Consumer Credit Shrinks Unexpectedly As Credit Card Rates Surge

Consumer credit just recorded its first drop since late 2024 as Americans paid down credit cards amid painfully high rates. Is this a sign of caution or mounting pressure on household budgets? The details reveal more than you might expect...

Financial market analysis from 09/07/2026. Market conditions may have changed since publication.

Have you ever opened your monthly statements and felt that quiet unease when the numbers don’t add up the way you expected? That’s exactly what many economists experienced recently when fresh data showed consumer credit unexpectedly pulling back. After months of steady growth, particularly in revolving debt like credit cards, May brought a notable shift that has everyone paying closer attention.

The latest figures reveal total consumer credit contracted for the first time since November 2024. Instead of the anticipated increase, we saw an outright decline. This development comes at a time when many households are already navigating higher costs for everything from groceries to gas. It’s the kind of data point that makes you pause and wonder what’s really happening beneath the surface of our economy.

Understanding the Sudden Shift in Consumer Borrowing

What makes this contraction particularly interesting is how it breaks a recent pattern. The previous two months had shown strong gains in consumer credit, partly fueled by rising energy prices and broader inflationary pressures. Yet May flipped the script entirely. Non-revolving credit, which includes things like auto and student loans, grew only modestly while revolving credit actually decreased.

In my experience following these trends, such reversals often signal changing consumer sentiment or external pressures finally taking their toll. People aren’t just spending less on credit – in some cases, they’re actively paying down balances. That deserves a closer look.

Breaking Down the Numbers: Revolving vs Non-Revolving Credit

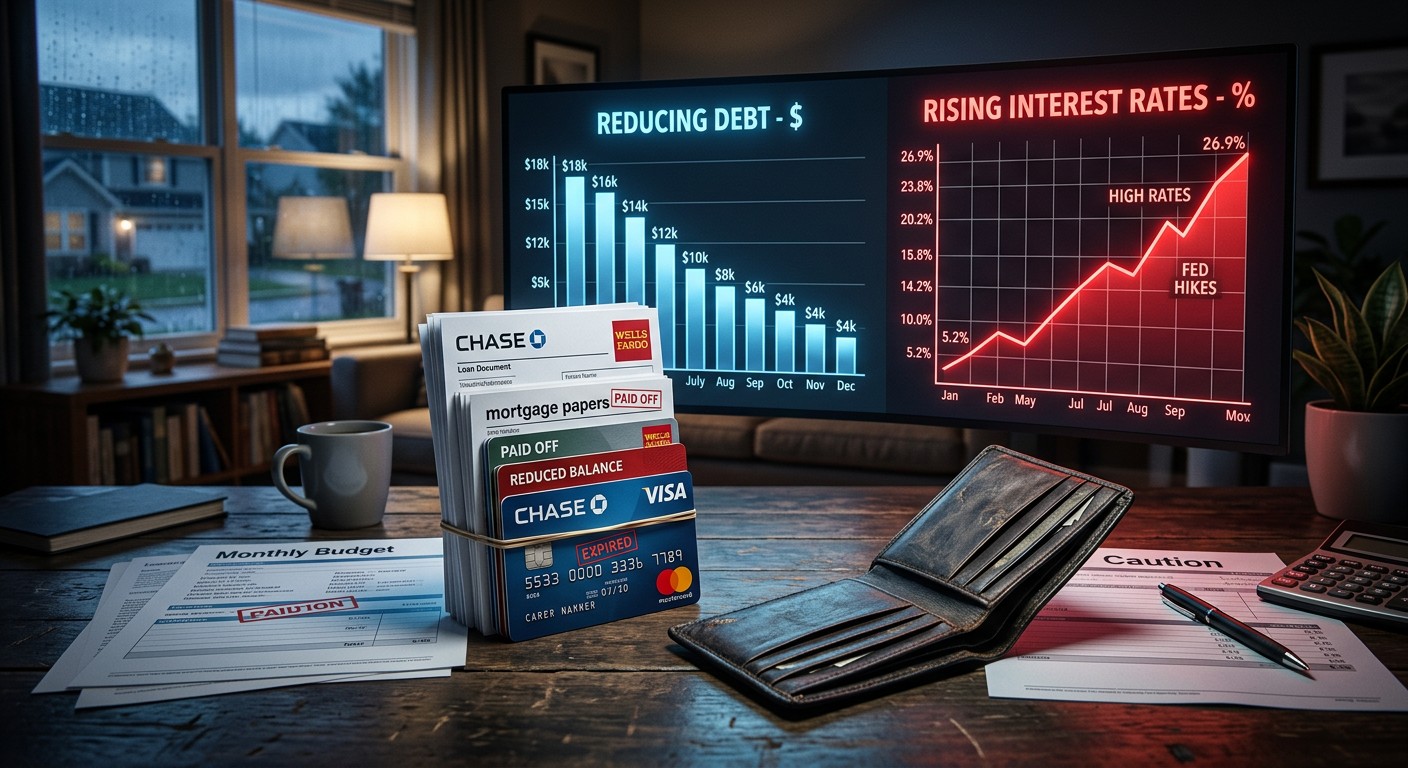

Revolving credit, primarily credit cards, dropped by a significant amount in May. This stands out after two straight months of increases exceeding $10 billion each. Consumers appear to have hit the brakes on accumulating more card debt, possibly due to those eye-watering interest rates we’re seeing.

On the other side, non-revolving credit saw only a small uptick. Car loans and student debt combined added just a fraction of what analysts had projected. This slowdown raises questions about big-ticket purchases and long-term borrowing commitments.

When borrowing slows this abruptly, it can point to either prudent financial management or households feeling squeezed by existing obligations.

I’ve found that the truth usually lies somewhere in between, depending on which income groups we’re examining. Lower and middle-income families often feel these shifts more acutely.

Credit Card Rates Reach Levels Not Seen in Years

One factor that’s impossible to ignore is the cost of borrowing on credit cards. The average interest rate on accounts that actually assess interest climbed to 22.15%. That’s a level we haven’t seen in three years, even though overall policy rates have eased somewhat from their peaks.

This stubbornness in credit card pricing highlights how lending institutions protect their margins. Rates go up quickly when conditions tighten, but they seem reluctant to come back down even when broader rates moderate. It’s a pattern that’s frustrated many borrowers over the years.

- Credit card rates remain elevated despite some cooling in official benchmarks

- Consumers are responding by paying down balances rather than adding new debt

- This paydown could influence retail spending in coming months

The question many are asking is whether this signals broader caution or if it’s simply a reaction to unsustainable debt loads. Perhaps it’s a bit of both.

The Story Behind Auto Loans and Student Debt

Auto loans have remained remarkably stable for nearly three years now, hovering around the same level. That consistency is noteworthy in a market where vehicle prices have climbed substantially. The average amount financed for new cars hit a record in early 2026, reaching over $42,000. No wonder loan growth has been muted – the sticker shock is real for many buyers.

Student loans, by contrast, continue their long-term upward trajectory. After a brief pause, balances are once again approaching all-time highs near $1.9 trillion. This segment of debt has its own unique dynamics, influenced by repayment plans, forgiveness programs, and the ongoing costs of higher education.

When you step back and look at the bigger picture, these two categories represent different aspects of consumer finances. One reflects immediate lifestyle choices while the other ties into long-term investment in one’s future earning potential.

What This Means for Everyday Households

For the average person, these numbers aren’t just abstract statistics. They translate into real decisions about budgeting, saving, and spending. If more people are paying down credit cards instead of swiping for new purchases, we might see that reflected in softer retail sales figures soon.

I’ve spoken with friends and colleagues who describe cutting back on discretionary spending as rates make carrying balances too expensive. One colleague mentioned finally tackling her credit card debt after years of minimum payments. Stories like hers are probably becoming more common.

The psychology of debt changes when the cost becomes painfully obvious each month.

This contraction could indicate that many Americans are prioritizing financial health over short-term consumption. Or it might reflect limited access to new credit for those with stretched budgets. Either way, it’s worth monitoring closely.

Broader Economic Implications

Consumer spending drives a huge portion of economic activity. When credit growth slows or reverses, it can act as a brake on overall momentum. Retailers, service providers, and manufacturers all feel the effects eventually.

At the same time, lower borrowing can help reduce systemic risks if it prevents debt from spiraling out of control. There’s a delicate balance here. Too much credit expansion creates bubbles, but too little can starve the economy of necessary fuel.

- Reduced consumer borrowing may slow GDP growth in coming quarters

- Paydown of high-interest debt improves household balance sheets long-term

- Businesses may need to adjust inventory and hiring plans accordingly

- Policy makers will be watching for signs of broader weakness

The recent geopolitical events, including tensions that affected energy markets, added another layer of complexity. Higher gas prices earlier in the year likely influenced spending patterns before this May pullback.

Historical Context and Comparisons

Looking back, consumer credit behavior has always been sensitive to interest rates and economic confidence. Periods of contraction often coincide with caution ahead of potential downturns or after major shocks. Yet each cycle has its unique characteristics.

In this case, the stability in auto loan balances over several years stands out. It suggests that despite rising vehicle costs, Americans aren’t rushing to finance bigger purchases at current rates. The record average loan size tells its own story about affordability challenges in the auto market.

Student debt’s relentless climb, meanwhile, reflects structural issues in education financing that go beyond short-term economic cycles. This isn’t something that will resolve quickly, and it affects younger generations’ ability to take on other forms of debt like mortgages.

Personal Finance Lessons From the Data

There’s practical wisdom to extract here for your own situation. High credit card rates make carrying balances extremely costly over time. Paying them down aggressively, as many seem to be doing, can free up future cash flow and reduce stress.

Before taking on new auto debt, it’s worth shopping around for the best rates and considering whether the purchase is truly necessary. With average financing amounts so high, even small differences in interest can add up to thousands over the life of a loan.

For those with student loans, staying informed about repayment options and potential policy changes remains important. The balances are large, but so is the potential return on that educational investment if managed wisely.

Potential Impact on Retail and Consumer Sectors

If credit card balances continue to decline, we could see noticeable effects on retail sales. Many discretionary purchases are funded through plastic, especially during periods of wage stagnation or higher essential costs. June’s retail numbers will be particularly telling in this regard.

Businesses that rely on consumer spending might need to get creative with promotions or financing offers to maintain momentum. On the flip side, this deleveraging could create healthier foundations for future growth if it reduces financial vulnerabilities.

Sometimes stepping back from borrowing is the smartest move forward.

That’s a perspective worth considering in our debt-heavy modern economy. Not every contraction is a crisis – some represent necessary adjustments.

Looking Ahead: What to Watch For

The coming months will reveal whether this May contraction was a one-off blip or the start of a new trend. Key indicators to monitor include employment data, wage growth, inflation readings, and of course, future consumer credit reports.

Policy responses could also play a role. If officials see signs of excessive weakness, they might adjust approaches to support growth. Conversely, persistent inflation could keep rates elevated longer than hoped.

For individuals, the best strategy often involves building emergency savings, managing existing debt responsibly, and avoiding unnecessary leverage. These timeless principles become even more relevant during uncertain periods.

As we digest this unexpected decline in consumer credit, it’s clear that American households are making calculated decisions in response to current conditions. High credit card rates are prompting paydowns, while big-ticket financing remains cautious. This dynamic will shape economic activity in the quarters ahead.

The situation reminds us that economies are ultimately collections of individual choices. When enough people decide to tighten their belts or pay down plastic, the effects ripple outward. Whether this leads to slower growth or sets the stage for more sustainable expansion remains to be seen.

What stands out most is the resilience and adaptability consumers continue to show. Facing higher rates and costs, many are choosing prudence over further accumulation. That deserves recognition even as we keep a close eye on the broader implications.

In the end, personal financial health contributes to national economic strength. By understanding these trends, we can all make better informed decisions for our own situations and communities. The coming data releases will provide more clarity, but for now, this May surprise serves as a valuable reminder to stay vigilant about borrowing and spending habits.

Expanding further on the context, it’s important to consider how different generations are responding. Younger adults burdened with student debt might be more hesitant to add credit card balances, while established professionals could be focusing on wealth building rather than consumption. These behavioral shifts matter.

Moreover, regional differences likely exist. Areas with higher costs of living might show stronger paydown trends as families grapple with expenses. Rural versus urban dynamics could also influence borrowing patterns in interesting ways.

Another angle involves the role of technology and fintech in consumer finance. Digital tools make it easier to track spending and automate payments, potentially contributing to more disciplined debt management. This evolution in personal finance management deserves attention.

Thinking about the auto sector specifically, the high average loan amounts reflect not just vehicle prices but also features and technology that have become standard. While this improves the driving experience, it raises the barrier to entry for many buyers. Manufacturers and lenders will need to address affordability to stimulate demand.

On student loans, the societal conversation continues around value, accessibility, and outcomes. With balances at record levels, ensuring that education translates into sufficient earning power is crucial for the debt to remain sustainable at a macro level.

Beyond the immediate numbers, this report invites reflection on our relationship with credit as a society. Credit can be a powerful tool for opportunity when used wisely, but it becomes burdensome when overextended. Finding that sweet spot is an ongoing challenge for individuals and policymakers alike.

As summer progresses and we approach key economic releases, staying informed will help navigate whatever comes next. Whether you’re managing personal finances or simply curious about the bigger picture, these developments affect us all in various ways.

The surprise contraction in consumer credit serves as both a warning and potentially a positive signal of deleveraging. Time will tell which interpretation proves more accurate, but one thing is certain: careful attention to these trends remains essential for anyone interested in economic health and personal prosperity.

Don't let money run your life, let money help you run your life better.

Liquid Staking Tokens: stETH and Depeg Risks Explained

Why MemeCore Exploded 150% This Week: The Full Story

Related Articles

Bybit and OKX Users Increase Bitcoin Holdings as USDT Balances Drop

On major exchanges like Bybit and OKX, users have noticeably increased their Bitcoin positions in recent weeks while letting USDT balances decline. What does this shift reveal about current market sentiment and future price movements?

China’s Biotech Boom Challenges U.S. Pharma Dominance

China’s biotech is skyrocketing, rivaling U.S. giants with cutting-edge drugs and billion-dollar deals. Can they overtake the West in innovation? Click to find out.

Bitcoin Hits $125K: Can It Reach $150K Soon?

Bitcoin just hit $125,600, a historic high! ETFs are booming, and the Fed’s rate cuts are fueling the rally. Could $150K be next? Click to find out!