Have you noticed prices creeping up at the grocery store or at the gas pump lately? It feels like just when things were starting to stabilize, something shifted. Recent projections from leading economic voices suggest we’re in for a rougher ride with inflation than many expected even a few months ago.

The latest survey of professional forecasters paints a concerning picture for the months ahead. What started as modest expectations has now ballooned into something much more significant, largely due to geopolitical developments that few saw coming at the start of the year.

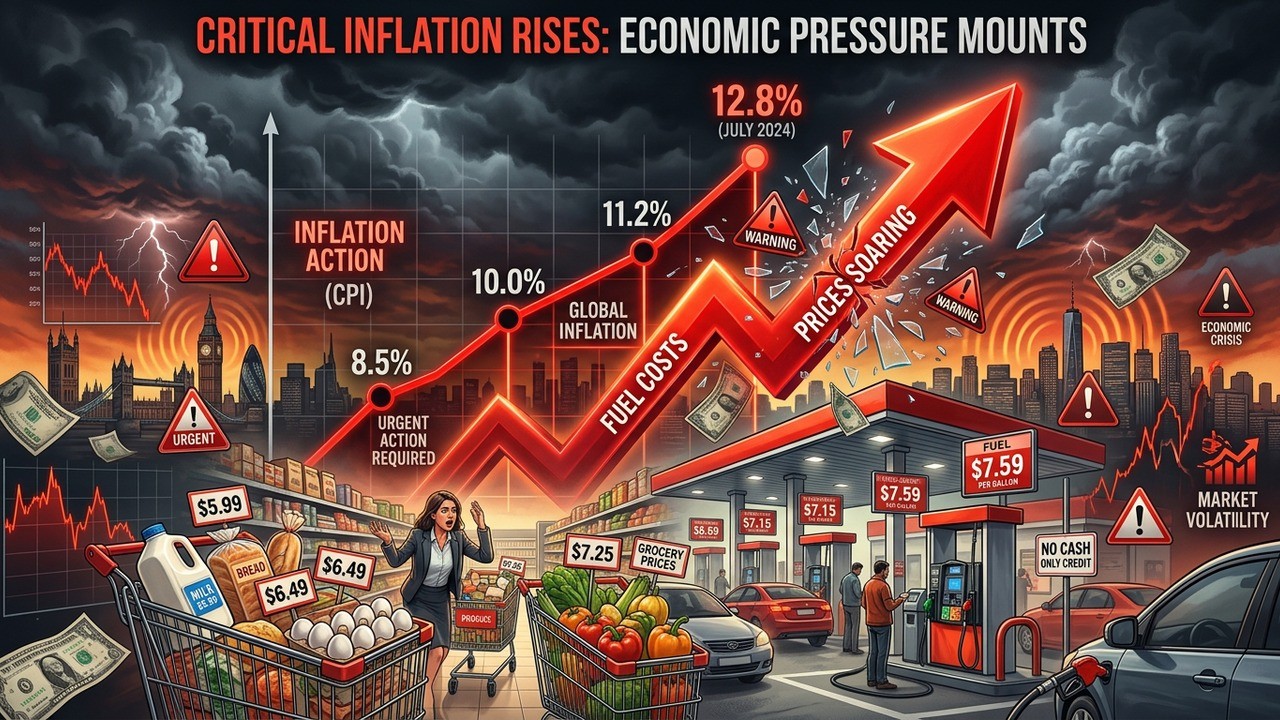

The Sharp Revision in Inflation Expectations

Only three months ago, the consensus among top economists pointed to relatively tame consumer price increases around 2.7% for the early part of the year. Now, that figure has more than doubled in their updated outlook. For the second quarter specifically, many are bracing for headline inflation to reach as high as 6%.

This isn’t just a minor adjustment. It reflects real-world pressures that have intensified rapidly. Energy markets in particular have been volatile, responding to international conflicts and supply uncertainties that have pushed costs higher across the board.

In my view, these kinds of sudden shifts remind us how interconnected our global economy truly is. One event halfway across the world can ripple through gas prices, heating bills, and eventually the items filling our shopping carts.

Breaking Down the Quarterly Projections

Looking more closely at the numbers, the picture becomes clearer – and a bit more worrying. The full-year consumer price index is now expected to land around 3.5%, up noticeably from previous estimates. Even when stripping out the wild swings in food and energy, core inflation projections have risen too.

By the third quarter, things might still feel elevated with headline figures around 3%, before hopefully easing toward the end of the year. Yet even in the fourth quarter, forecasters don’t see inflation dropping back to the levels many had hoped for earlier.

- Second quarter headline CPI projection: 6%

- Full year headline: 3.5%

- Core full year: 2.9%

- Fourth quarter easing to 2.5% headline

These aren’t abstract statistics. They translate into higher costs for families trying to budget, businesses planning investments, and policymakers trying to steer the economy.

The recent surge in inflation is likely to get worse over the next several months.

– Consensus from top economic forecasters

What Triggered This Sudden Change?

Timing matters here. The previous, more optimistic forecasts came before significant military actions involving major players in the Middle East. Those events sent shockwaves through energy markets, driving up oil and gas prices in ways that directly feed into broader inflation measures.

We’ve also seen concrete data confirming these pressures. Both consumer and wholesale price readings for April came in hotter than expected, with some measures hitting multi-year highs. When producers face higher costs, those eventually get passed along to consumers.

It’s worth noting that food prices, transportation costs, and housing expenses all play their parts in this story. Sometimes one sector leads, but lately it feels like multiple areas are contributing to the upward pressure simultaneously.

Implications for Federal Reserve Policy

With new leadership at the Fed, the timing of these inflation developments couldn’t be more critical. While there’s desire for lower interest rates to support growth, the data makes that path much narrower. Policymakers have signaled they’ll remain data-dependent, keeping options open for potential rate hikes if needed.

This creates a challenging balancing act. Too much focus on fighting inflation could slow the economy unnecessarily, but ignoring the price pressures risks letting them become entrenched. I’ve always believed that patience in monetary policy often pays off, but the current environment tests that approach.

The preferred inflation gauge watched closely by the central bank – the personal consumption expenditures index – also shows elevated readings in the forecasts. Second quarter projections there reach 4.5% for the headline measure.

Though indications point toward preference for lower rates, current conditions make that difficult to achieve quickly.

Growth Expectations Take a Hit Too

It’s not just inflation worrying forecasters. They’ve also dialed back expectations for economic growth. Second quarter GDP is now seen expanding at a 2.1% annualized rate, with the full year coming in at 2.2% – a downward revision from earlier estimates.

Looking further ahead, growth might slow even more in 2027 before recovering. This kind of pattern suggests the economy faces headwinds that could persist beyond the immediate inflation spike.

- Monitor personal spending habits as prices rise

- Consider fixed-rate options where possible for major purchases

- Stay informed about upcoming economic data releases

- Evaluate investment allocations with inflation in mind

Unemployment projections have also edged higher, expected to average around 4.5% for the year. While not dramatic, any increase in joblessness combined with rising prices creates a squeeze on household finances.

How This Affects Different Sectors

Energy-intensive industries face particular challenges when oil prices climb. Transportation companies, manufacturers, and even agriculture can see their costs rise rapidly. These pressures don’t stay contained – they spread through supply chains.

Consumers feel it in everyday ways. Higher fuel costs mean more expensive commutes and shipping. Food production and distribution become costlier. Even services can indirectly reflect these underlying increases.

On the positive side, some sectors might benefit from the environment. Energy producers could see improved revenues, though this depends on many variables. Certain defensive stocks or inflation-protected assets often get more attention during these periods.

Longer-Term Inflation Outlook

Even a decade out, forecasters don’t see inflation returning fully to the very low levels of previous years. The ten-year average projection sits at 2.4%, which still exceeds the traditional comfort zone for many policymakers when adjusted to their preferred measures.

This suggests we might be entering a new normal where 2% inflation targets feel more aspirational than easily achievable. Adapting to this reality could require changes in how businesses price products and how individuals approach saving and investing.

Practical Steps for Individuals

Rather than just worrying about the big picture, thinking through personal strategies makes sense. Budget reviews become more important when prices move higher. Looking for ways to reduce energy consumption or lock in certain costs can help.

I’ve found that people who take time to understand these economic signals often make better financial decisions. It’s not about predicting exact numbers but recognizing trends and positioning accordingly.

- Review and adjust monthly budgets to account for higher costs

- Explore opportunities in inflation-resistant investments

- Consider career moves or side income if expenses rise faster than wages

- Build emergency savings with attention to purchasing power

Wage growth will be key too. If salaries keep pace with or exceed inflation, the impact softens. However, when prices rise faster than earnings, living standards can take a hit even if employment remains solid.

Market Reactions and Investment Considerations

Financial markets don’t wait for official reports. They’ve been pricing in these possibilities already, which explains some of the volatility we’ve seen. Bonds, stocks, and commodities all respond differently to inflation expectations.

Higher inflation typically hurts fixed-income investments as real returns decline. Equities can be mixed – some companies pass costs along successfully while others struggle. Commodities often perform better in inflationary environments, though timing matters greatly.

Diversification remains crucial. Spreading risk across different asset types helps weather periods of uncertainty like the one we’re entering.

Elevated inflation levels are expected to persist into the third quarter before any meaningful relief.

Global Context Matters

While this discussion focuses on U.S. numbers, the story has international dimensions. Other economies face similar or different pressures depending on their energy dependence and policy responses. Currency movements can either amplify or dampen domestic inflation.

Trade relationships, supply chain resilience, and fiscal policies abroad all influence what happens at home. Understanding this bigger picture helps explain why forecasts shift so dramatically sometimes.

Perhaps the most interesting aspect is how quickly sentiment can change. From relative optimism to concern in just one quarter shows the dynamic nature of economic forecasting.

Looking Beyond the Headlines

Raw inflation numbers tell part of the story, but not all. Quality adjustments, regional differences, and personal consumption patterns mean that official figures might not perfectly match individual experiences. Someone spending heavily on energy or food feels these increases more acutely.

That said, the broad direction remains clear. Policymakers, businesses, and households all need to navigate this environment carefully. Overreacting could create unnecessary problems, while underestimating the challenge might allow problems to compound.

In my experience following these developments, the periods of transition often offer both risks and opportunities. Those who stay informed and flexible tend to fare better than those caught by surprise.

What Comes Next?

Upcoming data releases will be watched even more closely than usual. Any signs that inflation is peaking or continuing to accelerate could influence policy decisions significantly. Markets will react accordingly, creating potential volatility.

For now, the consensus leans toward persistent pressures through much of the year. The hope is for gradual moderation rather than abrupt changes, giving everyone time to adjust.

Staying prepared doesn’t mean panic. It means awareness and thoughtful planning. Whether you’re managing household finances, running a business, or making investment decisions, understanding these inflation dynamics provides valuable context.

The economic landscape continues evolving, and this latest inflation update serves as an important reminder that predictions require regular revision. What seems certain one quarter can look quite different the next.

As we move through this period, keeping a balanced perspective will help. Inflation at these levels isn’t ideal, but economies have navigated similar challenges before. The key lies in responsive policies and adaptable strategies from all participants.

We’ll continue monitoring developments closely. The coming months should provide more clarity on whether these elevated forecasts prove accurate or if other factors help bring prices back toward more comfortable territory.