Have you ever felt that nagging sense that prices keep climbing no matter how careful you are with your budget? As we head into Wednesday morning, many Americans are bracing for the latest inflation update that could confirm those feelings. The May consumer price index figures are set to drop, and early whispers from Wall Street suggest we might be crossing an unwelcome milestone.

After a period where inflation seemed to be cooling, recent developments have thrown a wrench into the recovery narrative. Energy markets have been particularly volatile, and that turbulence is starting to show up in broader measures of cost increases. What does this mean for everyday consumers and investors alike? Let’s dive deep into what the data might reveal and why it matters right now.

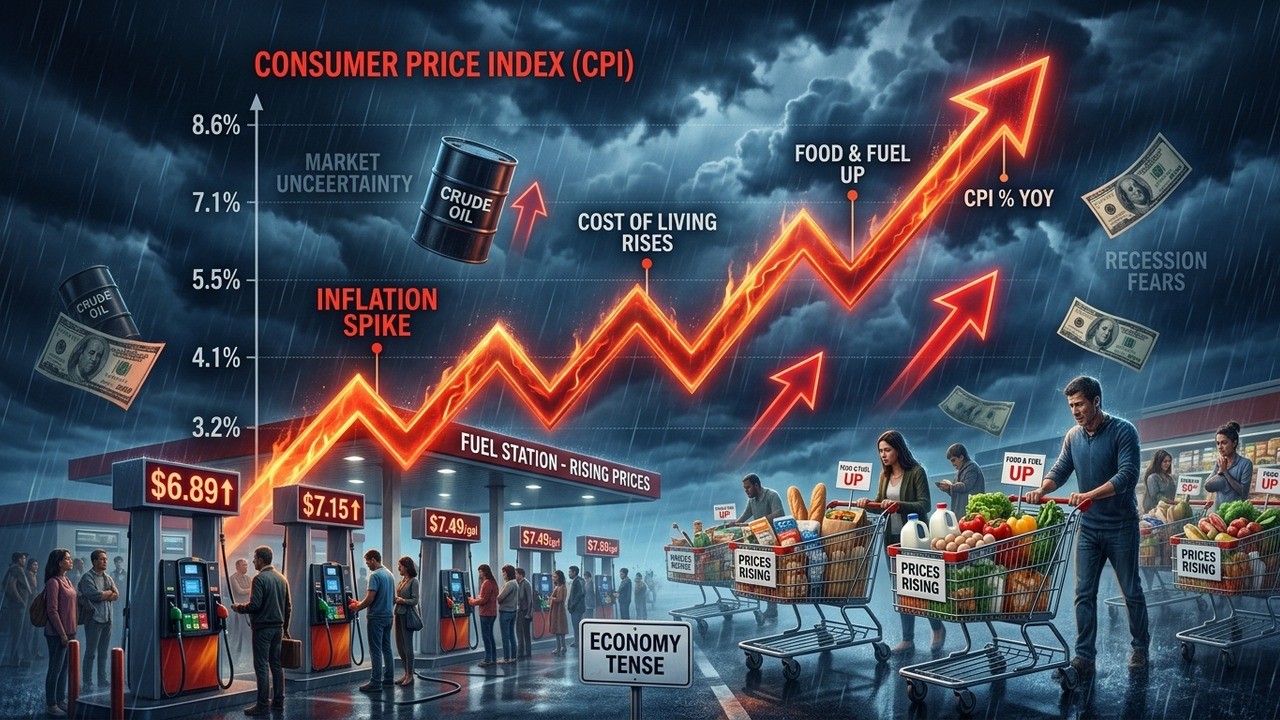

Understanding the Anticipated May CPI Release

The numbers expected this week paint a picture of inflation reaccelerating. Analysts are projecting a headline annual rate around 4.2 percent, coming off a solid 0.5 percent monthly gain. That would mark the first time we’ve seen the CPI push above 4 percent since May 2023. It’s a noticeable shift from the 2.4 percent reading we had just a year ago.

Of course, much of this headline jump ties back to energy costs. The surge in oil prices following geopolitical tensions has rippled through the economy. Yet even when you strip out the volatile food and energy components, core inflation isn’t exactly behaving itself either. Projections call for a 2.9 percent annual core rate after a 0.3 percent monthly increase.

In my experience following these releases over the years, crossing these psychological thresholds often shifts market sentiment more than the raw numbers themselves. When the public sees that 4 handle again, it tends to stick in people’s minds.

Breaking Down the Headline Versus Core Numbers

Headline inflation captures everything, including those wild swings in gas and grocery prices. Core inflation tries to look past the temporary noise to gauge underlying pressures. Right now, both are telling important but slightly different stories.

The April readings showed headline at 3.8 percent and core at 2.8 percent. Moving to May, that expected uptick reflects how energy costs don’t stay isolated. They eventually influence transportation, manufacturing, and even services. It’s like dropping a stone in a pond – the ripples keep spreading.

It’s not just an oil story, it’s a money supply story, and it’s increasingly an AI story. So this is a broader inflation problem than just energy, meaning that we probably still have somewhat sticky inflation.

– Chief investment strategist at a major firm

This perspective highlights something I’ve noticed in recent months. While energy grabs the headlines, other forces are at play. Supply chain adjustments, wage dynamics, and technological investments all contribute to price pressures in their own ways. Dismissing the rise as purely temporary might be overly optimistic.

The Role of Energy Prices in the Current Surge

Oil prices have climbed significantly amid Middle East developments. This isn’t just affecting your weekly fill-up at the pump. Higher energy costs flow into nearly every sector – from food production and delivery to plastics and chemicals used in manufacturing.

Even if conflicts ease quickly, restoring previous production levels isn’t like flipping a switch. Infrastructure damage and market adjustments take time. That means elevated energy prices could linger, keeping upward pressure on the overall inflation picture.

- Transportation costs rising for goods and services

- Manufacturing input prices increasing

- Household energy bills potentially climbing

- Broader spillover into consumer goods pricing

These connections explain why economists are watching this release so closely. A single month’s data doesn’t tell the whole story, but it adds to a pattern that markets will interpret.

Market Reactions and Investor Concerns

Equity markets have shown some skittishness around inflation lately. When price pressures appear sticky, it raises questions about how long higher interest rates might need to stay in place. That uncertainty weighs on valuations, particularly for growth-oriented sectors.

Bond markets are also sensitive here. Higher inflation expectations can push yields higher, affecting everything from mortgage rates to corporate borrowing costs. It’s a complex web where one data point influences many others.

Perhaps the most interesting aspect is how quickly sentiment can shift. Just months ago, talk centered on rate cuts. Now, the conversation includes whether we might need to remain restrictive for longer than previously thought.

Broader Economic Context and Implications

Inflation doesn’t exist in isolation. Consumer spending, business investment, and employment trends all interact with price changes. When costs rise faster than wages for many households, it squeezes budgets and can slow economic momentum over time.

Small businesses face particular challenges as they try to manage higher input costs while remaining competitive on pricing. Some pass costs along, others absorb them and see margins shrink. Either path has consequences.

Even if there would be a quick resolution to the war, you probably wouldn’t see oil prices come down to prior lows, because there’s been so much disruption to production. That’s not something that a switch can just be turned back on.

This reality check matters. Policy makers and investors alike need to account for these lags and structural changes rather than hoping for an immediate return to previous conditions.

What This Means for Different Sectors

Energy companies might benefit from higher prices in the near term, but the picture is mixed across the board. Consumer discretionary sectors could face headwinds as households prioritize essentials. Technology and growth stocks often react negatively to persistent inflation due to higher discount rates on future earnings.

Real estate and housing remain sensitive to interest rate expectations tied to inflation. Even utilities and staples, typically more defensive, aren’t completely immune when energy costs spike.

| Sector | Potential Impact | Key Driver |

| Energy | Positive near-term | Higher commodity prices |

| Consumer Goods | Pressure on margins | Input cost increases |

| Technology | Valuation challenges | Higher rates |

| Financials | Mixed signals | Yield curve dynamics |

Of course, these are generalizations. Individual companies within sectors can perform very differently based on their specific situations.

Looking Beyond the Headlines

While the May numbers will grab attention, smart observers look at trends over multiple months. Is this a one-off bump or the start of a new phase? Wage growth, productivity improvements, and supply chain resilience will all influence the path ahead.

Technological advancements, including AI applications in business, could eventually help tame some costs through efficiency gains. But in the shorter term, implementation expenses and adjustments can actually add to price pressures – something worth watching.

I’ve always believed that inflation expectations are almost as important as actual inflation. When businesses and consumers start baking higher prices into their planning, it can become somewhat self-fulfilling. Breaking that cycle requires clear progress on multiple fronts.

Preparing for Different Scenarios

Investors might consider how their portfolios are positioned for various inflation outcomes. Diversification across asset classes, attention to real returns, and focus on companies with pricing power can help navigate uncertainty.

- Review exposure to interest rate sensitive assets

- Consider inflation-protected securities where appropriate

- Focus on quality companies with strong balance sheets

- Maintain some cash reserves for potential opportunities

- Stay informed but avoid knee-jerk reactions to single data points

At the household level, similar principles apply. Budgeting with some buffer for rising costs, seeking ways to improve energy efficiency, and being thoughtful about major purchases can make a difference.

The Bigger Picture for Economic Policy

Central bankers face a delicate balancing act. They want to support growth while keeping price stability. Recent data complicates that task by suggesting inflation might not be vanquished as quickly as hoped.

Markets will parse every word from officials in coming weeks, looking for clues about the likely policy path. Clear communication becomes even more valuable during uncertain times.

Ultimately, sustainable economic growth requires price stability. Getting back to that environment might take longer than many initially expected, but patience and prudent policy could still deliver positive results over time.

Key Factors to Watch After the Release

Once the CPI numbers are out, the focus will quickly shift to details within the report. Which categories are driving the changes? Are there signs of broadening pressures or containment? How do these figures compare to forecasts?

Forward-looking indicators like inflation expectations from surveys and market-based measures will also gain attention. Consistency across different data sources builds confidence in the narrative, while divergences create more questions.

In my view, the most important question isn’t just what happened last month, but what it suggests about the next several months. Context always matters more than any single snapshot.

Historical Perspective on Inflation Cycles

Looking back, inflation has periods of acceleration and deceleration. External shocks like geopolitical events often play a role, but domestic factors determine how long effects last. The current environment shares some similarities with past episodes while differing in important ways due to modern supply chains and technology.

Understanding these patterns helps frame current developments without overreacting. We’ve navigated challenging inflation periods before, and resilience has typically followed.

Remember: A single month's data is one piece of a much larger puzzle.

This reminder feels particularly relevant now. With so many variables at play – from global events to domestic policy choices – maintaining perspective serves investors and consumers well.

Practical Takeaways for Readers

Regardless of the exact numbers on Wednesday, certain principles remain useful. Building financial buffers, focusing on long-term goals, and avoiding emotional decisions based on headlines can help weather economic fluctuations.

Staying informed through reliable sources while recognizing that markets often overreact in both directions creates an edge. Knowledge combined with patience tends to be a winning combination over time.

As we await this important data point, it’s worth reflecting on how far we’ve come in the inflation battle and what steps might still be needed. The path ahead likely won’t be perfectly smooth, but understanding the dynamics puts us in a better position to navigate it.

The coming weeks and months will reveal more about whether this uptick represents a temporary bump or requires more significant adjustments in expectations and strategy. For now, Wednesday’s release will provide the next chapter in an ongoing economic story that affects us all.

Whatever the precise figures show, one thing seems clear: vigilance around costs and thoughtful planning remain essential skills in today’s environment. By looking beyond the surface numbers to underlying trends, we can make more informed decisions for our financial futures.

**