Have you ever wondered how much more your Social Security check might need to stretch next year just to keep up with the bills? With fresh government data showing inflation heating up again, many retirees are watching closely for clues about their 2027 cost-of-living adjustment. The numbers coming in suggest it could be more generous than earlier predictions, but there’s still plenty of uncertainty ahead.

Why the 2027 Social Security COLA Matters More Than Ever

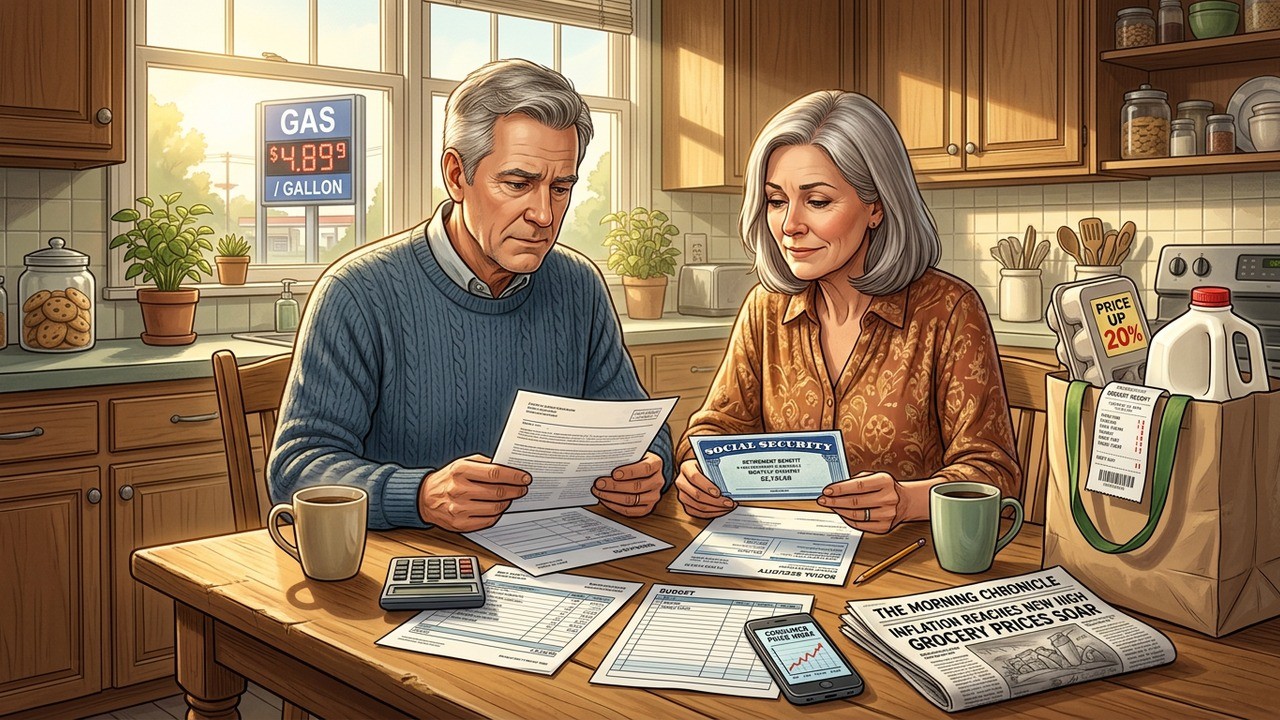

Inflation has a sneaky way of eating away at fixed incomes, and for millions of Americans relying on Social Security, even small changes in the COLA can make a real difference in daily life. Recent figures indicate the Consumer Price Index for Urban Wage Earners and Clerical Workers, known as CPI-W, rose notably over the past year. This index is the key benchmark used to calculate annual benefit increases.

In my view, these adjustments aren’t just numbers on a page. They represent real purchasing power for people who have worked hard their entire lives and now depend on these benefits to cover essentials like groceries, housing, and healthcare. When inflation accelerates, the pressure mounts quickly.

Latest Inflation Data Sparks Revised Forecasts

April’s inflation report caught attention with a 3.9% increase in the CPI-W over the previous 12 months. Analysts tracking these trends have bumped up their expectations for the coming year’s adjustment. Some independent experts now project the 2027 COLA could land between 3.9% and 4.2%, a noticeable step up from earlier estimates around 2.8% to 3.2%.

It’s worth noting how certain everyday costs are driving this shift. Prices for gasoline, home heating oil, fresh produce, and even coffee have climbed noticeably. These aren’t luxury items for most households – they’re necessities that hit fixed-income budgets hard.

The pace of certain price increases has been sharper than anticipated, which directly feeds into higher potential COLA calculations.

This kind of movement reminds us that economic conditions can change direction faster than we expect. Retirees I speak with often express a mix of cautious optimism and lingering worry about whether the adjustment will truly match their lived experience at the store.

Understanding How Social Security COLA Is Calculated

The process itself is straightforward on paper but depends heavily on timing. Officials look at CPI-W data from the third quarter of the current year compared to the same period the year before. That difference determines the percentage increase, if any, announced typically in October for the following January.

With several months of data still to come, current forecasts remain preliminary. Yet the recent uptick has shifted conversations from modest increases to something potentially more meaningful for beneficiaries.

- Third-quarter CPI-W readings are the official basis for the final number

- Energy and food prices often play an outsized role in the index

- Past adjustments have ranged widely depending on economic conditions

Over the last decade, the average COLA has hovered around 3.1%. The 2026 increase came in at 2.8%, providing some relief but perhaps not enough for everyone feeling the pinch from cumulative price rises.

The Real Impact on Average Retiree Benefits

Let’s put some numbers to this. A 3.9% COLA might translate to roughly $81 more per month for the typical beneficiary. While welcome, many seniors point out that years of smaller adjustments have left their benefits lagging behind actual cost increases. One analysis suggests purchasing power has declined by over 13% since 2016, requiring a much larger catch-up to restore balance.

I’ve heard from older friends and family members how even a modest bump helps with confidence in planning, but persistent inflation in housing and medical costs can quickly absorb those gains. It’s a delicate balance that policymakers try to navigate.

What stands out in recent reports is how specific categories are contributing to the broader trend. Fresh vegetables, dairy, and transportation fuels have seen notable jumps. These directly affect household budgets in ways that general inflation figures sometimes mask.

Broader Economic Context Behind the Numbers

Inflation isn’t happening in isolation. Factors like supply chain ripples, energy market shifts, and global events continue to influence domestic prices. The overall consumer price index reached 3.8% in the latest reading, the highest in some time, signaling broader pressures that could persist.

For retirees, this environment creates both challenges and opportunities to review their financial strategies. Those with some flexibility in investments or part-time work might offset pressures more easily, but many live primarily on these benefits.

Fixed incomes require careful attention when prices move unexpectedly.

Perhaps the most interesting aspect is how different generations view these developments. Younger workers paying into the system today wonder about its long-term sustainability, while current recipients focus on immediate affordability.

Historical Perspective on COLA Adjustments

Social Security has included cost-of-living adjustments for decades to help maintain benefit value. Some years brought double-digit increases during high inflation periods, while others saw zero adjustments when prices were stable. This variability underscores why tracking current trends matters so much.

Looking back, the average over recent years shows modest growth, but cumulative effects matter. When small shortfalls compound over time, the gap between benefits and real needs widens, prompting calls for potential reforms or supplemental support measures.

- Review your current budget against recent price changes

- Consider healthcare cost projections for coming years

- Explore ways to supplement income if possible

- Stay informed about official announcements in October

Preparation can ease anxiety. Even small steps like tracking expenses more closely or discussing options with family can provide peace of mind.

What Retirees Can Do While Waiting for Official Figures

Waiting for the final October announcement doesn’t mean sitting idle. Many financial advisors recommend using this period to assess overall retirement readiness. Are there areas where spending could be optimized? Might certain benefits or tax strategies yield extra savings?

In my experience talking with people navigating retirement, those who take a proactive approach often feel more in control regardless of the exact COLA percentage. Simple actions like reviewing energy usage, comparing insurance options, or even community resources for seniors can stretch dollars further.

| Potential COLA Range | Estimated Monthly Increase | Key Driving Factors |

| 3.9% | Around $81 | Energy and food prices |

| 4.2% | Higher end | Broader inflation trends |

Of course, individual circumstances vary widely. Average benefit figures provide a starting point, but actual amounts depend on earnings history and other factors.

Challenges Beyond the Headline COLA Number

Even with a solid adjustment, other pressures remain. Healthcare costs often rise faster than general inflation, and housing expenses continue climbing in many regions. These realities mean the COLA serves as one piece in a larger financial puzzle.

I’ve found that conversations about retirement security benefit from looking holistically. Savings, investments, family support networks, and government programs all interact. Ignoring any element can lead to unpleasant surprises down the road.

Another consideration involves the long-term health of the Social Security system itself. While COLA discussions focus on immediate relief, broader solvency debates continue among policymakers. Understanding both short-term adjustments and potential future changes helps in planning.

How Different Household Types Might Experience the Change

Single retirees often feel price shifts more acutely than couples who can share certain costs. Urban dwellers might face higher housing and transportation expenses compared to those in rural areas. These differences highlight why one-size-fits-all solutions rarely address every need perfectly.

Consider a typical grocery basket today versus a few years ago. Items once taken for granted now require more careful selection. A higher COLA provides breathing room, but smart shopping habits and meal planning remain valuable tools.

Every percentage point matters when your budget is tight.

Energy costs deserve special mention. With winter heating bills on the horizon for many, any boost from COLA could help offset anticipated rises in utility expenses. Timing of these factors plays a crucial role in how helpful the adjustment feels.

Looking Ahead: Remaining Months of Data

Five more months of inflation readings will shape the final calculation. Economists will watch energy markets, supply chains, and consumer behavior closely. Unexpected events could still move the needle in either direction, which is why experts caution against treating current forecasts as guarantees.

This uncertainty is part of what makes financial planning both challenging and essential. Building some flexibility into retirement strategies can help weather varying economic conditions over time.

Many seniors also explore part-time work or gig opportunities not just for income but for social connection and mental engagement. These choices can complement benefit increases in meaningful ways.

Practical Tips for Maximizing Your Benefits

- Delay claiming if possible to increase monthly amounts

- Coordinate spousal benefits strategically

- Stay on top of Medicare and supplemental insurance options

- Consider tax implications of combined income sources

- Build an emergency fund focused on inflation-resistant assets

These steps won’t replace a strong COLA, but they can enhance overall financial resilience. Knowledge truly is power when navigating complex systems like this.

I’ve seen how sharing experiences within community groups helps people discover local resources they might have overlooked. From food assistance programs to senior discounts, small advantages add up.

The Human Side of Economic Statistics

Behind every inflation report and COLA projection are real people making daily choices. A retiree deciding between medications and groceries. A couple calculating whether they can afford a family visit. These stories remind us why accurate adjustments matter deeply.

While forecasts point toward a potentially helpful increase for 2027, staying informed month by month remains wise. Economic landscapes shift, and adaptability serves retirees well.

As we move through the rest of the year, keep an eye on official updates. The final number will provide clarity, but thoughtful preparation throughout the months ahead can make the difference between merely getting by and maintaining a comfortable quality of life.

Retirement should be a time to enjoy the fruits of decades of work, not constant financial stress. A stronger COLA could contribute positively to that goal for millions, provided other costs don’t outpace it. The coming data will tell more of the story.

In wrapping up these thoughts, it’s clear that vigilance and proactive steps go hand in hand with hoping for favorable policy outcomes. Whether you’re already receiving benefits or planning ahead, understanding these dynamics empowers better decisions.

The interplay between inflation trends and benefit adjustments continues to shape retirement realities across the country. By staying engaged with the details and adapting where possible, seniors can navigate the uncertainties with greater confidence. What the final 2027 figure brings remains to be seen, but current signals offer reason for measured optimism amid ongoing challenges.