving with tax changes and shifting family norms. Staying informed and adaptable serves your family best. Take that first step today – review your documents, start the conversation, and seek guidance from professionals who understand these nuanced situations.

Your legacy isn’t just about money. It’s about the love and security you provide for all your family members across different chapters of life. With care and forethought, you can navigate the potential minefields and create arrangements that reflect your true wishes and values.

I’ve watched too many families struggle with unintended consequences to stay silent on this topic. Taking time now to plan carefully can prevent heartaches later. Your future self – and all those you love – will thank you for it.

Planning for the future in a blended family requires patience, honesty, and often expert help. But the reward is knowing you’ve done your best to protect everyone important to you, no matter what tomorrow brings.