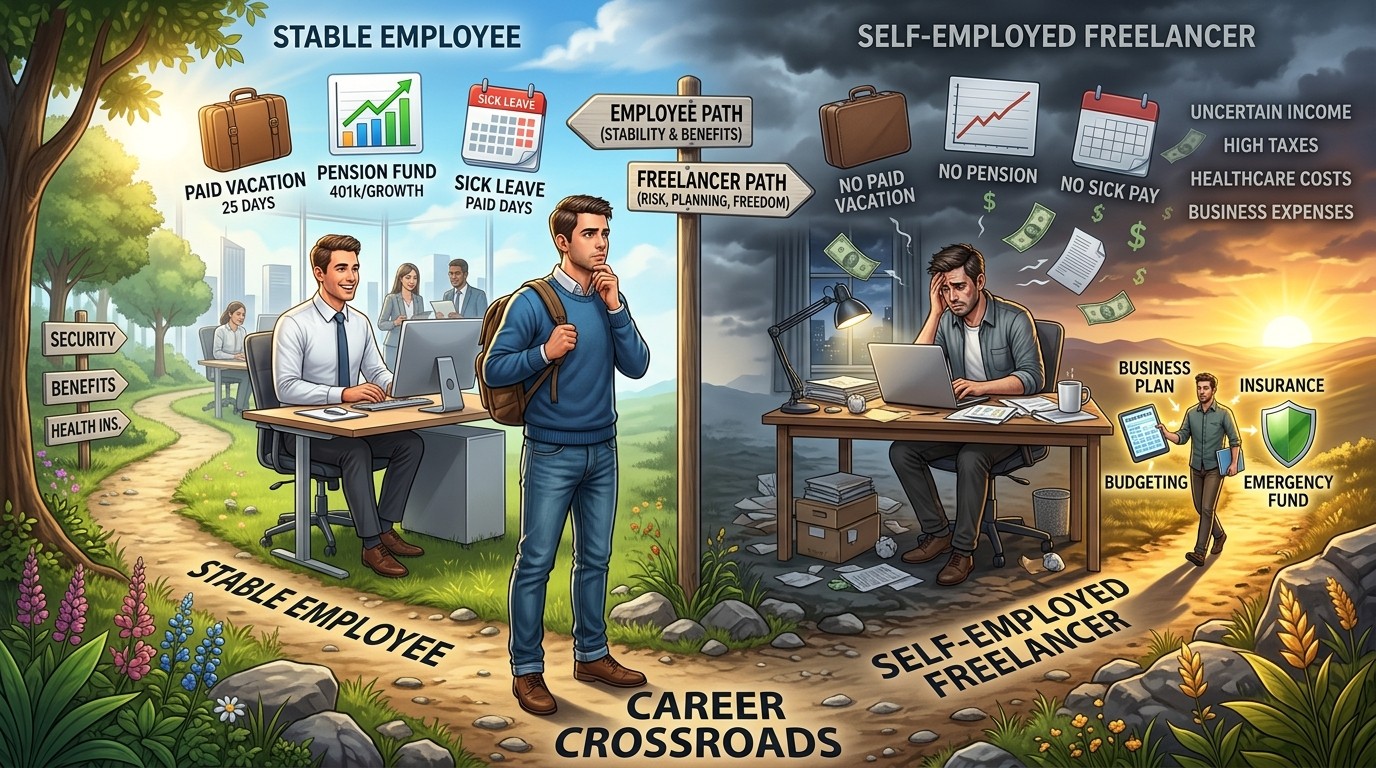

Have you ever fantasized about quitting your job, becoming your own boss, and finally taking control of your schedule? The idea sounds liberating, doesn’t it? Yet behind that dream of independence lies a financial reality that catches many people off guard. Recent analysis suggests that stepping into self-employment could mean waving goodbye to around £6,000 worth of benefits each year that most employed workers take for granted.

I remember chatting with a friend who made the jump a few years back. He loved the flexibility at first, but when he caught a nasty flu and couldn’t work for two weeks, the reality hit hard. No sick pay, no holiday allowance rolling in, and suddenly those “perks” of employment started looking pretty valuable. This isn’t just about missing out on a few days off – it’s a systemic gap that affects everything from daily cash flow to long-term retirement security.

In this comprehensive guide, we’ll break down exactly what you’re giving up when you go solo, why the numbers add up to such a significant sum, and most importantly, practical steps you can take to bridge that gap without losing the freedom that drew you to self-employment in the first place.

Understanding the True Cost of Independence

The appeal of self-employment is obvious. You set your own hours, choose your clients, and potentially keep more of what you earn through smart tax planning. But freedom comes with responsibility, and that responsibility has a price tag. Research indicates the average self-employed person forfeits benefits worth approximately £6,428 annually. That’s not pocket change – it’s real money that impacts your lifestyle and future security.

Let’s put this into perspective. If you’re earning around the UK median salary before going self-employed, replacing those lost benefits might require working an extra three weeks per year just to stay even. Suddenly that “flexible lifestyle” requires more hours than you might have anticipated. But it doesn’t have to be this way. With proper planning, you can recreate many of these protections yourself.

Paid Annual Leave: Your Time Is Now Money

Full-time employees in the UK typically enjoy 28 days of paid annual leave, including bank holidays. For someone earning the median salary of roughly £39,000, this translates to about £4,704 in paid time off. When you’re self-employed, taking a week off means no income during that period unless you’ve built up reserves or planned cleverly.

I’ve seen too many new freelancers burn out because they never schedule proper breaks. They push through, working seven days a week, telling themselves they’ll rest “when the business is stable.” The problem is that stability takes time, and without intentional time off, both your productivity and creativity suffer. Perhaps one of the smartest moves you can make is treating holiday pay as a non-negotiable business expense from day one.

Consider setting aside 12-15% of every invoice specifically for your “paid leave fund.” This way, when you decide to take that well-deserved trip or simply unplug for a week, the money is already allocated. It’s a simple shift in mindset that turns an invisible benefit into a visible priority.

The freedom to choose when you work is wonderful, but only if you actually take time off to enjoy it.

Sick Pay: The Hidden Health Tax

The average UK employee takes around 4.4 sick days per year. At median earnings, that’s approximately £740 covered by their employer. Self-employed individuals face a starkly different reality. Many report taking significantly fewer sick days not because they’re superhumanly healthy, but simply because they can’t afford to stop working.

This creates a dangerous cycle. You push through illness, potentially prolonging recovery time and reducing the quality of your work. Clients notice when you’re not at your best, which can harm your reputation and future earnings. It’s a false economy that many learn the hard way.

- Build an emergency health fund covering at least 4-6 weeks of expenses

- Consider income protection insurance that kicks in after a waiting period

- Look into critical illness cover for more serious health events

- Structure your business to allow for temporary outsourcing during illness

One self-employed consultant I know set up a simple system with a trusted colleague. They cover for each other during short illnesses, maintaining client relationships while recovering. It’s not perfect, but it’s far better than losing income entirely while feeling terrible.

Pension Contributions: The Long-Term Impact

Under auto-enrolment rules, employers must contribute at least 3% of qualifying earnings to an employee’s pension. For someone on median salary, that’s around £984 per year that you’re missing out on as a self-employed person. Over a full career with reasonable investment growth, this can snowball into over £100,000 in lost retirement savings.

That number stopped me in my tracks when I first saw it. We’re not just talking about current income here – this affects the quality of your life decades from now. The good news? You have complete control over your pension strategy when self-employed, which can actually work to your advantage if you play your cards right.

Consider contributing more aggressively during good years to make up the difference. Self-employed individuals can often make tax-efficient contributions that provide immediate tax relief. A personal pension or SIPP (Self-Invested Personal Pension) gives you flexibility that employed workers don’t always have.

The Mortgage Challenge

Getting approved for a mortgage becomes notably more complicated when your income comes from self-employment. Lenders prefer predictable, provable earnings, and business owners often have fluctuating profits, especially in the early years. This can limit how much you can borrow or delay major life decisions like buying a home.

The solution involves meticulous record-keeping from day one. Keep detailed accounts, separate business and personal expenses clearly, and consider incorporating as a limited company if it makes financial sense. Some specialist lenders understand self-employed finances better than high street banks, so shopping around is crucial.

Let’s dive deeper into how these costs accumulate and what strategic moves can help you maintain financial stability while enjoying the autonomy of self-employment.

Creating Your Own Benefits Package

The beauty of self-employment is that you can design a benefits package tailored exactly to your needs rather than accepting a one-size-fits-all corporate offering. However, this requires deliberate planning and treating these costs as essential business expenses rather than optional luxuries.

Start by calculating your true hourly rate. Factor in not just your desired take-home pay, but also time for administration, marketing, professional development, and all those missing benefits. Many freelancers undercharge initially because they don’t account for these hidden costs properly.

| Benefit | Annual Value (approx) | Replacement Strategy |

| Paid Holiday | £4,700 | Build dedicated leave fund |

| Sick Pay | £740 | Income protection insurance |

| Pension Contributions | £984+ | Personal pension with tax relief |

| Other Perks | Variable | Private insurance and savings |

This isn’t about making self-employment sound scary. Far from it. The autonomy and potential earnings upside often outweigh these challenges for the right person. But going in with eyes wide open gives you the best chance of long-term success and financial peace of mind.

Insurance: Your New Best Friend

Business insurance isn’t just a nice-to-have when you’re self-employed – it’s essential protection. Public liability, professional indemnity, and income protection policies can provide the safety net that employers typically offer. While these policies cost money upfront, they can save you from financial disaster if things go wrong.

Think about it like this: when you’re employed, your company absorbs many risks. As a self-employed person, you’re now the company. That means you need to think like a business owner, not just a skilled individual offering services. This shift in perspective is crucial for long-term sustainability.

Visibility of costs isn’t the same as waste. It’s actually the path to better financial decisions.

Tax Efficiency and Business Structure

One area where self-employment can actually outperform traditional employment is in tax planning. Operating through a limited company opens up legitimate ways to manage your finances more efficiently. You can pay yourself a salary and dividends, contribute to pensions with corporation tax relief, and claim various business expenses.

However, this comes with increased administrative responsibility and potentially higher accounting costs. It’s rarely worth going down this route in the very early stages unless your earnings justify it. Many people start as sole traders and incorporate later when the numbers make sense.

- Track every business expense meticulously

- Understand what you can and cannot claim

- Consider quarterly tax payment planning

- Work with a good accountant who understands your industry

- Build relationships with financial advisors specializing in self-employed clients

Building Financial Resilience

Success as a self-employed person often comes down to cash flow management more than raw earnings. Having reserves for quiet periods, unexpected expenses, and those missing benefits makes all the difference between thriving and merely surviving.

Aim to build an emergency fund covering at least six months of essential expenses. This gives you breathing room during client dry spells or economic downturns. Some of the most successful freelancers I know maintain even larger buffers because they’ve experienced how quickly things can change in business.

Diversifying your income streams also provides protection. Rather than relying on one or two big clients, develop multiple revenue channels. This might include retainer work, product sales, teaching, or consulting across different sectors. The more diversified you are, the more secure your financial foundation becomes.

The Mental Side of Financial Planning

There’s a psychological aspect to all this that often gets overlooked. When you’re employed, financial worries about benefits tend to stay in the background. As a self-employed person, these concerns can creep into your daily thoughts, affecting focus and decision-making.

Creating systems that automate as much of your financial protection as possible helps tremendously. Automatic transfers to savings accounts, pension contributions, and insurance premiums mean you don’t have to think about them constantly. This frees up mental energy for growing your business and serving clients effectively.

In my experience working with various professionals, those who treat their self-employment like a proper business from the beginning tend to experience less stress and achieve better results. They view benefit replacement not as an annoying cost but as an investment in their stability and peace of mind.

Practical Steps to Get Started

If you’re considering going self-employed or have recently made the transition, here’s a prioritized checklist to help you address these hidden costs systematically:

- Calculate your current benefit gap based on your expected earnings

- Prioritize income protection and critical illness insurance

- Set up an automatic system for building your leave fund

- Open a suitable pension and set contribution targets

- Review your business structure with an accountant

- Build relationships with specialist financial advisors

- Track your finances using robust accounting software

Remember that these aren’t one-time decisions. Your needs will evolve as your business grows, your personal circumstances change, and economic conditions shift. Regular reviews – perhaps quarterly – ensure your protection strategies remain aligned with your current reality.

Long-Term Perspective on Self-Employment

While the numbers around lost benefits can seem daunting, it’s worth remembering that self-employment offers opportunities that traditional employment simply cannot match. Many self-employed individuals ultimately earn significantly more than they did as employees, precisely because they capture more of the value they create.

The key lies in treating those initial years as an investment phase. You’re building not just a business, but an entire financial ecosystem that supports your lifestyle and goals. This takes time, discipline, and often a willingness to learn new skills around money management.

I’ve watched countless people transform their lives through self-employment. They enjoy greater freedom, pursue work that genuinely excites them, and often achieve financial success that surpasses what was possible in traditional roles. But almost without exception, the ones who thrive are those who respected the financial realities rather than ignoring them.

Making Self-Employment Sustainable

Sustainability comes from balancing the pursuit of growth with adequate protection. It’s easy to get caught up in chasing the next client or project while neglecting the foundational elements that keep everything stable. Yet those foundations – proper insurance, savings buffers, pension planning – are what allow you to take calculated risks and seize opportunities when they arise.

Consider working with professionals who understand the unique challenges of self-employed finances. A good accountant and financial advisor can help you navigate everything from tax optimization to retirement planning in ways that maximize your hard-earned money.

Don’t forget about continuous professional development either. When you’re self-employed, investing in your skills isn’t just nice – it’s essential for maintaining and increasing your value in the marketplace. Many successful freelancers allocate a specific percentage of revenue to training, conferences, and skill enhancement.

Going self-employed represents one of the most significant financial and lifestyle decisions you’ll make. Understanding the true costs involved doesn’t diminish the potential rewards – it actually enhances them by helping you prepare properly.

The £6,000 annual figure isn’t meant to scare you away from entrepreneurship. Rather, it should empower you to approach self-employment with realistic expectations and a solid plan. By addressing these hidden costs proactively, you position yourself not just to survive as your own boss, but to truly thrive with the freedom and fulfillment that self-employment can provide.

Take time to assess your personal situation, calculate your specific benefit gap, and create a tailored strategy that works for your industry, risk tolerance, and goals. The investment you make in proper planning today will pay dividends for years to come – both financially and in terms of reduced stress and increased confidence in your business journey.

Self-employment isn’t for everyone, but for those willing to embrace both the opportunities and responsibilities, it can be incredibly rewarding. The key is going into it informed, prepared, and proactive about replacing those workplace benefits with systems and protections of your own design. Your future self will thank you for it.

(Word count: approximately 3250)