Have you ever watched two completely different stories unfold at the same time and wondered how they could possibly connect? That’s exactly what’s happening in global finance right now. While equity markets cling to optimism and push toward fresh records, the bond market is whispering warnings about sticky inflation and longer-term risks. Add in some surprising diplomatic developments in the Middle East, and you’ve got a recipe for genuine uncertainty that could shape investment decisions for the rest of the year and beyond.

I’ve been following these crosscurrents closely, and what strikes me most is how the usual rules seem to be bending. Risk assets refuse to blink, yet fixed income investors are clearly repositioning for a bumpier road. It’s a classic case of markets trying to price in multiple futures at once, and that tension rarely lasts forever without some resolution – or volatility.

The Delicate Balance Between Diplomacy and Markets

Recent high-level discussions between American and Iranian officials in a neutral European location have injected a note of cautious optimism into energy markets. Both sides reportedly made enough headway to outline a 60-day roadmap toward a broader agreement. Key talking points included stabilizing shipping lanes critical for global oil transport and easing tensions in surrounding conflict zones.

Of course, diplomacy moves at its own pace, and plenty of thorny issues remain. Still, the mere fact that technical teams are staying engaged and a joint oversight committee has been mentioned suggests both parties see value in continued dialogue. In my experience, these kinds of incremental steps can sometimes create more breathing room for markets than dramatic breakthroughs.

The path forward remains uncertain, but any reduction in geopolitical friction around key energy chokepoints could ease some of the upward pressure on prices we’ve seen lately.

Even so, traders aren’t popping the champagne just yet. History shows that Middle East negotiations can shift quickly, and markets have learned to price in a healthy dose of skepticism until concrete actions replace promises.

How Geopolitics Feeds Into Energy Markets

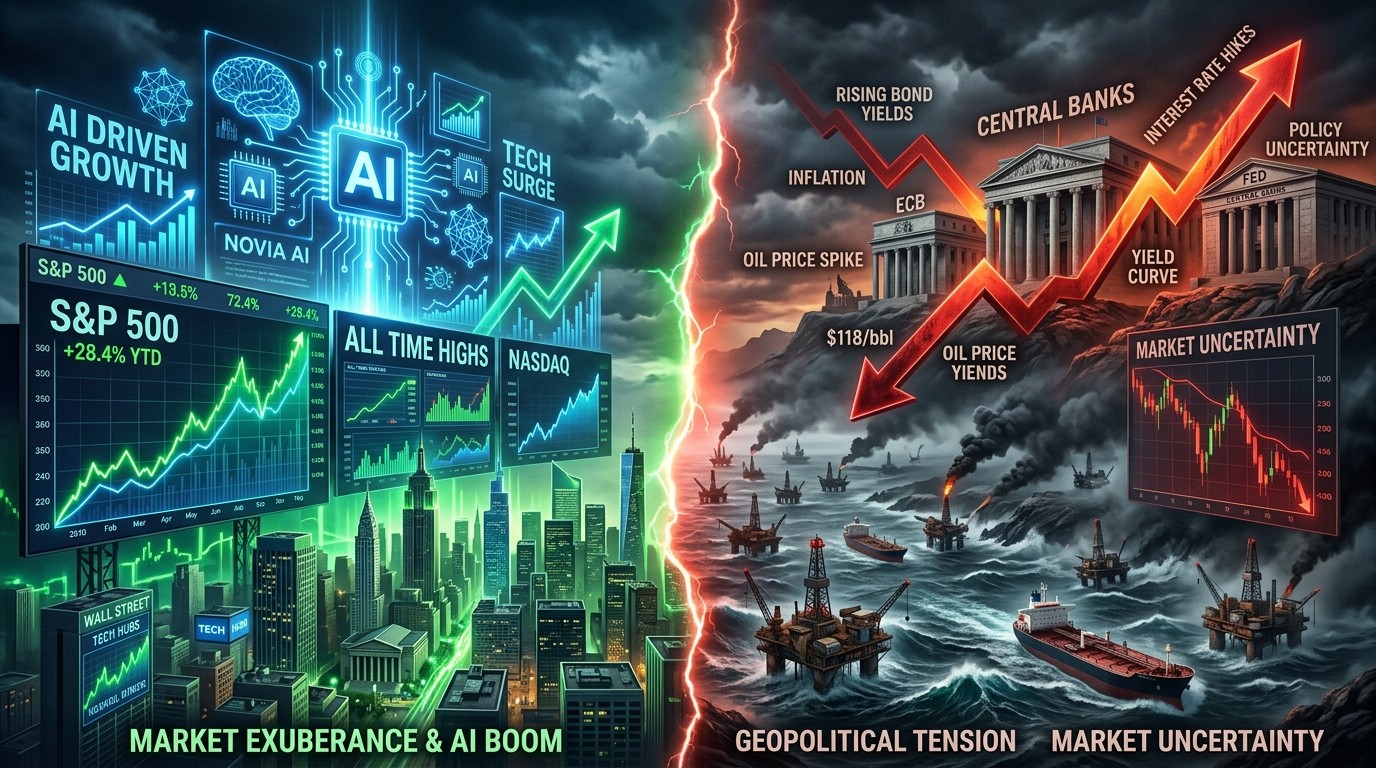

Energy has been the wildcard this year. Disruptions to vital shipping routes earlier triggered a meaningful spike in oil prices and drew down global inventories faster than many analysts expected. Transportation costs climbed, feeding into everything from grocery bills to manufacturing inputs. This isn’t just an isolated event – it’s a textbook supply shock rippling through the entire economy.

What makes this situation particularly tricky is the dual impact: higher prices stoke inflation while simultaneously weighing on demand. Projections now suggest global oil consumption could actually decline next year under certain scenarios. That’s the kind of environment where central bankers lose sleep.

- Higher fuel costs passing through to consumer prices

- Businesses facing margin pressure and potential cutbacks

- Households trimming discretionary spending as real incomes take a hit

I’ve seen similar dynamics play out before, and they rarely resolve cleanly. The hope now is that successful talks could gradually restore more normal flows, but even in the best case it will likely take months for production and logistics to normalize fully.

Central Banks Chart Different Courses

The world’s major central banks are responding to these pressures in notably different ways. The Federal Reserve held rates steady at their latest meeting and dropped earlier hints of an easing bias. Officials highlighted resilient economic activity alongside inflation that remains stubbornly above target. Their updated forecasts show core measures likely staying elevated well into 2026.

Market participants now price in a more gradual path for rate reductions, perhaps a couple of cuts mid-next year if conditions cooperate. This more patient stance reflects recognition that supply-side factors, particularly energy, are playing an outsized role right now.

We expect the data-dependent approach to continue, with officials ready to adjust based on how inflation and growth actually evolve rather than pre-committing to a specific path.

Across the Atlantic, the picture looks quite different. European policymakers have already moved back toward tightening, delivering a rate hike earlier in the month. They too pointed to energy-driven inflation pressures but paired that with downward revisions to growth expectations. The result is a classic stagflationary dilemma that leaves limited good options on the table.

This policy divergence matters for currencies, capital flows, and relative asset performance. A stronger euro in the near term isn’t out of the question, but Europe’s greater sensitivity to energy costs could cap any sustained appreciation.

Equities Defy the Headlines

Despite the macro crosswinds, major stock indices – particularly in the US – have displayed impressive resilience. Corporate earnings have generally held up well, supported by pricing power and continued heavy investment in transformative technologies like artificial intelligence. The narrative around AI remains a powerful tailwind for select sectors and companies.

Yet this strength deserves some scrutiny. Valuations sit at elevated levels by many traditional measures, and the market seems to be discounting a relatively soft landing scenario even as risks around inflation and geopolitics linger. Perhaps the most interesting aspect is how investors continue to reward growth stories while largely shrugging off near-term macroeconomic noise.

That said, I wouldn’t be surprised to see periods of heightened volatility ahead. When bonds and stocks diverge this sharply, it often signals underlying doubts that eventually need to be reconciled.

| Asset Class | Current Signal | Key Driver |

| Equities | Resilient / Bullish | Corporate earnings and AI narrative |

| Bonds | Cautious / Higher yields | Inflation expectations and term premia |

| Commodities | Geopolitically sensitive | Energy supply disruptions |

The Bond Market’s Cautionary Tale

Long-term government bond yields have climbed to levels not regularly seen in nearly two decades. This move reflects several intertwined factors: elevated inflation expectations tied to energy costs, higher term premia due to geopolitical uncertainty, and a reassessment of how aggressively central banks will ultimately respond.

The message from fixed income seems clear – inflation risks remain tilted to the upside, and policy rates may need to stay higher for longer than many hoped just a few quarters ago. This environment challenges traditional portfolio construction, particularly for strategies relying heavily on duration.

I’ve always believed that when bonds and stocks tell different stories, it’s worth paying extra attention to the bond market. It tends to be more attuned to macro risks over the medium term.

Broader Economic Implications

The combination of higher energy costs and restrictive financial conditions creates a challenging backdrop for growth. Businesses face rising input costs while consumers pull back on spending. This dynamic can feed into slower expansion, potentially pressuring corporate margins if pricing power eventually wanes.

On the positive side, strong labor markets in several major economies have so far prevented a sharp downturn. Wage growth, while contributing to service sector inflation, also supports household incomes in the face of higher prices for necessities.

- Monitor upcoming inflation prints for signs of second-round effects

- Watch corporate earnings guidance for any shifts in outlook

- Track diplomatic developments for their impact on oil supply forecasts

- Assess currency moves as policy divergence plays out

One area that deserves particular attention is the potential for feedback loops. If higher yields begin to tighten financial conditions more than expected, it could weigh on growth and eventually force central banks to reconsider their stance. Timing these shifts is never easy, but staying flexible remains crucial.

Investment Considerations in Uncertain Times

For investors, this environment calls for nuance rather than sweeping conclusions. Diversification across asset classes, regions, and sectors makes more sense than ever. Those with exposure to energy may benefit from near-term strength but should also consider the longer-term demand risks if global growth slows.

Quality companies with strong balance sheets and genuine pricing power could continue to outperform in a higher-for-longer rate world. At the same time, it’s wise to maintain some dry powder for potential opportunities if volatility spikes and creates mispricings.

The current setup rewards selectivity and patience more than aggressive positioning.

I’ve found over the years that the most successful approaches in mixed environments tend to balance conviction in structural themes – like technological transformation – with humility about near-term macro outcomes. AI’s potential remains compelling, but its realization will still occur against a real economic backdrop.

Political Shifts Add Another Layer

Recent leadership changes in major economies, including the surprise resignation of the UK’s prime minister, underscore the fluid nature of the political landscape. Such developments can influence fiscal policy, regulatory approaches, and market sentiment in unpredictable ways. While the immediate market reaction may be muted, the longer-term implications for growth and stability deserve monitoring.

Political instability tends to amplify existing economic vulnerabilities. In an already complex global environment, these domestic shifts could complicate coordinated international responses to shared challenges like energy security and inflation.

What Could Shift the Narrative?

Several key variables will likely determine whether current market divergences resolve constructively or lead to sharper adjustments. First and foremost, progress on the diplomatic front could ease energy market strains and support a more benign inflation path. Conversely, any renewed disruptions would likely reinforce the hawkish tilt in bond markets.

Second, incoming economic data will be scrutinized for evidence of second-round inflation effects, particularly in wages and services. Clear signs here could prompt central banks to maintain restrictive settings even longer than currently anticipated.

Finally, the resilience of consumer and business spending will be critical. If growth holds up better than feared, equities may continue their run. A sharper slowdown, however, could trigger a broader reassessment across asset classes.

In my view, the most probable path involves gradual adjustment rather than dramatic resolution. Markets have proven remarkably adaptable, but that doesn’t mean the ride will be smooth. Staying informed and avoiding emotional decisions remains the best approach during periods like this.

Looking Further Ahead

As we move through the remainder of the year and into the next, the interplay between geopolitics, monetary policy, and technological innovation will continue to dominate. The energy transition, while facing short-term hurdles, retains its longer-term importance. Similarly, productivity gains from AI and related technologies could eventually help offset some of the structural challenges we face.

Yet none of these positive forces operate in a vacuum. Policy choices, international relations, and simple economic cycles all matter. Investors who can maintain a balanced perspective – acknowledging both risks and opportunities – stand the best chance of navigating successfully.

I’ve always believed that periods of elevated uncertainty ultimately create the conditions for stronger subsequent returns for those positioned thoughtfully. The key is avoiding the temptation to chase momentum at extremes or to hide completely from risk when fear dominates.

With so many moving pieces, disciplined analysis and a willingness to adapt will be essential. The divergence between markets today may not persist indefinitely, but understanding why it exists provides valuable clues about potential future directions.

Whether you’re managing personal investments or simply trying to make sense of the daily headlines, keeping these broader dynamics in mind can help cut through the noise. The coming months promise to be eventful, and those who approach them with clear eyes and flexible strategies may find meaningful opportunities amid the complexity.

One final thought: while the macro picture feels heavy at times, human ingenuity and market mechanisms have a way of finding solutions. The current environment tests that resilience, but it also highlights the importance of staying engaged rather than sitting on the sidelines. After all, the most rewarding investments often emerge from precisely these kinds of uncertain periods.