I’ve followed the cross-border payments world for years, and few debates have been as passionate as the one surrounding Ripple and SWIFT. The idea that XRP would completely upend the traditional banking messaging giant captured imaginations, fueled countless online discussions, and became a cornerstone of many investment theses. Yet here we are in 2026, and the reality feels both more promising and more complicated than the bold headlines of the past.

When you step back and look at the actual developments rather than the slogans, a fascinating story emerges. SWIFT isn’t fading away. Instead, it’s evolving aggressively while Ripple has adjusted its approach in subtle but meaningful ways. The question isn’t simply whether one replaces the other anymore. It’s about how these systems are learning to coexist, compete, and occasionally connect in an increasingly digital financial landscape.

Understanding the Core Tension Between Speed and Tradition

Let’s be honest from the start. The traditional cross-border payment system has frustrations built into its DNA. When a business in one country wants to send money abroad, the process often involves multiple banks, pre-funded accounts in different currencies, and days of waiting. Fees add up, transparency can be limited, and weekends or holidays bring everything to a halt. This is where the promise of blockchain technology, and specifically solutions like those from Ripple, entered the conversation with such force.

Yet SWIFT, for all its perceived slowness, serves as the trusted backbone for over eleven thousand financial institutions worldwide. It handles instructions for trillions of dollars daily. It’s not going anywhere overnight, and understanding exactly what it does versus what newer technologies offer is key to seeing the bigger picture.

What SWIFT Really Does Day to Day

SWIFT functions primarily as a messaging network. Think of it like the postal service for bank instructions. When Bank A needs to transfer funds to Bank B overseas, SWIFT carries the detailed message telling the recipient bank what to do. The actual movement of money happens separately through correspondent banking relationships. This distinction matters enormously because many critiques aimed at SWIFT actually target the underlying settlement layers rather than the messaging itself.

Over time, SWIFT has introduced improvements like its gpi service, which dramatically sped up tracking and reduced settlement times for many transactions. Still, the core architecture relies on those pre-funded accounts and intermediary banks, creating friction that innovators sought to eliminate.

The real bottleneck in international transfers has always been the settlement plumbing beneath the messaging layer.

In my view, recognizing this separation helps explain why the replacement narrative gained so much traction. If you could solve the settlement problem directly, the entire process could transform. This is precisely what Ripple set out to achieve with its focus on actual value movement rather than just instructions.

How Ripple’s On-Demand Liquidity Changes the Game

Ripple took a different approach by building technology that targets the settlement layer head-on. Through On-Demand Liquidity (ODL), financial institutions can convert sending currency to XRP, move that value across the XRP Ledger in seconds, and convert it to the destination currency on the other side. This eliminates the need for maintaining large pre-funded balances in multiple foreign currencies.

The benefits are tangible: near-instant settlement, minimal costs, and 24/7 availability. For businesses operating across time zones and dealing with volatile currencies, this represents a genuine leap forward. The XRP Ledger has proven its reliability through billions of transactions, handling significant liquidity volumes in real-world use cases.

Yet as impressive as this technology is, adoption by major institutions hasn’t followed the explosive trajectory some predicted. Banks tend to move cautiously, prioritizing regulatory comfort and integration with existing systems over pure speed and cost savings.

The ISO 20022 Factor: More Hype Than Magic Bullet

No discussion about modern payments would be complete without addressing ISO 20022. This new global standard for financial messaging brings richer data, better automation, and improved compliance capabilities. SWIFT completed its full migration to this standard in late 2025, marking a significant modernization of its infrastructure.

Many in the XRP community interpreted this shift as automatic validation for their preferred asset. The reality is more measured. While Ripple’s network can handle ISO 20022 messages effectively, the standard itself focuses on data formatting rather than endorsing specific settlement assets. It creates a more level playing field where both traditional and blockchain solutions can compete on better terms.

- Improved data richness for compliance and automation

- Better interoperability between different payment systems

- No direct certification of cryptocurrencies or tokens

- Benefits established players like SWIFT as much as newcomers

Perhaps the most interesting aspect is how this standard enables rather than dictates outcomes. It raises the bar for everyone without crowning a single winner.

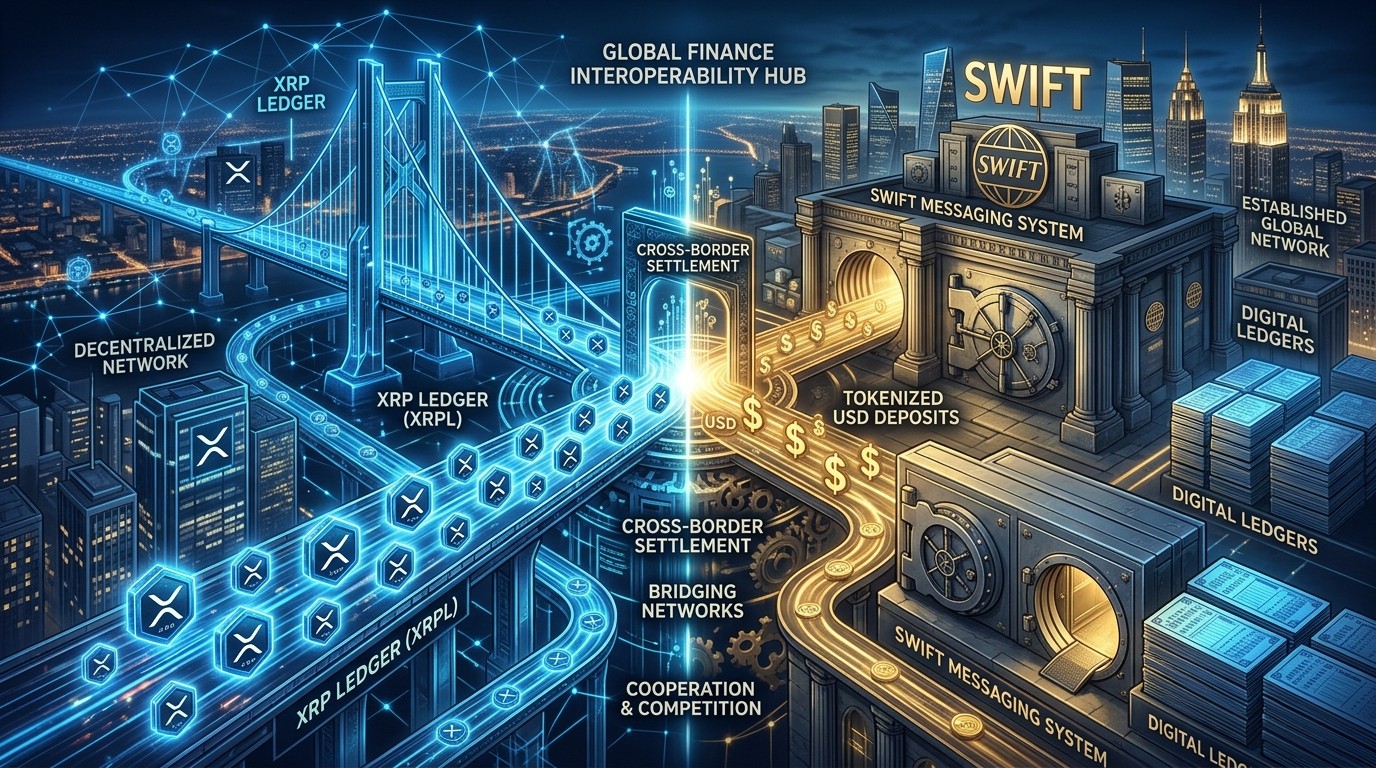

SWIFT’s Blockchain Evolution: Not Standing Still

One of the most overlooked developments in 2026 is SWIFT’s proactive move into blockchain technology. After finalizing its ISO 20022 migration, the organization has been building its own permissioned shared ledger designed for round-the-clock cross-border settlement. This isn’t some distant concept – trials with dozens of banks have already taken place, and the project moved into active development earlier this year.

What makes this particularly relevant is the design philosophy behind it. SWIFT’s ledger focuses on tokenized bank deposits and keeps value firmly within regulated banking perimeters. This approach prioritizes the control and auditability that supervisors and central banks demand. Public network assets like XRP were deliberately excluded from the core architecture.

In my experience covering fintech, this represents a classic incumbent strategy: absorb the benefits of new technology while maintaining control over the rails. SWIFT aims to offer blockchain speed and programmability without ceding ground to external networks.

The XRP Exclusion and What It Really Means

For XRP enthusiasts, SWIFT’s decision to build without incorporating public assets like XRP feels like a significant blow to the replacement narrative. If banks can achieve fast, blockchain-based settlement using trusted tokenized deposits through their existing SWIFT connection, the unique value proposition of XRP as a mandatory bridge asset weakens considerably.

This doesn’t mean XRP has no role. Far from it. But it does suggest the future won’t be the wholesale displacement many envisioned. Instead, we’re seeing parallel systems developing, each with distinct advantages depending on the specific use case and risk tolerance of the institutions involved.

Institutions value familiarity and regulatory certainty as much as they value technological innovation.

The Side Door: Optional Integration Through Partners

Here’s where the story gets nuanced. Even as SWIFT builds its XRP-free ledger, connections exist that give banks optional access to Ripple’s liquidity solutions. Through partnerships with payments specialists, SWIFT-connected institutions can route certain transactions through ODL when it makes sense for them.

The keyword here is “optional.” Banks aren’t required to use XRP. They can choose it when the speed and cost benefits outweigh other considerations, but they retain full flexibility. This creates a marketplace of solutions rather than a forced migration to a single standard.

From a practical standpoint, this optionality provides XRP with valuable distribution and exposure. Thousands of institutions now have easier technical access to the technology. Whether they actually route meaningful volume through it remains to be seen and will depend on real-world performance and internal decision-making.

Ripple’s Strategic Pivot Toward Stability

Perhaps the strongest signal about the evolving landscape comes from Ripple itself. The company has invested heavily in RLUSD, its own dollar-pegged stablecoin designed for enterprise use. This move speaks volumes about how Ripple views the future.

By offering a stable, regulated alternative to volatile bridge assets, Ripple demonstrates pragmatism. Not every institution wants exposure to price fluctuations, even for brief periods. A stablecoin settlement option provides speed without volatility, complementing rather than competing directly with traditional tokenized deposits.

I’ve always believed successful companies adapt to market realities rather than clinging to initial visions. Ripple’s diversification suggests they understand the future will likely feature multiple coexisting solutions rather than one dominant winner.

What This Means for XRP Holders in 2026

Let’s talk directly to those who hold XRP or are considering it. The replacement dream painted a picture of inevitable dominance where XRP would capture enormous value as the primary settlement asset for global finance. The complementary reality is more grounded but still offers genuine opportunity.

XRP’s strengths remain clear: unmatched speed, extremely low costs, and continuous operation. Through optional integrations, it has a seat at the table with major institutions. The question shifts from “Will XRP replace SWIFT?” to more practical ones: How often will institutions actually choose the XRP rail when given options? Can ODL volume grow sufficiently to impact the token’s economics given its supply?

- Focus on real adoption metrics rather than headlines

- Understand that competition will be fierce from multiple alternatives

- Recognize that regulatory clarity and institutional comfort take time

- Consider the broader ecosystem including stablecoin developments

In my opinion, this reframing from inevitability to competition creates a healthier investment thesis. It rewards actual utility and sustained growth rather than narrative momentum.

The Broader Implications for Global Finance

Beyond XRP specifically, the interplay between traditional finance and blockchain innovation is reshaping expectations across the industry. We’re moving toward a hybrid model where the best elements of both worlds combine in different configurations depending on needs.

Permissioned ledgers offer control and regulatory alignment. Public networks provide neutrality and efficiency. Stablecoins bridge gaps with reduced volatility. The winners will likely be those who integrate these tools most effectively rather than those who bet everything on a single approach.

| Approach | Strengths | Limitations |

| Traditional SWIFT | Trust, scale, regulation | Speed, cost, availability |

| XRP ODL | Speed, cost, 24/7 | Volatility, adoption barriers |

| Tokenized Deposits | Regulatory comfort, familiarity | Less decentralized |

| Stablecoins | Stability, programmability | Issuer dependency |

This table illustrates why a single winner-takes-all outcome seems increasingly unlikely. Different tools serve different purposes, and institutions value choice.

Looking Ahead: Fragmented Innovation Rather Than Revolution

As we move further into 2026 and beyond, the most likely scenario appears to be continued evolution rather than sudden disruption. SWIFT will keep modernizing its offerings. Ripple and similar innovators will push boundaries with new products and integrations. Banks will adopt what works best for their specific needs while managing risk carefully.

For XRP, this means its success depends on proving superior value in head-to-head competition rather than riding a wave of inevitable replacement. The optional nature of its integrations gives it a genuine chance to demonstrate utility at scale. Whether that translates into sustained demand sufficient to support its market position remains one of the more interesting questions in crypto today.

I’ve come to appreciate how financial systems evolve incrementally even when technology offers revolutionary potential. Trust, regulation, and legacy infrastructure create powerful inertia. The companies that succeed are those who work with rather than purely against these realities.

Practical Considerations for Anyone Following This Space

If you’re interested in the future of payments or hold positions in related assets, staying informed means looking beyond surface-level narratives. Pay attention to actual transaction volumes, partnership announcements that include usage metrics, and regulatory developments that could open or close doors for different solutions.

The integration of blockchain into traditional finance isn’t a binary event but a gradual process with many players and competing visions. Understanding the nuances helps separate signal from noise in what remains a noisy and often hype-driven market.

One thing seems clear: the conversation has matured. The simplistic “XRP will flip SWIFT” framing has given way to more sophisticated analysis about complementary roles, optional adoption, and the complex interplay between innovation and regulation. That shift itself represents progress.

Whether XRP ultimately carves out a significant permanent role in global settlement will depend on its ability to deliver consistent value in a world that now offers multiple paths to similar outcomes. The technology is impressive. The market adoption challenge is substantial. And the story continues to unfold in real time.

From my perspective, the most exciting possibility isn’t total replacement but meaningful coexistence where different solutions push each other toward better performance. In that world, users and businesses ultimately benefit from increased choice and efficiency. And that, perhaps more than any single winner, represents the real transformation we’ve been waiting for in cross-border finance.

The coming months and years will reveal how these dynamics play out. SWIFT’s blockchain initiatives, Ripple’s stablecoin efforts, and the real-world usage patterns of optional XRP liquidity will provide the data points needed for clearer assessment. For now, the evidence points toward a more connected, competitive, and ultimately more capable global payments ecosystem than we had before.