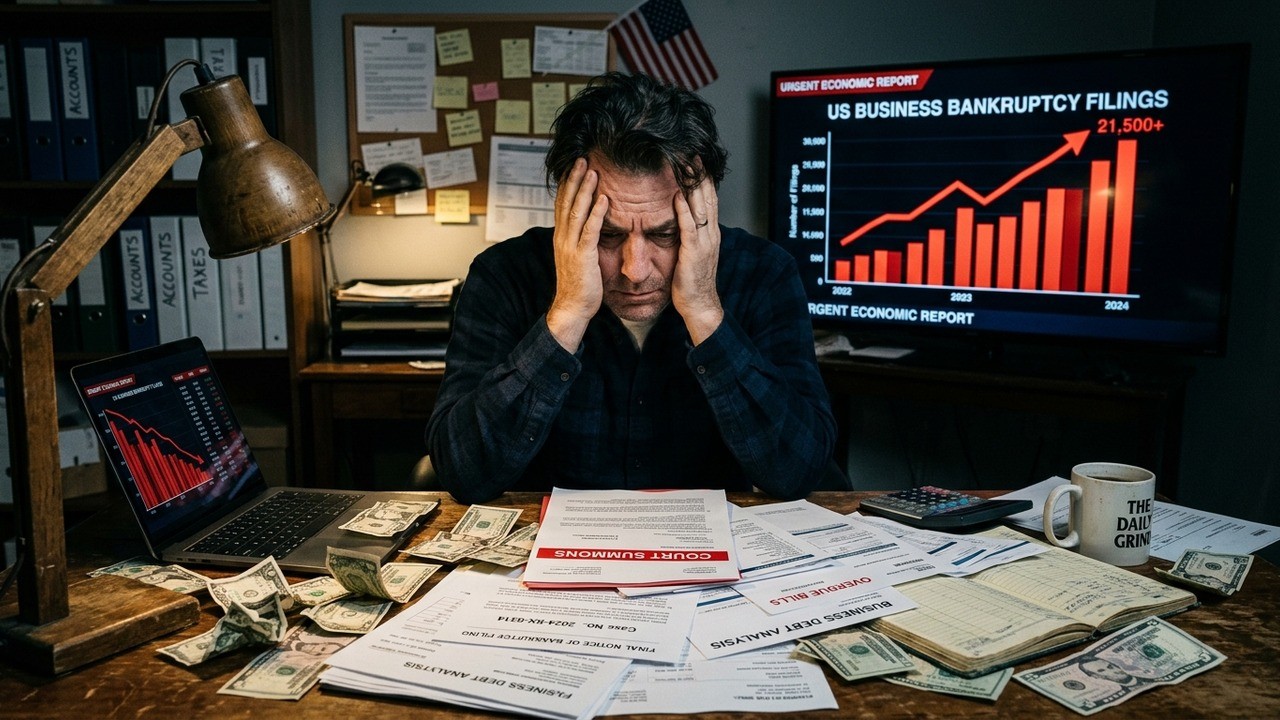

Have you ever wondered what happens when the economy starts showing cracks beneath the surface? Last month brought another reminder that not everything is as stable as the headline numbers might suggest. Total US bankruptcy filings climbed 7 percent compared to the same period last year, painting a picture of growing financial stress across both businesses and individuals.

This increase isn’t just a blip on the radar. It reflects deeper challenges that have been building for some time. From stubborn inflation to high borrowing costs, many are feeling the squeeze. As someone who follows these trends closely, I’ve noticed how these pressures tend to hit certain groups harder than others, and the latest data really drives that point home.

Understanding the Latest Bankruptcy Trends

The numbers released recently show a continued but somewhat measured rise in bankruptcy activity. Individual filings were up by about 8 percent, while overall commercial filings remained nearly flat, dipping just 0.1 percent. However, digging deeper reveals a more troubling story for smaller operations.

Small businesses experienced a significant 36 percent jump in filings. That’s not a small shift. It suggests that many entrepreneurs are struggling to keep their heads above water amid rising costs and tighter credit conditions. This disparity between large and small entities is something worth paying attention to.

The May data reflects a continued but measured uptick in bankruptcy activity, particularly among small businesses.

– Industry data analyst

What makes this trend particularly noteworthy is how it fits into the broader economic landscape. We’ve seen inflation remain above target levels for quite a while now. Recent months have brought further increases, influenced by various global factors. When prices keep climbing, it puts pressure on everyone from consumers to the companies trying to serve them.

The Role of High Interest Rates

Central bank policies have kept benchmark rates elevated for an extended period. Currently sitting in the 3.5 to 3.75 percent range, these levels make borrowing more expensive across the board. For businesses reliant on loans to manage cash flow or expand, this creates real headaches.

I’ve spoken with several business owners who describe the current environment as challenging yet navigable for now. The key issue is access to affordable credit. When rates stay high, it limits options and forces tougher decisions. Some companies are choosing to restructure rather than risk going under completely.

- Elevated borrowing costs reduce expansion plans

- Cash flow management becomes more difficult

- Smaller firms with limited reserves feel the impact first

- Consumer spending patterns shift under financial pressure

This situation didn’t appear overnight. It’s the result of several years of economic adjustments following periods of low rates and stimulus. Now, as the dust settles, the cumulative effects are showing up in bankruptcy statistics.

Chapter 11 Filings: Reorganization or Last Resort?

Chapter 11 bankruptcies, which allow companies to reorganize while continuing operations, saw a 7 percent decline in May compared to the previous year. On the surface, that might sound positive. Yet when you look at the longer trend, Chapter 11 cases have been rising through much of the year.

In the first quarter, these filings jumped 37 percent year-over-year. April saw a 42 percent increase. The May dip breaks that streak but doesn’t necessarily signal improvement. It could simply reflect timing or specific large cases moving through the system at different paces.

One notable example involved a specialty materials company announcing plans to cut debt significantly through restructuring. Cases like this highlight how even established firms are seeking ways to reset their financial footing. For smaller players, the path can be even more precarious.

Small Businesses Bearing the Brunt

The 36 percent surge in small business bankruptcies stands out as one of the most concerning aspects of the latest report. These enterprises often operate with thinner margins and less access to capital markets than their larger counterparts. When costs rise and revenue growth slows, the buffer disappears quickly.

Persistent inflation has forced many to increase prices, but there’s only so much consumers can absorb. At the same time, labor shortages and higher wages add to operational expenses. It’s a difficult balancing act that some simply can’t maintain indefinitely.

The trend highlights the cumulative impact of elevated interest rates, persistent inflation, and higher operating costs.

– Bankruptcy data expert

In my view, this is where the real story lies. Small businesses form the backbone of local economies and job creation. When they struggle, the effects ripple outward to employees, suppliers, and communities. Watching this segment closely can provide early warning signs for broader economic health.

Macroeconomic Factors at Play

Several elements are contributing to this environment. Inflation has fluctuated but recently moved higher again. Fuel prices and global uncertainties, including conflicts in key regions, add layers of complexity. These aren’t abstract concepts – they directly affect business planning and consumer behavior.

Employment data presents a mixed picture. The economy added jobs in May, beating some expectations, and the unemployment rate held steady. However, initial unemployment claims reached a four-month high toward the end of the month. This suggests potential softening in the labor market that could compound financial pressures.

| Indicator | May Performance | Year-over-Year Change |

| Total Bankruptcy Filings | Up | +7% |

| Individual Filings | Up | +8% |

| Small Business Filings | Sharp Rise | +36% |

| Commercial Chapter 11 | Down | -7% |

Stock markets showed resilience during the month, with major indexes gaining ground. Yet market performance doesn’t always tell the full story of underlying business conditions. Many analysts describe the current period as relatively calm but potentially leading into more challenging times ahead.

Government and Policy Responses

Efforts are underway to support businesses, particularly smaller ones. Initiatives to expand loan guarantees and increase financing limits aim to provide breathing room. For manufacturers and capital-intensive sectors, these measures could make a meaningful difference in accessing needed funds.

Whether these steps will be enough remains to be seen. The combination of high rates and inflation creates a tough environment that policy tweaks alone might not fully resolve. Businesses are adapting in various ways – from seeking alternative suppliers to adjusting pricing strategies.

- Many owners have raised prices to protect margins

- Others switched to lower-cost vendors

- Some implemented operational efficiencies

- A significant portion adopted new growth strategies

Surveys indicate that while optimism among small business owners has ticked up slightly, concerns about inflation and labor issues persist. The resilience shown by many is admirable, but it doesn’t eliminate the underlying risks.

Sector-Specific Impacts

Not all industries are affected equally. Some sectors reported improved activity in May, including healthcare, consumer goods, basic materials, and industrials. Others, such as financials, technology, and consumer services, saw declines. This variation underscores how economic pressures play out differently across the economy.

For companies in more cyclical or discretionary areas, the combination of higher costs and cautious consumer spending creates particular vulnerabilities. Those with strong balance sheets and adaptable business models are better positioned to weather the storm.

What This Means for Individuals and Consumers

The rise in personal bankruptcy filings by 8 percent indicates that households are also facing difficulties. Higher prices for everyday goods, combined with elevated interest rates on mortgages, credit cards, and loans, stretch budgets thin. Many families are making difficult trade-offs.

This isn’t just about statistics. Behind each filing is a story of financial strain that affects life decisions, from housing to education and retirement planning. When consumer finances weaken, it can eventually feed back into slower economic growth as spending contracts.

I’ve always believed that personal financial health serves as a key indicator of broader stability. The current trends suggest many are seeking ways to reset and restructure their debts. While bankruptcy provides a fresh start for some, it also comes with long-term consequences that require careful consideration.

Looking Ahead: Potential for More Filings?

Analysts have warned that we might be in a “calm before the storm” period. Macroeconomic uncertainties, including geopolitical tensions and inflationary pressures, could lead to increased filings in coming months. Companies that have been hanging on might reach breaking points if conditions don’t improve.

On the positive side, some businesses are finding creative solutions and adapting to new realities. The question is whether these adaptations will be sufficient or if more widespread challenges lie ahead. Monitoring key indicators like unemployment claims, consumer confidence, and credit availability will be crucial.

This could be the calm before the storm ahead of a potential barrage of commercial bankruptcy filings.

– Legal and financial expert

For investors and business owners alike, staying informed is essential. Understanding these trends can help in making better decisions about risk management, cash reserves, and strategic planning. It’s not about panic, but about preparation.

Strategies for Navigating Uncertain Times

Businesses facing challenges have several options. Some focus on cost control and efficiency improvements. Others explore new revenue streams or markets. Debt restructuring through formal or informal processes can provide relief when needed.

Individuals should review their own finances carefully. Building emergency funds, reducing high-interest debt, and diversifying income sources are timeless principles that gain extra importance during stressful periods. Seeking professional advice early can prevent small issues from becoming larger ones.

- Maintain detailed financial records and forecasts

- Explore government support programs where available

- Consider professional restructuring advice proactively

- Focus on core strengths and customer relationships

- Build flexibility into business models

The current environment demands both caution and creativity. Those who adapt thoughtfully may emerge stronger, while those who ignore warning signs risk more severe outcomes.

Broader Economic Context and Implications

The stock market’s performance in May, with notable gains in major indexes, shows that investor sentiment remains relatively positive despite these underlying pressures. However, equity markets can sometimes diverge from real economy conditions, especially in the short term.

Longer term, sustained increases in bankruptcies could signal deeper issues that eventually affect growth, employment, and market stability. Policymakers face the delicate task of balancing inflation control with support for economic activity.

As rates remain higher for longer, the adjustment process continues. Some sectors benefit from this environment while others struggle. The uneven nature of the recovery creates both opportunities and risks that savvy observers are tracking closely.

Key Takeaways and Final Thoughts

The 7 percent year-over-year increase in US bankruptcy filings for May serves as an important data point. While not catastrophic, it highlights ongoing vulnerabilities, especially for small businesses and individuals dealing with high costs and expensive credit.

In my experience following these developments, such trends rarely reverse suddenly. Instead, they build gradually until conditions shift meaningfully. Whether through policy changes, economic adaptation, or external factors, the coming months will reveal more about the direction we’re heading.

For now, the prudent approach involves awareness, preparation, and flexibility. Businesses and consumers alike would do well to assess their financial positions and consider contingency plans. The economy has shown remarkable resilience before, and it may do so again, but ignoring the signals isn’t wise.

What stands out most is the human element behind these numbers. Each filing represents real people making tough choices. As we navigate this period, supporting sustainable business practices and sound personal finance habits becomes more important than ever. The path forward may not be smooth, but informed decisions can help mitigate risks and identify opportunities even in challenging times.

Staying updated on these trends, understanding their causes, and thinking through potential impacts remains one of the best ways to protect and position yourself for whatever comes next. The surge in May filings is a reminder that vigilance in financial matters always pays off.

This situation continues to evolve, and future reports will provide additional clarity. For those running businesses or managing household finances, the key is balancing optimism with realism. Economic cycles have ups and downs, and being prepared for both is what separates those who merely survive from those who thrive.