Imagine running a fintech operation where your stablecoin balances sit idle between transactions, earning nothing while traditional finance options beckon from the sidelines. What if you could keep everything onchain, maintain full control, and actually generate meaningful yield without complicating your settlement flows? That’s exactly the kind of evolution that just became reality with a significant integration in the payments space.

The world of blockchain payments is maturing rapidly, and one particular development this week caught my attention as particularly noteworthy. A payments-focused chain backed by major players has activated access to a substantial decentralized lending marketplace, potentially changing how enterprises handle their digital asset liquidity.

Unlocking New Possibilities in Onchain Finance

When a dedicated payments blockchain decides to layer sophisticated lending capabilities on top of its core infrastructure, it signals a broader shift in how traditional and decentralized finance can coexist. This isn’t just another protocol launch. It’s a strategic move that bridges everyday business operations with advanced DeFi mechanics.

The integration allows businesses building on this network to lend, borrow, and earn returns on their stablecoin holdings without ever leaving the ecosystem. For companies that process significant volumes of stablecoin transactions, having idle capital sitting in wallets represents missed opportunities. Now, those balances can contribute to productive lending markets while remaining available for seamless settlements.

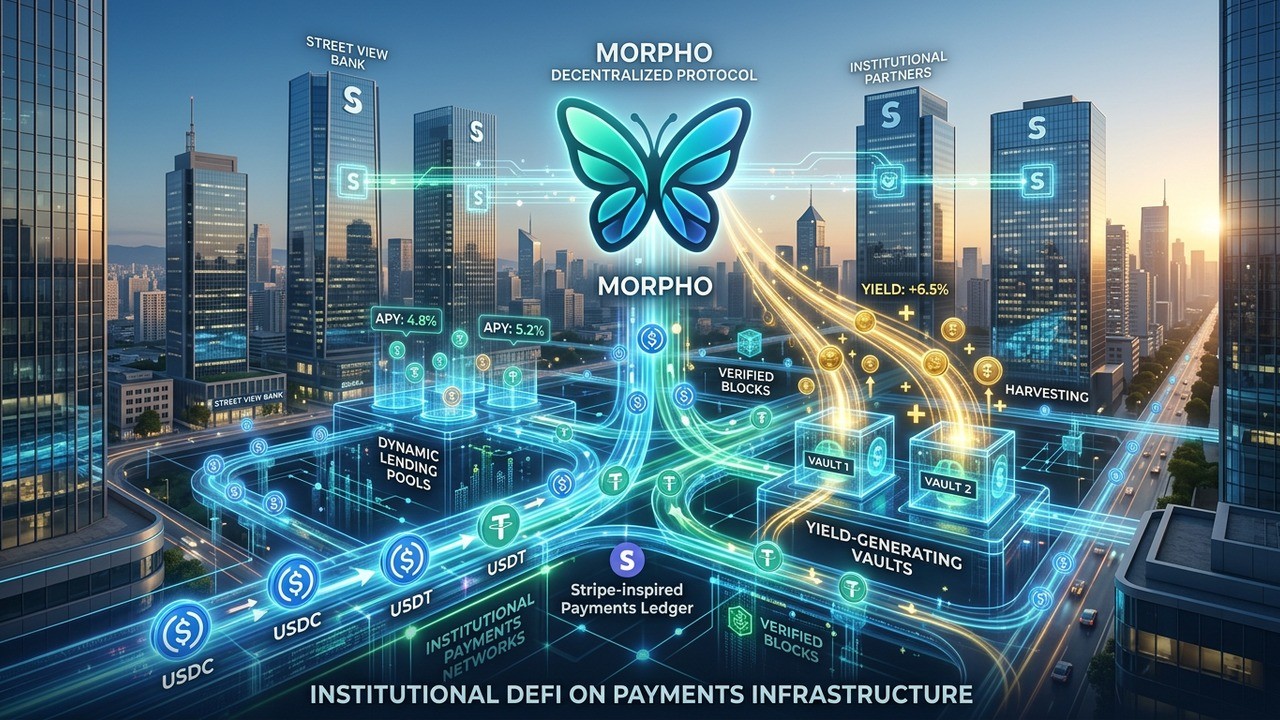

Understanding the Core Components

Let’s break this down without getting lost in technical jargon. The payments chain in question focuses primarily on stablecoin transfers, foreign exchange, and efficient settlement for businesses. It was designed from the ground up to serve enterprise needs, with fees settled in stablecoins and no native gas token complicating the user experience.

On the other side, the lending protocol brings a modular system where different curators establish specific risk parameters and asset rules for individual markets. This approach allows for tailored solutions rather than one-size-fits-all pools that might not suit institutional requirements. Professional risk managers have already begun creating dedicated markets, complete with reliable price oracles for various assets including stablecoins and tokenized real-world items.

We’re seeing growing demand from enterprises looking to integrate DeFi capabilities into their payments products and create more value for their users.

– Industry executive involved in the rollout

This kind of thinking reflects a maturing mindset in the space. It’s no longer enough to simply move money efficiently. Participants want that money to work while it’s waiting, creating additional value within the same trusted environment.

Why Payments Chains Need Lending Layers

Picture this scenario: A large merchant processes thousands of stablecoin transactions daily. Between incoming payments and outgoing settlements, substantial balances accumulate. In traditional banking, these might earn minimal interest in sweep accounts. Onchain, without proper tools, they simply sit there.

The addition of curated lending markets changes the equation entirely. Businesses can now participate in carefully managed pools where risk is calibrated to institutional standards. This isn’t speculative DeFi farming. It’s structured yield generation aligned with payments operations.

I find it particularly interesting how this addresses a real pain point. Many companies exploring blockchain payments have been hesitant because of the opportunity cost of locking capital in non-yielding environments. By integrating lending directly, the chain becomes more attractive as a complete financial operating system rather than just a transfer rail.

The Role of Specialized Curators and Oracles

Not all lending markets are created equal, especially when institutional money enters the picture. That’s where experienced risk firms come in. Two notable entities have stepped up to design and manage dedicated markets, setting parameters around loan-to-value ratios, interest rates, and acceptable collateral types.

Meanwhile, a trusted oracle provider ensures accurate pricing for everything from major stablecoins to bitcoin-backed assets and various tokenized real-world assets. This infrastructure layer is crucial for maintaining confidence in the system, particularly for larger players who can’t afford pricing discrepancies or manipulation risks.

- Curated markets focus on specific risk profiles suitable for enterprise users

- Price feeds cover both crypto-native and tokenized traditional assets

- Governance incentives help bootstrap initial liquidity and activity

- Everything settles within the same chain environment for operational simplicity

The modular nature means that as the ecosystem grows, new curators can emerge with different specializations. Perhaps one focuses on short-term liquidity provision while another handles longer-duration strategies. This flexibility could prove valuable as user needs evolve.

Institutional Interest in Productive Stablecoins

We’ve witnessed increasing appetite from traditional finance players for ways to make stablecoins more than just digital cash equivalents. Major institutions have been exploring various protocols for yield generation, and this integration fits neatly into that trend.

Think about it. Stablecoins have grown tremendously as a medium for transfers and settlements. But holding them shouldn’t mean forgoing returns entirely. By connecting to established lending infrastructure, payments chains can offer a more compelling value proposition to corporate treasurers and fintech operators.

The protocol’s institutional traction tracks broader appetite for productive stablecoin balances.

This development builds on previous examples where other chains have incorporated similar capabilities. The pattern suggests a clear direction: payments infrastructure evolving to include full financial services layers.

Implications for Enterprise Blockchain Adoption

For companies considering blockchain for their payments stack, having built-in yield opportunities removes one major objection. Instead of viewing onchain assets as purely operational, treasurers can see them as part of a broader asset management strategy.

This matters especially in a competitive landscape where multiple institution-friendly chains are vying for attention. The ability to offer seamless payments plus yield creation could become a significant differentiator. Enterprises don’t want to manage multiple systems. They prefer consolidated platforms where transfers, settlements, and capital efficiency coexist.

From my perspective, this represents the next logical step in making blockchain practical for real business use cases. It’s less about hype and more about solving concrete problems around capital efficiency and user experience.

How It Works in Practice

Let’s walk through a simplified example. A fintech company using the payments chain receives stablecoin payments from customers. Rather than letting excess balances sit in a wallet, they route them into approved lending markets. These markets, managed by professional curators, lend to borrowers seeking short-term liquidity.

The fintech earns yield on those lent assets while maintaining the ability to withdraw when needed for settlements. Because everything happens on the same chain, transaction costs and complexity remain low. The risk parameters are set conservatively, aligning with enterprise risk tolerance.

| Process Stage | Traditional Approach | With Lending Integration |

| Receive Payments | Stablecoins sit idle | Option to lend immediately |

| Manage Liquidity | Manual sweeps to banks | Onchain yield markets |

| Settlement Needs | Potential delays | Seamless withdrawal |

| Overall Efficiency | Opportunity cost | Productive capital |

Of course, real implementations involve more nuances around compliance, reporting, and integration with existing systems. But the foundational capability opens doors that were previously closed.

Broader Context in DeFi Evolution

Decentralized finance has come a long way from its early experimental days. What began with permissionless pools accessible to anyone has gradually incorporated more structured approaches suitable for larger participants. Curated markets, professional risk management, and institutional-grade oracles represent this maturation.

Payments chains, in particular, benefit from this evolution because their users typically prioritize reliability and compliance over maximum yields. Conservative, well-managed lending pools fit perfectly with that philosophy.

I’ve observed how different chains are finding their niches. Some focus purely on high-throughput consumer applications while others target enterprise use cases. The ones that successfully layer financial primitives like lending stand to capture more significant mindshare and volume.

Potential Challenges and Considerations

No integration is without hurdles. Smart contract risks, though mitigated through audits and battle-tested code, still exist. Liquidity fragmentation across different chains can create inefficiencies. Regulatory landscapes continue evolving, requiring careful navigation.

However, by working with established protocols and professional curators, the teams involved appear to be taking a measured approach. They’re not rushing into experimental features but building upon proven infrastructure.

- Ensure robust risk management frameworks are in place

- Maintain clear communication with enterprise users about capabilities and limitations

- Continue developing tools for seamless integration with traditional finance systems

- Monitor and adapt to changing regulatory requirements

Success will depend on execution and the ability to deliver genuine value without introducing unnecessary complexity.

Impact on Stablecoin Ecosystem

Stablecoins have become the backbone of onchain economic activity. Making them more productive could accelerate adoption across various sectors. When holding stablecoins on a payments chain offers competitive yields, companies have stronger incentives to increase their usage.

This creates positive feedback loops. More usage leads to better liquidity, which supports more sophisticated financial products, attracting even more participants. We’ve seen similar dynamics in other areas of crypto infrastructure.

Particularly interesting is the potential for tokenized real-world assets to find homes in these lending markets. As traditional assets become increasingly represented onchain, the ability to use them as collateral or lend against them expands the design space considerably.

What This Means for Fintech Builders

Developers and companies building applications on payments infrastructure now have more tools in their arsenal. Instead of focusing solely on transfer mechanics, they can think about comprehensive financial experiences for their users.

Consider a payment app that automatically sweeps idle balances into yield-generating positions. Or treasury management dashboards that show real-time earning potential across different markets. These features could differentiate offerings in a crowded market.

Enterprises and applications can add onchain yield to their services with the open credit network.

The message is clear. The infrastructure is ready for more ambitious applications that blend payments with capital efficiency tools.

Looking Ahead: The Future of Integrated Financial Stacks

As more chains adopt similar approaches, we might see a convergence toward full-stack onchain financial platforms. Payments, lending, trading, and asset management could all coexist within unified environments designed for institutional and enterprise use.

This doesn’t mean decentralized finance will replace traditional systems overnight. Rather, we’re likely heading toward hybrid models where the strengths of both worlds complement each other. Blockchain excels at transparency, speed, and programmability. Traditional finance brings regulatory clarity, deep liquidity, and established trust frameworks.

The most successful players will be those who navigate this intersection thoughtfully, prioritizing user needs over ideological purity.

Risk Management in the New Environment

While the opportunities are exciting, prudent risk management remains essential. Enterprises will need to understand the specific parameters of each lending market they participate in. Diversification across different curators and asset types can help mitigate concentration risks.

Monitoring tools and clear reporting will become increasingly important. Companies won’t want to be surprised by sudden changes in market conditions or protocol parameters. The integration of professional risk managers helps, but doesn’t eliminate the need for internal oversight.

In my experience following these developments, the projects that communicate transparently about risks and maintain conservative parameters tend to build the most lasting trust with institutional users.

Technical Architecture Considerations

From a technical standpoint, integrating lending protocols into a payments chain requires careful attention to several areas. Gas efficiency matters when dealing with high-frequency settlement operations. Security audits and ongoing monitoring are non-negotiable.

The ability to move assets seamlessly between payment accounts and lending positions without excessive friction will determine user adoption. Smart contract design must account for the specific needs of enterprise users, including permissioned access where required and robust error handling.

Key Technical Priorities: - Efficient cross-functionality between payments and lending - Reliable oracle integration for accurate pricing - Scalable market creation and management tools - Clear audit trails for compliance requirements

Teams that get these fundamentals right will have a significant advantage as competition intensifies.

Market Positioning and Competition

The broader landscape includes various initiatives aiming to serve institutional needs with blockchain technology. Some focus on specific verticals while others attempt broader platforms. The ability to combine reliable payments with yield generation positions this particular chain uniquely.

Partnerships with major financial institutions and payment networks provide credibility and distribution channels that purely decentralized projects often lack. At the same time, leveraging established DeFi protocols brings proven technology without reinventing every wheel.

This hybrid approach might prove particularly effective in accelerating adoption among companies that want blockchain benefits without the full complexity of building everything from scratch.

User Experience Revolution

Ultimately, success in this space comes down to user experience. Enterprises don’t care about underlying protocols as long as the tools work reliably and integrate with their existing workflows.

By abstracting away much of the DeFi complexity while retaining the benefits, this integration could set new standards for how businesses interact with onchain financial tools. Simple dashboards showing available yield opportunities, automated allocation options, and clear risk summaries would go a long way.

The goal isn’t to turn corporate treasurers into DeFi power users but to provide institutional-grade tools that feel familiar and trustworthy.

Longer-Term Strategic Implications

Looking beyond the immediate launch, this development hints at how the financial system might evolve over the coming years. As more value moves onchain, the lines between different types of financial activities blur. Payments become intertwined with lending, which connects to asset management and beyond.

Companies that position themselves at these intersections stand to capture significant value. For the broader crypto ecosystem, each successful enterprise integration strengthens the case for blockchain as serious financial infrastructure rather than just a speculative arena.

I’ve always believed that the real transformation happens when technology solves genuine business problems rather than creating new ones. This integration appears to follow that principle by enhancing capital efficiency within existing payment flows.

Preparing for the Next Phase

For observers and participants alike, staying informed about these developments is crucial. The pace of innovation in blockchain payments and DeFi continues accelerating. What seems cutting-edge today might become table stakes tomorrow.

Businesses considering their digital asset strategies should evaluate not just current capabilities but roadmaps and partnership ecosystems. The ability to adapt and expand functionality without disrupting core operations will differentiate winners from also-rans.

As always, thorough due diligence remains essential. Understanding the teams, technology, and economic incentives behind these platforms helps separate substantive progress from marketing hype.

Final Thoughts on This Milestone

This integration represents more than a simple protocol connection. It embodies a philosophy where decentralized technology serves practical business needs rather than existing in isolation. By bringing substantial lending capacity to a payments-focused chain, the groundwork is laid for more sophisticated onchain financial operations.

Whether this sparks wider adoption depends on execution, market conditions, and the broader regulatory environment. But the direction feels right. Enterprises need tools that enhance efficiency and create value. This development delivers on both fronts.

I’ll be watching closely to see how users respond and what additional features emerge. The combination of reliable payments infrastructure with productive capital deployment could unlock meaningful innovation in how businesses manage their digital finances.

The journey toward more integrated onchain financial systems continues, and moments like this feel like genuine progress worth paying attention to. What comes next could reshape expectations for corporate blockchain usage in profound ways.

In the end, it’s about creating systems that work better for the people and organizations who rely on them. If this integration helps achieve that goal even incrementally, it will have been worth the effort. The real test will be in the real-world usage that follows, and I’m optimistic about the potential I see unfolding.