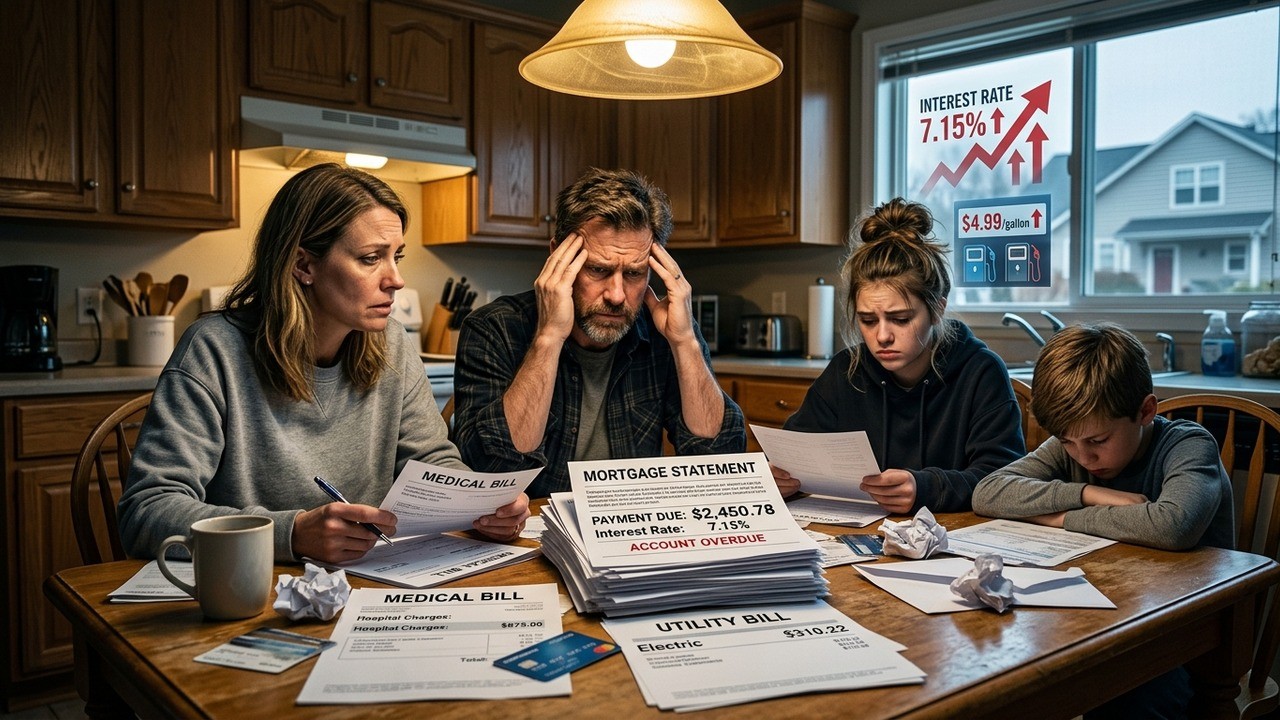

Have you ever opened your monthly bills and just paused, wondering how things got this expensive this fast? I know I have. Lately, conversations with friends and neighbors keep circling back to the same uncomfortable truth: making ends meet feels harder than ever. And the numbers coming out recently paint a picture that’s hard to ignore. For the first time in history, the typical monthly mortgage payment in the United States has climbed above two thousand dollars. That’s not just a statistic. It’s a daily reality reshaping how families budget, save, and even dream about the future.

What used to be a manageable part of the American Dream has turned into a heavy weight for millions. Home prices keep pushing upward while interest rates refuse to come down comfortably. Combine that with other essential costs skyrocketing, and you have a situation where even dual-income households feel stretched thin. I’ve spoken with people who work long hours yet still find themselves choosing between fixing the car and paying the insurance premium. This isn’t about occasional tough months anymore. It feels like a slow, steady shift that’s been building for years.

The Mortgage Milestone That’s Raising Eyebrows Nationwide

Let’s talk about that mortgage figure more closely. In late 2025, the average payment on existing home loans reached $2,005 according to industry reports. That’s a massive 44 percent jump from just a few years earlier. For many families, this means an extra six hundred dollars or more leaving their accounts each month compared to 2021. Think about what you could do with that money if it weren’t tied up in housing costs alone.

Homeownership has always carried expenses, but this level feels different. Younger buyers entering the market face even steeper challenges with new purchase loans often carrying higher rates. Those who bought earlier and refinanced or locked in lower rates years ago are still seeing their overall cost of living rise around them. The housing market simply hasn’t cooled enough to bring relief to the average person.

Why Home Prices and Rates Refuse to Budge

Several factors play into this stubborn situation. Limited inventory in desirable areas keeps pushing prices higher. Builders struggle with material costs and labor shortages, meaning new homes don’t come online fast enough to meet demand. At the same time, mortgage rates remain elevated compared to the super-low period we saw during the pandemic. Even small increases in the rate can add hundreds to the monthly bill over a thirty-year loan.

In my experience following these trends, the psychological impact matters just as much as the dollars. People who once viewed their home as a source of stability now worry about whether they can keep up if something unexpected happens. A job change, medical issue, or repair can quickly turn into a crisis when so much income already goes toward the mortgage.

The rise in housing costs isn’t just numbers on a spreadsheet. It’s families making tough choices about vacations, education funds, and even daily groceries.

This pressure doesn’t stop at the mortgage statement. It ripples into every other area of household spending. When shelter takes such a large bite, less remains for everything else that makes life feel balanced and secure.

Health Insurance Costs Surpassing Housing Expenses

Here’s something that really stops you in your tracks. The average family now spends more on health insurance each month than on their mortgage. We’re talking over $2,200 in many cases. That shift says a lot about where our priorities and systems have landed. Keeping your family healthy has literally become more expensive than keeping a roof overhead for many Americans.

Premiums continue their upward climb year after year with no real signs of slowing. Deductibles grow larger too, meaning you pay more out of pocket before coverage even kicks in. I’ve heard from parents who hesitate to take their kids to the doctor for anything short of an emergency because of what it might cost. That kind of hesitation carries real consequences for long-term health and peace of mind.

- Monthly premiums that consume a huge chunk of take-home pay

- Higher deductibles forcing more direct spending

- Prescription drug costs adding another layer of burden

- Limited provider networks restricting choices

The frustration runs deep. Many feel the system benefits large companies more than the people it should serve. When nearly everyone you talk to shares similar complaints, you know something needs attention. Yet real solutions seem stuck in political gridlock while families bear the daily cost.

Energy Prices Spike Amid Global Tensions

The situation gets even more complicated when you factor in events happening overseas. Conflicts in the Middle East have sent energy prices higher, adding hundreds of dollars to household budgets in just a few months. Gasoline alone has cost the typical family an extra four hundred dollars or more since tensions escalated. For people who drive to work or have long commutes, this hits especially hard.

Oil inventories are being drawn down rapidly, and strategic reserves have dropped to concerning levels. This isn’t a temporary blip that will vanish next week. The longer these pressures continue, the more they work their way through the entire economy. Everything from groceries to manufactured goods feels the impact because transportation costs rise.

I’ve always believed that energy stability forms the foundation for economic confidence. When that foundation shakes, everything built on top becomes less secure. Families adjust by cutting back on non-essentials, but those cuts eventually affect local businesses and jobs too. It’s a chain reaction that’s difficult to stop once it gains momentum.

Household Debt Reaches Dangerous New Heights

With all these costs mounting, it’s no surprise that total household debt has climbed to record levels. The latest figures show Americans carrying nearly $18.8 trillion in debt. Credit card delinquencies have jumped to their highest point in fifteen years, signaling that many people have reached their limit. They’re using plastic to bridge gaps that their regular income can’t cover anymore.

This debt spiral creates a heavy emotional load. The constant worry about minimum payments and interest charges steals focus from enjoying life or planning ahead. Young adults especially face tough entry points into financial independence when student loans, rent, and now higher everyday costs stack up so quickly.

When basic expenses require borrowing, the cycle becomes incredibly difficult to break without major changes.

Saving for emergencies or retirement feels like a luxury many can’t afford right now. That lack of a safety net makes every unexpected bill feel like a potential disaster.

Workforce Participation and the Hidden Crisis

Another troubling trend sits in the background: fewer men participating in the workforce. Only about 66 percent of men aged twenty and older are working or actively looking for work. That’s near levels last seen during major economic downturns. When large portions of the population step back from employment, it affects everything from family income to overall economic growth.

Reasons vary. Some cite discouragement after long job searches, others point to health issues, caregiving responsibilities, or simply deciding the math doesn’t work when wages don’t keep pace with costs. Whatever the individual stories, the collective impact creates less tax revenue, smaller consumer spending, and added pressure on social systems.

Women have increased their participation in many fields, which helps, but it also places new stresses on family dynamics and childcare arrangements. The ideal of a single-income household that could comfortably support a family feels increasingly out of reach for most.

How Families Are Adapting Day to Day

People find creative ways to cope. Some move in with relatives to share expenses. Others take on side gigs or second jobs despite the exhaustion that brings. Budgeting apps and strict tracking have become common tools, yet even careful planners struggle when prices keep shifting upward.

- Reviewing every subscription and membership for possible cuts

- Meal prepping and reducing dining out

- Shopping sales and using coupons more strategically

- Delaying major purchases or home improvements

- Seeking community resources and support networks

These adjustments help in the short term, but they don’t solve the underlying problems. When basic middle-class life requires six-figure income in many regions, something fundamental has shifted in our economy.

I’ve found myself reflecting often on what a sustainable path forward might look like. Perhaps more focus on vocational training, policies that actually encourage housing construction, or incentives for domestic energy production could ease some pressure. But those conversations tend to get lost in partisan noise while families continue carrying the load.

The Broader Picture of Cost of Living Pressure

Inflation statistics released by officials often tell a milder story than what people experience at grocery stores, gas stations, and utility companies. This gap between reported numbers and real-world spending creates distrust and frustration. When your paycheck buys noticeably less each year, abstract percentages feel disconnected from daily struggles.

Food prices, vehicle maintenance, childcare, and education costs have all climbed significantly. Each area compounds the others. A family might handle one increase, but when several hit simultaneously, the budget breaks. This explains why so many report higher financial stress than at any previous point in their lives.

| Category | Recent Change | Impact on Families |

| Mortgage | +44% since 2021 | Higher monthly commitments |

| Health Insurance | Exceeds mortgage | Reduced disposable income |

| Gasoline | + $400+ per household | Transportation budget strain |

| Credit Debt | Delinquency at 13.1% | Long-term financial risk |

Looking at these figures side by side helps illustrate why so many feel overwhelmed. The combined effect creates a situation where progress feels elusive no matter how hard people work.

What This Means for Future Generations

Younger adults watching these trends develop may question whether homeownership or even starting a family remains realistic. That kind of doubt affects society on a deeper level. When the next generation loses confidence in the traditional milestones of success, motivation and innovation can suffer.

Yet I remain cautiously optimistic. History shows Americans adapt and find solutions during challenging periods. Innovation in housing, energy, and healthcare could still bring relief if we prioritize practical approaches over ideology. The key lies in recognizing the problem honestly rather than downplaying it with cherry-picked statistics.

Communities can play a role too. Local initiatives supporting affordable housing, job training programs, and small business growth might provide more immediate help than waiting for Washington to act. Neighbors helping neighbors has always been part of the American spirit during tough times.

Personal Reflections on Financial Resilience

In my own conversations and observations, the people who seem to manage best focus on controllable factors. They build emergency funds when possible, develop multiple income streams, and maintain realistic expectations. They also talk openly with family about money instead of pretending everything is fine until it isn’t.

That openness matters. Financial stress can damage relationships and health if kept hidden. Acknowledging the challenge together often leads to better decision-making and reduced anxiety. Perhaps the most valuable skill right now is learning to live well within constraints while still working toward improvement.

The road ahead won’t be easy. With mortgage payments at record levels, energy costs fluctuating, and other essentials demanding more of our income, American families are navigating uncharted territory. Yet recognizing these pressures clearly is the first step toward finding workable paths forward. Whether through policy changes, personal habits, or community support, the goal remains the same: creating conditions where hard work can once again provide genuine security and opportunity.

We’ve covered a lot of ground here because this issue touches nearly every aspect of modern life. From the monthly budget meeting at the kitchen table to larger questions about economic fairness and stability, these trends deserve serious attention. If you’re feeling the squeeze yourself, know that you’re far from alone. Millions share similar stories and frustrations right now.

The coming months and years will test our collective resilience. How we respond, both individually and as a society, will shape the economic landscape our children inherit. Staying informed, making thoughtful choices, and advocating for practical solutions can help move us toward more sustainable outcomes. The American spirit has overcome big challenges before. With clear eyes and determined effort, it can do so again.

Take time to review your own financial picture. Small adjustments today might prevent larger problems tomorrow. Talk with others facing similar situations. Share strategies that work. Build support networks that extend beyond just financial advice to include encouragement and perspective. These human connections often provide the strength needed during uncertain periods.

Ultimately, understanding the full scope of these cost increases helps us face them more effectively. The mortgage payment milestone of $2000 serves as a wake-up call, but it doesn’t have to define our future. By addressing root causes and supporting one another, we can work toward an economy that better serves the people working hardest within it. The conversation continues, and every voice matters in finding the right direction ahead.